What Is Zero-Based mostly Budgeting?

Zero-based budgeting (ZBB) is a budgeting technique the place each rupee of earnings is assigned a function from a “zero base” every interval. Not like conventional incremental budgeting (which adjusts final yr’s numbers), ZBB requires justifying all bills from scratch for every new month or yr. In observe, you listing your whole earnings after which allocate each unit (greenback, rupee, and many others.) to bills, financial savings, or debt till the steadiness is zero. This implies on the finish of planning, earnings minus allocations equals zero – therefore “zero-based” budgeting. For instance, in case your month-to-month earnings is ₹60,000, you would possibly allocate ₹10,000 to lease, ₹6,000 to groceries, and many others., till no unassigned earnings stays.

Pete Pyhrr, a supervisor at Texas Devices, popularized zero-based budgeting within the Nineteen Seventies, and each people and firms have since used it to enhance value self-discipline. As one company finance useful resource explains, ZBB treats each expense as discretionary and requires a strategic justification for every line merchandise. In brief, ZBB forces you to “give each rupee a job” and determine forward of time the place it should go.

Why Use Zero-Based mostly Budgeting? (Advantages)

Zero-based budgeting provides unparalleled management and readability over your funds. Its advantages embody:

- Full Spending Visibility: By planning each expense, you get a clearer view of your monetary image. ZBB forces you to look at every value, so that you would possibly uncover you’re paying for unused subscriptions or duplicate providers. This will help eradicate wasted spending (e.g. a number of streaming providers).

- Intentional Financial savings: With ZBB, you “pay your self first” by allocating financial savings and investments in the beginning of budgeting. As a substitute of saving no matter is left, you determine upfront to place apart, say, 10–20% of earnings. This proactive method can increase financial savings charges and guarantee long-term targets (like emergency funds or retirement) are funded.

- Personalized Flexibility: Not like inflexible proportion guidelines (e.g. 50-30-20), ZBB is extremely adaptable. You set guidelines every month based mostly in your present wants. For instance, if earnings or priorities change, you’ll be able to reallocate funds with out mounted cut up guidelines constraining you. This flexibility can profit irregular-income earners (freelancers, gig staff) who want to regulate budgets often.

- Higher Determination-Making: By scrutinizing each class, ZBB promotes lively monetary decision-making and self-discipline. You deliberately plan indulgences (like eating out) quite than letting them occur by probability. This will curb impulse spending and assist keep on with monetary targets.

- Adaptable to Objectives: Since every rupee is purposeful, ZBB can speed up debt reimbursement or financial savings when wanted. For example, if aiming to repay an EMI quicker, you’ll be able to allocate additional rupees there first. This makes it a strong device for turning particular targets (debt freedom, down cost, and many others.) into motion plans.

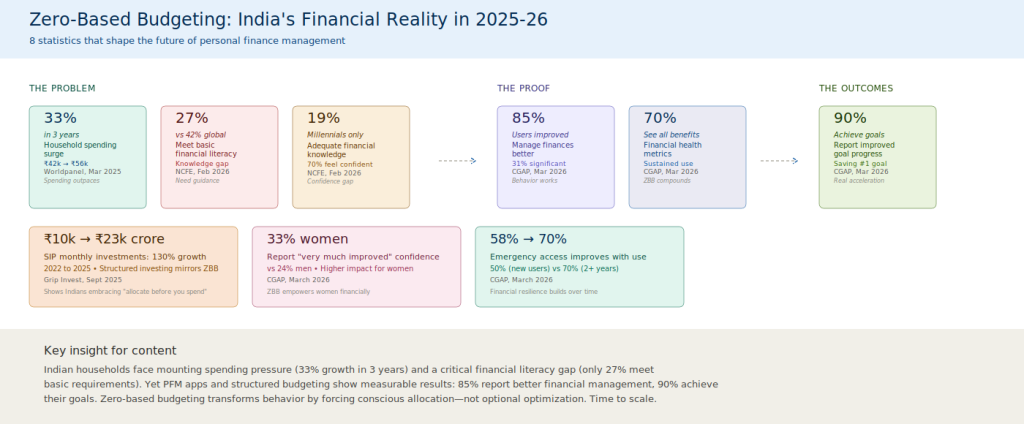

In abstract, ZBB offers you whole management over your cash and ensures each expense aligns together with your priorities. It promotes monetary self-discipline and helps uncover pointless spending. Many monetary planners and consultants in India suggest this technique for individuals who need the utmost readability and effectivity in budgeting.

Drawbacks of Zero-Based mostly Budgeting

Whereas highly effective, ZBB has some downsides to think about:

- Time-Consuming: Zero-based budgeting requires detailed planning and monitoring. You will need to listing each earnings supply and expense class and modify allocations exactly. Particularly at first, this could really feel labor-intensive.

- Can Be Inflexible: As a result of each rupee is pre-planned, ZBB could be much less versatile on a day-to-day foundation. If an sudden expense happens, you need to shuffle allocations or dip into an emergency fund (which ought to already be deliberate for, ideally).

- Hectic if Not Adopted: When you skip monitoring or overspend, ZBB can develop into advanced and unsustainable. Mint Cash warns that if not adopted, ZBB “turns into advanced” and loses its effectiveness.

- Not At all times Enjoyable: Some individuals might discover ZBB too strict. It requires you to say no to unplanned needs when you set the price range. This degree of self-discipline might not go well with everybody’s character or life-style.

- Attainable Overhead: For companies, ZBB could be bureaucratic (constructing many “determination packages” for every value). For people, utilizing a number of apps or spreadsheets can really feel like overhead.

Total, the cons boil right down to effort and self-discipline. ZBB works finest for these dedicated to thorough budgeting. When you favor extra free-wheeling strategies or don’t need to plan each element, less complicated techniques (just like the 50-30-20 rule) would possibly go well with you higher.

Methods to Create a Zero-Based mostly Price range: Step by Step

Implementing a zero-based price range is methodical. Right here’s a step-by-step course of you’ll be able to comply with:

- Checklist All Revenue Sources. Calculate your whole month-to-month earnings from each supply: wage, enterprise, curiosity, aspect gigs, and many others. Instance: Mr. P’s whole earnings is ₹60,000 (₹50,000 wage + ₹5,000 curiosity from FD + ₹5,000 tutoring). (See instance breakdown beneath.)

Determine: Instance breakdown of month-to-month earnings for a zero-based price range (supply: Gripinvest) - Checklist All Bills, Financial savings, and Money owed. Write down each expense class you could have. Embody mounted prices (lease, EMIs, utilities) and variable prices (groceries, eating, leisure). Additionally listing financial savings targets (emergency fund, mutual funds, and many others.) and debt funds. Don’t overlook occasional classes (insurance coverage premiums, items). Be complete.

- Mounted Bills: Lease/mortgage, mortgage EMIs, insurance coverage, subscriptions (Netflix, and many others.), faculty charges, utilities.

- Variable Bills: Meals, transport, procuring, leisure, journey.

- Objectives/Financial savings: Emergency fund, investments, trip fund, charity.

- Debt Reimbursement: Bank card payments, private loans, and many others.

- Allocate Each Rupee Till the Stability is Zero. Begin assigning your earnings to every merchandise on the listing. Usually:

- Cowl necessities first: Allocate mounted bills (lease, EMIs) totally. Allocate financial savings/debt subsequent: Resolve how a lot to avoid wasting or make investments and pay towards debt. It requires you to say no to unplanned needs when you set the price range. Assign remaining to variable or discretionary bills. Modify quantities in order that sum of all allocations equals your whole earnings. When you attain the top and have leftover earnings, allocate extra to financial savings or pay down debt additional. If allocations exceed earnings, you need to trim discretionary spending.

Proceed tweaking these numbers till Revenue – Complete Allocations = 0. In different phrases, each rupee is assigned. Instance (continued): Mr. P’s ₹60,000 is allotted as ₹10,000 lease, ₹6,000 groceries, ₹4,000 transport, ₹1,000 telephone, ₹10,000 investments, ₹5,000 leisure, ₹10,000 EMI, ₹12,000 emergency fund, and ₹2,000 financial savings account – totaling ₹60,000. Now his earnings left = 0.

- Monitor and Modify Month-to-month. Each month, evaluate precise spending towards the plan. When you under- or overspend in a class, modify the following month’s price range. ZBB encourages common evaluations so your price range stays lifelike. Use financial institution statements or apps to trace bills.

By following these steps every budgeting cycle (month-to-month or yearly), you guarantee each supply of cash is purposefully used. This course of might require effort initially, but it surely turns into faster as you get used to it.

Zero-Based mostly Budgeting vs Different Strategies

| Methodology | Core Precept | Greatest For | Execs | Cons |

|---|---|---|---|---|

| Zero-Based mostly Budgeting (ZBB) | Assign each rupee to an expense or objective; begin every interval from zero | Aggressive savers, debt paydown, seasoned planners | Most spending management; uncovers waste; adapts to altering wants | Time-consuming; requires strict monitoring and self-discipline |

| 50-30-20 Rule | 50% wants, 30% needs, 20% financial savings | Rookies, steady incomes | Easy, straightforward cut up; minimal monitoring | Might not match all life; much less exact |

| Envelope Budgeting | Mounted money limits for every spending class | Impulse spenders; visible learners | Sturdy curb on overspending in every class | Inconvenient with out money (or app); rigid as soon as envelope is empty |

| Incremental Budgeting | Construct on final interval’s price range with small adjustments | Conventional method; companies/governments | Simple to take care of if few adjustments; acquainted | Can perpetuate inefficiencies; little accountability |

Tailored options from Mint Cash and GripInvest. For instance, Mint’s evaluation exhibits ZBB provides “whole management of each rupee,” however requires “devoted monitoring”. In distinction, the 50-30-20 rule is simpler however much less tailor-made. Envelope budgeting caps spending successfully, however is usually finished with money or apps for every class. Every technique has trade-offs, so select based mostly in your targets and life-style.

Instruments, Apps, and Monetary Planners

You are able to do zero-based budgeting with paper, spreadsheets, or apps. Many digital instruments can simplify the method:

- Spreadsheets: Google Sheets or Excel templates permit full customization. You’ll be able to construct your individual ZBB template simply.

- Budgeting Apps: Apps like Goodbudget (envelope-style), Pockets, or Mint (US-based) could be tailored for ZBB by setting class budgets. In India, apps like Walnut or MoneyView assist monitor bills by linking financial institution accounts.

- Expense Trackers: Use apps or financial institution SMS alerts to observe spending in real-time.

- Calculators: On-line ZBB calculators (e.g. MintByte’s Zero-Based mostly Price range Calculator) can information the primary price range setup.

No matter instruments, consistency is vital. Monetary planning providers usually embody budgeting as a part of their choices. A licensed monetary planner or monetary guide in India will help arrange a zero-based price range aligned together with your targets. They will account for taxes, investments, insurance coverage, and many others., making certain you allocate every rupee successfully. When you really feel overwhelmed, contemplate in search of recommendation from a CFP or a good monetary advisor who provides budgeting steering.

ZBB in Enterprise and Authorities

Zero-based budgeting extends past private finance. Many corporations use ZBB for value administration. For instance, Bain & Firm notes that companies adopting ZBB can minimize their value base by ~25% and luxuriate in 150% greater returns over time. This exhibits how disciplined budgeting drives important financial savings and development. Nonetheless, company case research additionally warn: Kraft Heinz’s strict ZBB led to slicing innovation and model worth, whereas Unilever’s balanced “Save to Develop” method ring-fenced key initiatives and reinvested financial savings.

In India’s public sector, ZBB has been utilized too. In 2017, the federal government’s NITI Aayog carried out zero-based budgeting for nationwide schemes. This reform meant “each scheme should justify each rupee,” pruning outdated applications and reallocating funds to precedence initiatives like Digital India, GST rollout, and rural electrification. In different phrases, India shifted from incremental to zero-based budgeting to focus spending on outcomes and effectivity.

These examples spotlight that ZBB works for anybody – from households to massive organizations – who desire a rigorous framework for monetary decision-making.

Abstract of Key Factors

- Enterprise use: Firms and governments additionally apply ZBB to optimize prices (e.g. India’s 2017 price range reform).

- Zero-based budgeting (ZBB) means assigning each rupee of earnings a particular function, so earnings minus bills equals zero.

- Advantages: full management and readability of spending, intentional saving first, and tailor-made budgeting (no unallocated money).

- Drawbacks: requires extra time and self-discipline; could be inflexible and sophisticated if not maintained.

- Implementation: 1) Checklist all earnings sources, 2) Checklist bills (mounted/variable), financial savings and money owed, 3) Allocate funds to every merchandise till whole equals earnings.

- Comparability: Not like the 50-30-20 rule or incremental budgeting, ZBB offers maximal management however calls for detailed monitoring. It’s ultimate for debt discount or goal-focused savers, whereas less complicated strategies might go well with informal budgets.

- Skilled recommendation: Monetary planners and monetary planning providers in India usually use ZBB ideas. A licensed monetary guide can help in customizing your price range.

FAQs About Zero-Based mostly Budgeting

Q: What’s zero-based budgeting?

A: Zero-based budgeting (ZBB) is a technique the place you price range from scratch every interval, assigning each rupee of earnings to particular bills, financial savings, or money owed in order that earnings minus allocations equals zero.

Q: How do I begin a zero-based price range?

A: First, calculate your whole month-to-month earnings. Then listing all bills (lease, payments, groceries, and many others.), plus financial savings and debt funds. Allocate your earnings to every merchandise till no cash is left unassigned. Use a spreadsheet or app to assist monitor classes.

Q: What are the advantages of zero-based budgeting?

A: ZBB supplies most management over spending. It helps establish waste, ensures you save first, and aligns spending with targets. It additionally adapts simply to altering earnings or priorities.

Q: What are the disadvantages of zero-based budgeting?

A: It may be time-consuming and requires self-discipline. You will need to plan intimately and monitor bills intently. When you lose focus, the tactic can develop into cumbersome or collapse.

Q: When ought to I exploit zero-based budgeting?

A: ZBB is finest once you want strict management—corresponding to when paying off debt, saving aggressively, or managing irregular earnings. It’s particularly helpful for those who discover cash slipping away and need to perceive precisely the place each rupee goes.

Q: How does zero-based budgeting differ from the 50-30-20 rule?

A: The 50-30-20 rule units mounted percentages for wants (50%), needs (30%), and financial savings (20%). ZBB, in contrast, includes zero-based allocation with out preset ratios. ZBB can accommodate completely different percentages every month, giving extra flexibility however requiring extra effort.

Q: Can I do zero-based budgeting alone?

A: Sure, anybody can implement ZBB. Nonetheless, consulting a monetary planner or monetary guide could be useful for personalised steering, particularly to deal with tax, funding, and long-term monetary planning facets.

Q: What if my earnings adjustments month to month?

A: With variable earnings, you’ll be able to nonetheless use ZBB by first setting a baseline price range based mostly on anticipated earnings, then adjusting allocations every month. At all times cowl mounted wants first, and modify needs/financial savings if earnings is decrease.

Q: Is there software program for zero-based budgeting?

A: Many budgeting apps (Goodbudget, YNAB, and many others.) and spreadsheets can be utilized for ZBB. Some on-line calculators (e.g. MintByte) additionally exist. The secret is monitoring each expense class till the price range balances to zero.