Markets prolonged their record-breaking run on Thursday as President Trump introduced a 10-day Israel-Lebanon ceasefire and TSMC posted a 58% soar in quarterly revenue, offering each geopolitical and elementary gas for the rally. The S&P 500 logged one other all-time closing excessive whereas the U.S. greenback completed as one of many session’s better-performing main currencies, gaining towards all majors besides the Canadian greenback.

Take a look at the foreign exchange information and financial updates you will have missed within the newest buying and selling session!

Foreign exchange Information Headlines & Knowledge:

- Australia Shopper Inflation Expectations for April 2026: 5.9% (5.4% forecast; 5.2% earlier)

- Australia Employment Change for March 2026: 17.9k (34.2k forecast; 48.9k earlier)

- China GDP Development Price for March 31, 2026: 5.0% y/y (5.2% y/y forecast; 4.5% y/y earlier); 1.3% q/q (1.4% q/q forecast; 1.2% q/q earlier)

- China Retail Gross sales for March 2026: 1.7% y/y (3.5% y/y forecast; 2.8% y/y earlier)

- China Unemployment Price for March 31, 2026: 5.4% (5.2% forecast; 5.3% earlier)

- China Industrial Manufacturing for March 2026: 5.7% y/y (5.4% y/y forecast; 6.3% y/y earlier)

- U.Okay. Manufacturing Manufacturing for February 2026: -0.5% y/y (-0.5% y/y forecast; 1.3% y/y earlier); -0.1% m/m (0.1% m/m forecast; 0.1% m/m earlier)

- U.Okay. GDP for February 2026: 1.0% y/y (1.0% y/y forecast; 0.8% y/y earlier)

- Swiss Producer & Import Costs for March 2026: -2.7% y/y (-0.2% y/y forecast; -2.7% y/y earlier); 0.2% m/m (0.2% m/m forecast; -0.3% m/m earlier)

- SNB Financial Coverage Assembly Minutes: The minutes present the SNB protecting its coverage fee at 0%, judging total financial circumstances as having tightened as a result of Swiss franc appreciation and seeing its conditional inflation forecast nonetheless throughout the value stability vary and really near the earlier quarter’s path.

-

Euro space CPI Development Price Closing for March 2026: 2.6% y/y (2.5% y/y forecast; 1.9% y/y earlier)

- Euro space Core Inflation Price Closing for March 2026: 2.3% y/y (2.3% y/y forecast; 2.4% y/y earlier)

- Canada New Motor Car Gross sales for February 2026: 124.0k (80.0k forecast; 114.41k earlier)

- U.S. Preliminary Jobless Claims for April 11, 2026: 207.0k (216.0k forecast; 219.0k earlier)

- U.S. NY Fed Providers Exercise Index for April 2026: -14.0 (-22.6 earlier)

- Philadelphia Fed Manufacturing Index for April 2026: 26.7 (17.0 forecast; 18.1 earlier)

- U.S. Industrial Manufacturing for March 2026: 0.7% y/y (1.8% y/y forecast; 1.4% y/y earlier)

- U.S. Manufacturing Manufacturing for March 2026: 0.5% y/y (2.0% y/y forecast; 1.3% y/y earlier)

Promoted: Day merchants & Scalpers have higher odds of creating nice choices in the event that they see market catalysts instantly. Get the real-time feed that execs use to catch the information.

Be a part of FinancialJuice for Free to be taught extra!

Disclosure: We could earn a fee from our companions in case you enroll by way of our hyperlinks, at no further value to you.

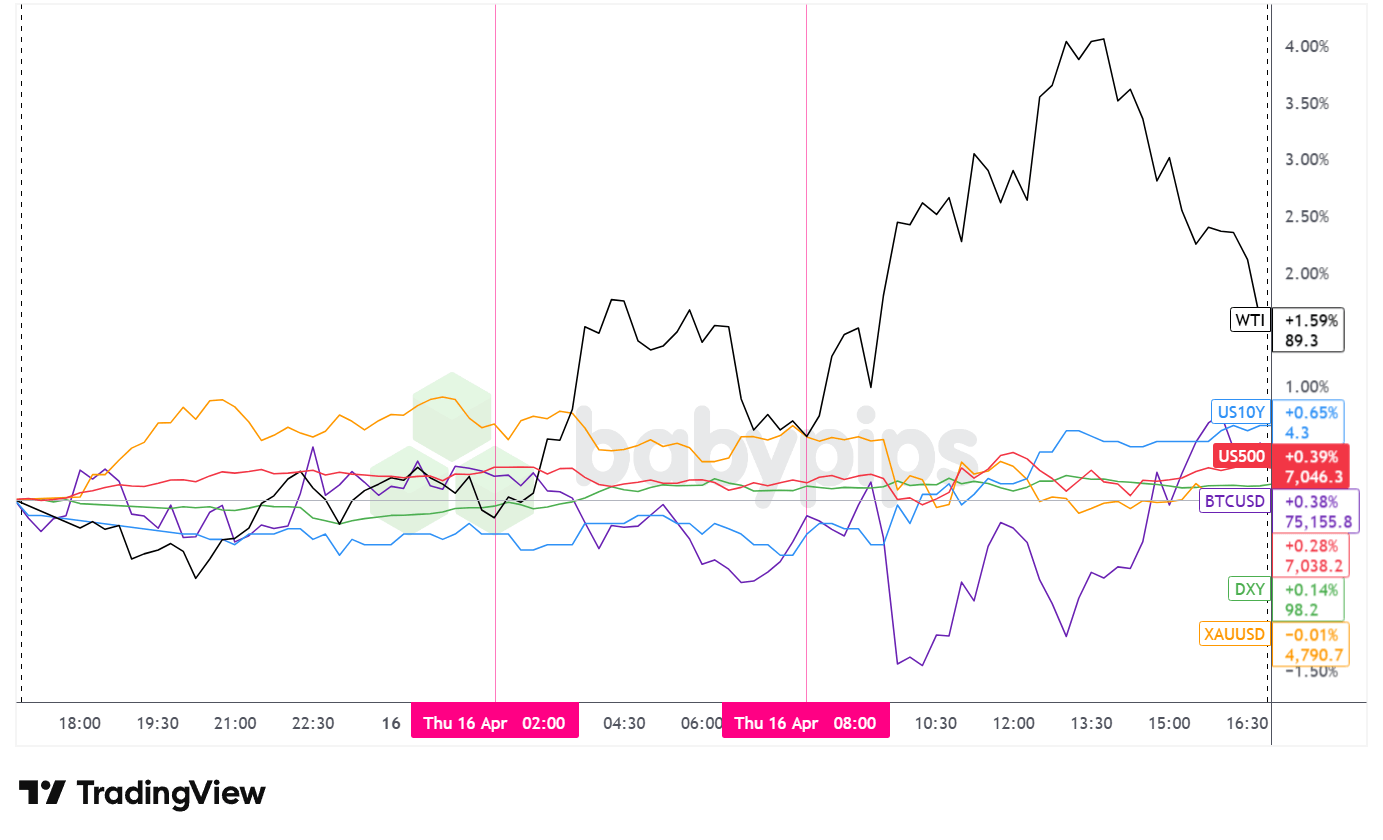

Broad Market Value Motion:

Greenback Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Sooner With TradingView

Thursday delivered one other constructive session for danger property, with equities and oil extending positive aspects towards a backdrop of incremental geopolitical de-escalation and a strong earnings beat from the semiconductor sector.

The S&P 500 closed at a recent all-time excessive, gaining 0.39% to settle at 7,046.0. The index opened the U.S. session close to flat earlier than bearish stress decrease across the 10:30 AM ET mark introduced value to an intraday low close to 7,017. The index recovered swiftly, surging to an intraday excessive above 7,051 round noon earlier than pulling again to shut close to 7,039. The intraday sample appeared to replicate the digestion of a heavy simultaneous knowledge slate, together with Philly Fed and preliminary jobless claims, earlier than bullish momentum resumed. The Nasdaq Composite logged its twelfth consecutive optimistic session, its longest profitable streak since July 2009, with expertise shares persevering with to profit from TSMC’s blockbuster first-quarter earnings that validated the AI infrastructure funding thesis.

WTI crude oil was the session’s strongest performer amongst broad property, advancing 159% to settle close to $89.30 per barrel. The transfer was notable given the constructive geopolitical backdrop, suggesting that offer considerations tied to the continuing U.S. naval blockade of the Strait of Hormuz doubtless continued to underpin crude costs even because the ceasefire framework slowly expanded. The rally started within the London session and prolonged into the U.S. morning, with value reaching a session excessive close to $91.76 earlier than easing into the shut.

Gold declined barely to settle close to $4,790 per ounce. After a gap bump greater, the valuable steel traded with relative stability by way of the Asian session earlier than starting a gradual downtrend that accelerated after the U.S. session opened, touching an intraday low close to $4,773. The transfer appeared broadly per the session’s risk-on tone, as investor urge for food for safe-haven property doubtless eased alongside the fairness rally and ceasefire headlines.

Bitcoin ended barely optimistic for the day, gaining 0.38% to commerce close to $75,155. The cryptocurrency traded with notable intraday volatility, dipping sharply towards the $73,300 space within the early U.S. session earlier than recovering firmly to shut close to its day by day highs. The uneven motion urged crypto markets have been delicate to the identical risk-on/risk-off swings seen throughout different asset courses all through the session.

The U.S. 10-year Treasury yield rose roughly 0.79% on the day to settle close to 4.31%. Yields have been largely subdued by way of the Asian and London classes however moved greater after the U.S. open, doubtless reflecting the Philly Fed’s vital beat on manufacturing and the robust new orders sub-index, alongside the below-forecast preliminary jobless claims print, which can have nudged merchants to mood near-term fee reduce expectations modestly.

Promotion: In case your confidence has grown in your market consciousness & methods with this market recap, and also you wanna take motion, Maven Buying and selling may also help. They supply simulated funding challenges beginning as little as $13, permitting you to commerce main pairs with professional-sized capital. No cut-off dates imply you may take swing performs on these market themes with out the stress of a ticking clock.

Be taught Extra About Maven Buying and selling In the present day!

Disclosure: We could earn a fee from our companions in case you enroll by way of our hyperlinks, at no further value to you.

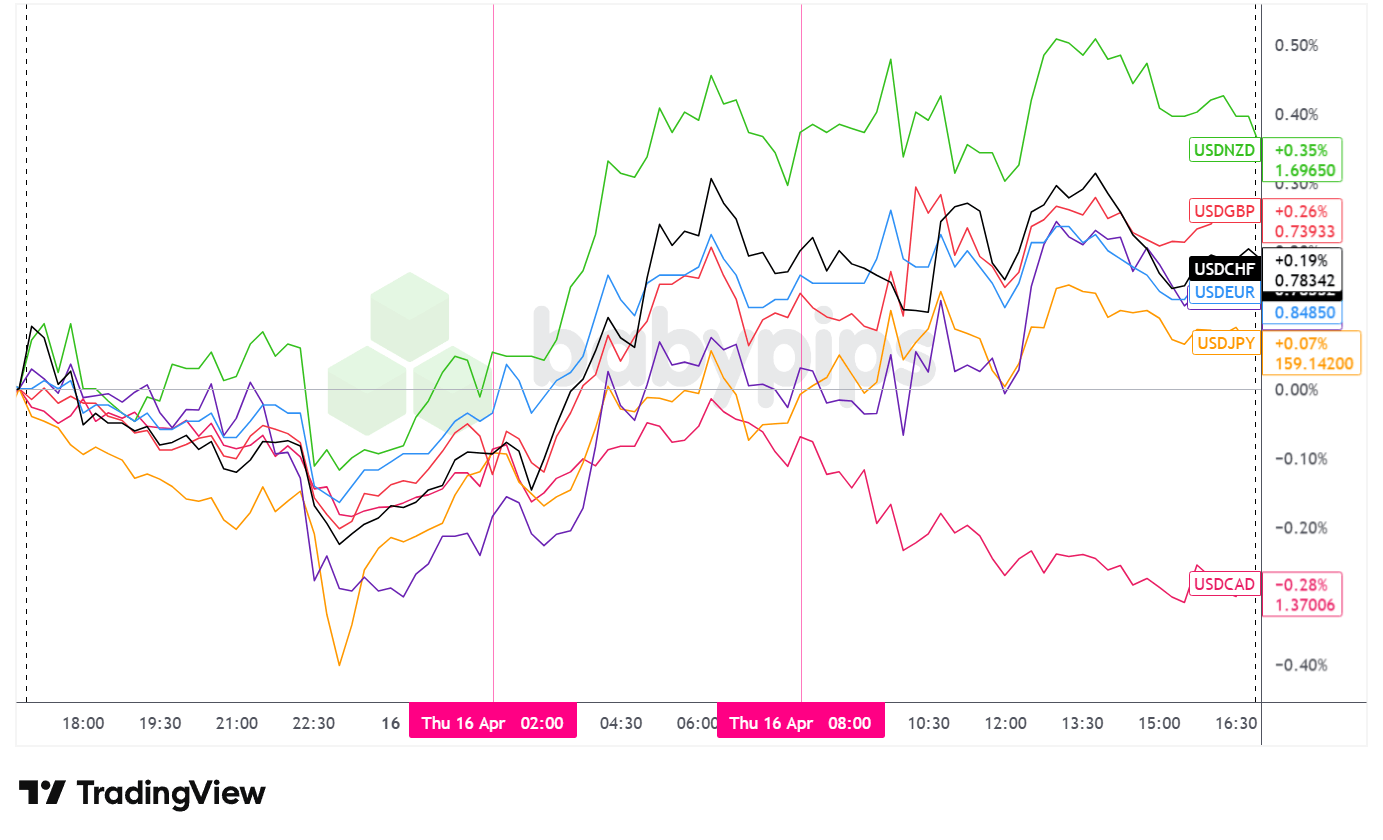

FX Market Conduct: U.S. Greenback vs. Majors

Overlay of USD vs. Majors – Chart Sooner With TradingView

The U.S. greenback closed Thursday as one of many session’s better-performing main currencies, ending the day greater towards all majors besides the Canadian greenback. The intraday journey concerned a number of distinct phases throughout the three most important buying and selling classes.

In the course of the Asian session, the greenback initially fell towards the most important currencies, doubtless reflecting the session’s tentative risk-on tone as Australia’s employment knowledge and China’s GDP crossed the tape alongside ongoing Iran ceasefire optimism. The Aussie obtained a modest carry from the roles report, which confirmed full-time employment surging 52.5k towards a 20.0k forecast even because the headline employment change fell in need of expectations, whereas China’s Q1 GDP progress of 5.0% year-over-year got here in barely beneath the 5.2% forecast. The greenback discovered a ground and started to stabilize, rebounding barely because the session transitioned towards Europe. Japan Finance Minister Katayama’s warning of potential “daring motion” in forex markets following talks with U.S. Treasury Secretary Bessent supplied some firming stress, nudging USD/JPY away from the 159 stage.

In the course of the London session, the greenback continued its rebound towards most main currencies earlier than topping out and pulling again barely because the U.S. session approached. European knowledge was broadly in line to modestly blended, offering restricted directional catalyst in isolation. The U.Okay. GDP print met expectations at 1.0% year-over-year, although manufacturing manufacturing continued to contract. Eurozone ultimate CPI got here in barely above the preliminary studying at 2.6% year-over-year, with core inflation holding at 2.3%. The ECB printed its financial coverage assembly accounts throughout this window, although no materials market response appeared to accompany the discharge. Swiss Nationwide Financial institution assembly minutes reiterated the coverage fee at 0% and flagged the franc’s safe-haven appreciation as a de facto tightening of financial circumstances. The SNB’s cautious tone could have tempered some franc demand on the margin.

After the U.S. session opened, the greenback traded with elevated intraday volatility, swinging in each instructions earlier than settling right into a internet optimistic posture for the rest of the session. The Philly Fed Manufacturing Index for April delivered a powerful upside shock at 26.7 towards the 17.0 forecast, with new orders surging to 33.0 from 8.6 and costs paid leaping to 59.3, pointing to accelerating exercise alongside constructing enter value pressures. Preliminary jobless claims fell to 207k towards a 216k forecast, suggesting the labor market stays resilient. These two releases doubtless supplied the elemental backdrop that allowed the greenback to agency by way of the afternoon. The sharp miss in U.S. industrial manufacturing for March at -0.5% month-over-month towards a +0.5% forecast was a counterpoint, although markets appeared to present higher weight to the forward-looking Philly Fed knowledge.

Upcoming Potential Catalysts on the Financial Calendar

- Australia Shopper Inflation Expectations for April 2026 at 1:00 am GMT

- Australia Employment Scenario Replace for March 2026 at 1:30 am GMT

- China GDP Development Price for March 31, 2026 at 2:00 am GMT

- China Unemployment Price for March 31, 2026 at 2:00 am GMT

- China Industrial Manufacturing for March 2026 at 2:00 am GMT

- China Retail Gross sales for March 2026 at 2:00 am GMT

- ECB Lane Speech at 3:40 am GMT

- U.Okay. Manufacturing & Industrial Manufacturing for February 2026 at 6:00 am GMT

- U.Okay. GDP for February 2026 at 6:00 am GMT

- Swiss Producer & Import Costs for March 2026 at 6:30 am GMT

- SNB Financial Coverage Assembly Minutes at 7:30 am GMT

- Euro space CPI Development Price Closing for March 2026 at 9:00 am GMT

- ECB Financial Coverage Assembly Accounts at 11:30 am GMT

- Canada New Motor Car Gross sales for February 2026 at 12:30 pm GMT

- U.S. Philadelphia Fed Manufacturing Index for April 2026 at 12:30 pm GMT

- U.S. NY Fed Providers Exercise Index for April 2026 at 12:30 pm GMT

- U.S. Preliminary Jobless Claims for April 11, 2026 at 12:30 pm GMT

- Fed Williams Speech at 12:35 pm GMT

- ECB Schnabel Speech at 1:00 pm GMT

- U.S. Industrial & Manufacturing Manufacturing for March 2026 at 1:15 pm GMT

Friday’s calendar is lighter on tier-one knowledge, however Fed audio system Barkin and Waller might provide significant market-moving commentary given the week’s blended alerts: robust Philly Fed exercise versus a mushy industrial manufacturing print, and continued labor market resilience working alongside still-elevated inflation danger. Any remarks on the trail of fee cuts, or the diploma to which the Iran battle’s power value affect is influencing the Fed’s inflation outlook, will doubtless draw dealer consideration.

On the geopolitical entrance, the sturdiness of each the U.S.-Iran ceasefire framework and the newly introduced Israel-Lebanon ceasefire will stay the dominant macro variable heading into the weekend, with oil pricing prone to stay delicate to any headline developments on both entrance.

Keep frosty on the market, foreign exchange pals!

Promoted: The Technique is Half the Battle; Your Mindset is the Relaxation.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ critiques on Amazon) Jack Schwager interviews profitable merchants to disclose a standard fact: their edge isn’t simply data or abilities—it’s their psychological resilience and inflexible danger management. Whether or not you’re navigating shifting geopolitical themes or high tier financial knowledge, learn the way the “wizards” keep medical when the remainder of the market is emotional.

Grasp Your Buying and selling Mindset with Market Wizards!

Disclosure: We could earn a fee from our companions in case you enroll by way of our hyperlinks, at no further value to you.