Monday’s session was outlined by geopolitical whiplash as a fast sequence of conflicting US-Iran headlines drove sharp reversals throughout oil, equities, and bond markets all through the day. Expectations for a diplomatic breakthrough had been repeatedly raised and dashed: Iran rejected US calls for as unacceptable, a drone struck close to a UAE nuclear facility, and reviews emerged that President Trump had deliberate renewed navy strikes on Iran for Tuesday.

By the late US afternoon, Trump confirmed on social media he had known as off the assault after the leaders of Saudi Arabia, Qatar, and the UAE requested extra time for negotiations, serving to oil ease off intraday highs and equities trim their losses — although multi-year excessive bond yields and chronic power provide uncertainty left the broader threat backdrop fragile into the shut.

Take a look at the foreign exchange information and financial updates you could have missed within the newest buying and selling session!

Foreign exchange Information Headlines & Knowledge:

- New Zealand Companies NZ PSI for April 2026: 48.9 (45.0 forecast; 46.0 earlier)

-

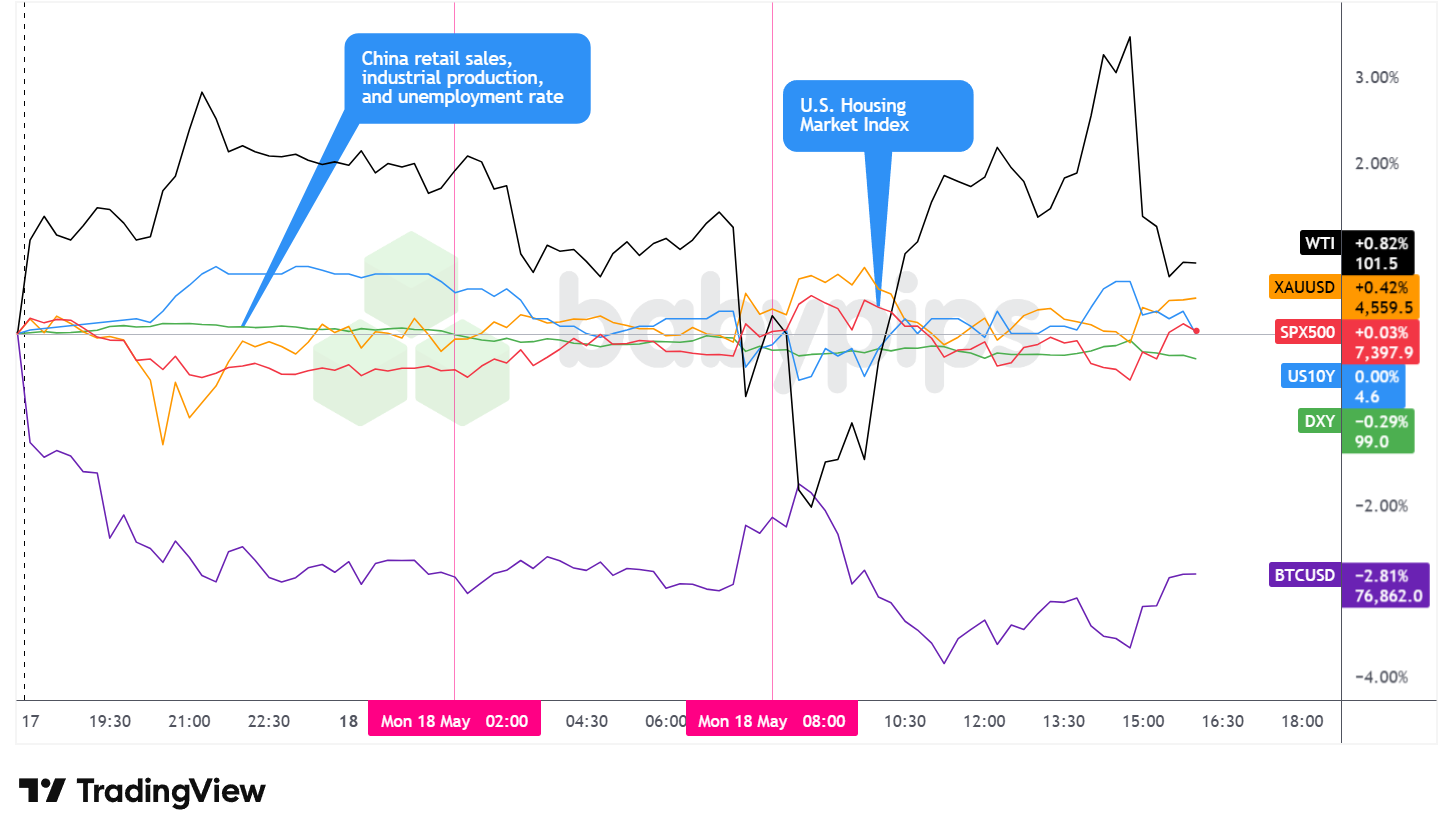

China’s April financial knowledge got here in broadly under expectations, including a second headwind to the day’s already fragile threat surroundings.

- China Home Value Index for April 2026: -3.5% y/y (-3.5% y/y forecast; -3.4% y/y earlier)

- China Unemployment Fee for April 30, 2026: 5.2% (5.5% forecast; 5.4% earlier)

- China Industrial Manufacturing for April 2026: 4.1% y/y (5.5% y/y forecast; 5.7% y/y earlier)

- China Retail Gross sales for April 2026: 0.2% (2.2% forecast; 1.7% earlier)

- China Fastened Asset Funding (YTD) for April 2026: -1.6% y/y (1.5% y/y forecast; 1.7% y/y earlier)

- Swiss GDP Progress Fee Flash for March 31, 2026: 0.5% q/q (0.3% q/q forecast; 0.2% q/q earlier)

- U.S. NY Fed Companies Exercise Index for Could 2026: -5.8 (-14.0 earlier)

- U.S. NAHB Housing Market Index for Could 2026: 37.0 (35.0 forecast; 34.0 earlier)

- The US Treasury Division issued a brand new 30-day basic license permitting the sale of Russian crude oil and petroleum merchandise presently loaded on tankers, days after the earlier waiver lapsed.

- US President Donald Trump mentioned he was “not open” to concessions after Iran’s newest response on peace talks; says he’ll maintain off on Iran assaults at request of Gulf states

Promoted: Day merchants & Scalpers have higher odds of creating nice choices in the event that they see market catalysts straight away. Get the real-time feed that professionals use to catch the information.

Be part of FinancialJuice for Free to study extra!

Disclosure: We could earn a fee from our companions if you happen to join via our hyperlinks, at no further price to you.

Broad Market Value Motion:

Greenback Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Sooner With TradingView

Monday’s broad market panorama was formed nearly totally by the evolving US-Iran diplomatic narrative, with property whipsawing as headlines alternated between escalation and aid all through the session.

WTI crude oil posted the strongest efficiency amongst tracked property, gaining roughly 0.82% to commerce close to $101.50 per barrel. The intraday vary, nonetheless, was significantly wider — costs surged to the $104 space throughout the US session on issues about renewed navy motion earlier than reversing sharply after Trump introduced the cancellation of Tuesday’s deliberate strike. The back-and-forth worth motion carefully tracked the information movement, with oil costs remaining elevated relative to the prior session even after the late-day pullback, probably reflecting the continued closure of the Strait of Hormuz and the absence of a reputable decision to the battle.

Gold superior roughly 0.42% to commerce close to $4,559.50, probably holding its function as a partial safe-haven hedge even because the session’s threat temper oscillated in each instructions. The valuable steel’s intraday volatility was comparatively contained in contrast with oil, bitcoin and equities, with costs discovering broad assist all through the day.

The S&P 500 closed roughly flat, up roughly 0.03% close to 7,397.9, masking a turbulent session that noticed the index drop sharply on damaging Iran headlines earlier than recovering most of its losses following Trump’s strike cancellation. The index briefly pushed towards the 7,430 space throughout the restoration earlier than fading into the shut, suggesting that whereas the diplomatic information offered short-term aid, lingering issues about elevated power prices and multi-year excessive bond yields continued to restrict upside participation.

The US 10-year Treasury yield closed slightly below 4.60%, roughly unchanged on the day, although the intraday journey was removed from quiet. Yields climbed to roughly 4.63% throughout the Asian session earlier than partially retracing as diplomatic hypothesis briefly improved sentiment, then stabilized close to opening ranges via the US afternoon. The muted internet day by day change belied a risky session wherein yields served as a barometer for shifting war-risk and inflation expectations all through the day.

Bitcoin was the session’s weakest performer amongst tracked property, declining roughly 2.81% to commerce close to $76,862. The cryptocurrency had weakened from the Asia session open, briefly discovering assist close to the $76,000 space earlier than consolidating in a subdued vary via the US session. The decline prolonged a pullback that started final week as threat sentiment deteriorated throughout asset lessons amid the escalating Iran battle.

Promotion: In case your confidence has grown in your market consciousness & methods with this market recap, and also you wanna take motion, Maven Buying and selling might help. They supply simulated funding challenges beginning as little as $15, permitting you to commerce main pairs with professional-sized capital. No deadlines imply you may take swing performs on these market themes with out the strain of a ticking clock.

Be taught Extra About Maven Buying and selling In the present day!

Disclosure: We could earn a fee from our companions if you happen to join via our hyperlinks, at no further price to you.

FX Market Conduct: U.S. Greenback vs. Majors

Overlay of USD vs. Majors – Chart Sooner With TradingView

The US greenback ended Monday as one of many weakest performers among the many main currencies, posting declines towards all friends besides the Japanese yen.

Throughout the Asian session, the greenback opened with a modest rebound, probably reflecting early-session warning as markets digested the most recent developments in Iran ceasefire negotiations and the information of a drone strike close to the UAE nuclear facility. That preliminary restoration proved short-lived. From across the center of the Asian morning, the greenback turned broadly decrease towards the main currencies as China’s disappointing April knowledge landed — retail gross sales badly lacking at 0.2% towards a 2.2% forecast, industrial manufacturing coming in properly under expectations at 4.1%, and fixed-asset funding contracting year-to-date. The dollar’s weak point via this era prolonged throughout most pairs, and the overlay chart above exhibits the transfer coinciding with the China knowledge, in line with a broad shift in market sentiment as the info crossed.

The London session prolonged the greenback’s decline into the European morning, with broad USD softness persisting via roughly mid-session as no main UK or eurozone knowledge releases offered a countervailing catalyst. The greenback’s decline eased towards the center of the London morning earlier than the dollar started to stabilize and get better.

Heading into the US session, the greenback staged a partial rebound throughout the board, probably reflecting pre-session positioning or a modest enchancment in sentiment as Trump’s public commentary started to form expectations across the Iran state of affairs. Nonetheless, the restoration was temporary: the greenback turned decrease once more simply forward of the US session open, with the overlay chart exhibiting a renewed leg down throughout a number of pairs within the minutes earlier than the NY open. As soon as US buying and selling was underway, the greenback stabilized and traded sideways and uneven via the shut, with the NAHB Housing Market Index beat at 10:00 ET (annotated on the chart) briefly correlating with a gentle USD bounce that settled into sideways motion, probably reactions to geopolitical information movement.

Promotion: When the Market Swings, Are You Reacting or Executing?

In “Optimistic Buying and selling Psychology,” famend psychologist Brett Steenbarger reveals in his latest e-book that the key to navigating volatility isn’t “fixing” your flaws—it’s doubling down in your innate character strengths. Discover ways to keep medical whereas the remainder of the market is emotional, turning sudden market shaking information into your skilled edge.

Be taught extra about “Optimistic Buying and selling Psychology: Turning private strengths into buying and selling strengths” on Amazon!

Disclosure: We could earn a fee from our companions if you happen to join via our hyperlinks, at no further price to you.

Upcoming Potential Catalysts on the Financial Calendar

- New Zealand Enterprise NZ PMI for April 2026 at 10:30 pm GMT

- New Zealand Meals Value Index for April 2026 at 10:45 pm GMT

- U.S. Fed Barr Speech at 11:00 pm GMT

- Japan PPI for April 2026 at 11:50 pm GMT

- China President Trump and President Xi Summit

- Australia Client Inflation Expectations for Could 2026

- Japan Machine Device Orders for April 2026 at 6:00 am GMT

- Swiss Industrial Manufacturing for March 31, 2026 at 6:30 am GMT

- China Present Account Prel for March 31, 2026 at 9:00 am GMT

- U.Ok. NIESR Month-to-month GDP Tracker for April 2026

- Canada Housing Begins for April 2026 at 12:15 pm GMT

- Canada Manufacturing Gross sales Closing for March 2026 at 12:30 pm GMT

- U.S. NY Empire State Manufacturing Index for Could 2026 at 12:30 pm GMT

- U.S. Industrial & Manufacturing Manufacturing for April 2026 at 1:15 pm GMT

- U.S. Capability Utilization Fee for April 2026 at 1:15 pm GMT

Tuesday’s calendar opens in a single day with Japan’s preliminary Q1 2026 GDP print and GDP Value Index at 11:50 pm GMT, providing the primary take a look at whether or not the Japanese financial system contracted below the burden of surging power import prices. Australian markets might be watching the RBA Assembly Minutes at 1:30 am GMT, together with a speech from RBA’s Hunter at 12:30 am GMT and the Westpac Client Confidence studying, for any steering on the RBA’s fee path within the present high-energy-cost surroundings.

Throughout the European morning, the UK employment replace arrives at 6:00 am GMT, overlaying Claimant Depend Change for April and the Unemployment Fee for March, with the potential to affect Financial institution of England fee expectations. BoE Deputy Governor Breeden speaks at 9:10 am GMT, and ECB Chief Economist Lane follows at midday GMT.

The North American session brings Canada’s April CPI at 12:30 pm GMT alongside Constructing Permits and the New Housing Value Index — Canada’s inflation print might be watched carefully given the worldwide power worth backdrop. Fed Governor Waller speaks at 1:00 pm GMT, and US Pending Residence Gross sales for April are due at 2:00 pm GMT. Waller’s remarks particularly could also be carefully monitored for clues about how the Fed is considering the speed path as oil costs hold inflation dangers elevated.

Keep frosty on the market, foreign exchange pals!

Monday’s session was fully pushed by geopolitical whiplash as US-Iran tensions alternated between escalation and de-escalation all through the day. Most merchants don’t perceive how occasions like these transfer currencies past the plain safe-haven movement. Premium members can learn our lesson:

📖 Geopolitical Threat, Commerce Coverage, and Protected Haven Flows

Studying this helps you perceive which currencies profit when world threat sentiment deteriorates, how geopolitical shocks transmit via asset costs, and which protected havens to observe when the world begins breaking issues.

And if you happen to’re not a Premium subscriber but, now’s a great time to enroll.

With Babypips Premium, you get full entry to Faculty of Pipsology classes that make it easier to perceive methods to place for geopolitical threat, acknowledge the warning indicators earlier than strikes hit, and revenue from the safe-haven flows that dominate session after session.