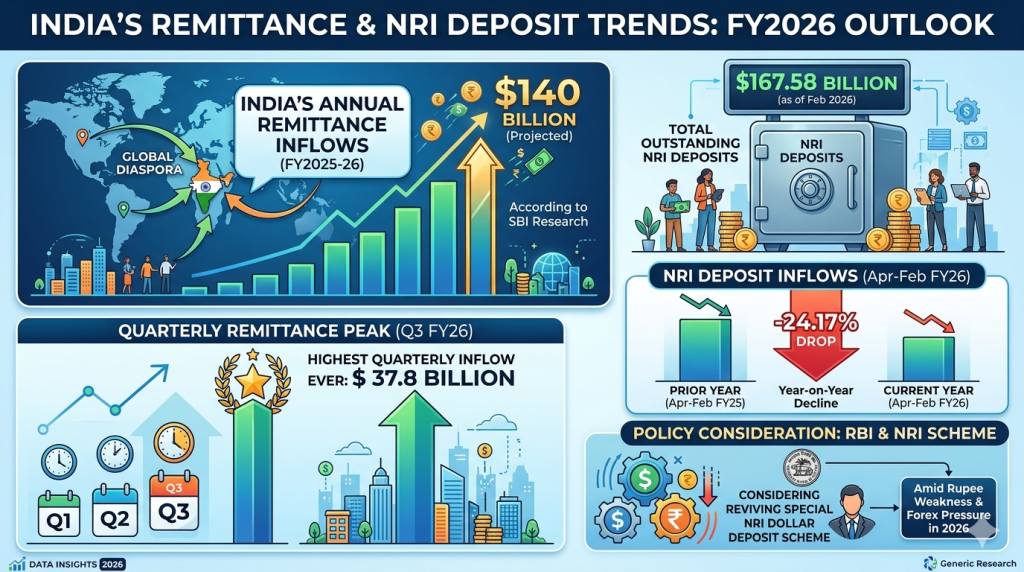

Monetary planning is a complete course of overlaying earnings, financial savings, investments, retirement, and taxes. For NRIs, this course of isn’t elective – it’s non-negotiable . An NRI (Non-Resident Indian) is outlined as an Indian citizen residing overseas . There are roughly 17.17 million NRIs worldwide , and their remittances reached about US$138 billion in FY2025 . This large capital movement highlights why clever NRI monetary planning is so essential. NRIs juggle overseas forex earnings with Indian monetary wants, face strict tax guidelines, and should navigate repatriation limits. With out professional steering, rising wealth effectively, minimizing taxes, and guaranteeing compliance can turn out to be chaotic .

Why NRI Monetary Planning Issues

Managing cash throughout borders creates distinctive challenges. NRIs earn in USD, EUR, AED or different currencies however usually have liabilities in INR (household bills, property, training). A globally diversified portfolio helps handle this mismatch relatively than amplify it . For instance, the USD and GBP have steadily strengthened versus the rupee over years , so holding some dollar-denominated belongings can enhance returns. NRIs additionally face completely different tax regimes overseas and in India, together with reporting necessities (TDS, DTAA) . Moreover, strict FEMA (Overseas Alternate Administration Act) guidelines govern how and when funds can transfer throughout borders. In brief, NRIs should stability two monetary worlds – and failure to plan upfront can result in extreme taxes, compliance penalties, and missed alternatives .

Key challenges embrace: forex fluctuations (impacting financial savings and investments), tax residency guidelines (e.g. the brand new 120-day rule for high-income Indians overseas ), twin taxation treaties (DTAA), and repatriation caps (USD 1 million per yr from NRO accounts ). With out a tailor-made plan, an NRI would possibly endure from over-deducted TDS on property sale or curiosity , idle rupee funds eroding in low-interest accounts , or household emergencies hampered by blocked funds. Efficient NRI monetary planning turns complicated cross-border laws into benefits – for instance, leveraging tax exemptions, choosing the proper funding autos, and timing transfers optimally.

Key Concerns for NRI Monetary Planning

Residency & Taxation Guidelines

Indian tax regulation hinges in your residency standing. Current adjustments make this particularly complicated. Historically, an Indian who stayed lower than 182 days in India was an NRI (non-resident Indian). Now, a 120-day rule additionally 9 applies for high-income people, making extra individuals tax-resident even with quick visits . The particular 11 class RNOR (Resident however Not Ordinarily Resident) has additionally turn out to be widespread for returning NRIs . RNOR standing taxes NRIs on overseas earnings extra favorably for a restricted interval – a useful planning window if used appropriately.

Key tax factors for NRIs:

• Scope of earnings: NRIs are taxed in India solely on earnings acquired or accrued in India . Nevertheless, international authorities now usually hint offshore earnings through data-sharing. Even non disclosable earnings might have reporting .

• TDS (Tax Deducted at Supply): NRI earnings (curiosity, rents, property sale) faces greater TDS charges (e.g. as much as 30% on capital positive aspects) . Over-deduction is widespread, so NRIs ought to file ITR (Revenue Tax Return) to assert refunds .

• DTAA: India has DTAA agreements with many nations. NRIs ought to acquire a Tax Residency Certificates (TRC) and declare treaty advantages to keep away from double taxation .

• Reporting: Overseas belongings disclosure is obligatory should you qualify as resident in any yr . The 2026 Price range launched a one-time disclosure window (FAST-DS 2026) for small unreported overseas belongings, easing penalties.

Staying knowledgeable on these guidelines (and adjustments from the most recent funds) is significant. As an example, Price range 2026 prolonged the deadline for belated tax returns and decriminalized minor defaults – helpful aid for busy NRIs. Seek the advice of a certified adviser or CA to make sure your tax standing is appropriate and filings are well timed.

NRE, NRO & FCNR Accounts Defined

Correct checking account construction is the spine of NRI planning. Reserve Financial institution of India (RBI) guidelines provide three fundamental rupee accounts for NRIs:

- NRE (Non-Resident Exterior) Account: Overseas earnings (wage, dividends from overseas) might be remitted into an NRE account. It earns tax-free curiosity in India, and each principal and curiosity are absolutely repatriable . NRE accounts should be maintained in INR however are funded by overseas forex.

- NRO (Non-Resident Strange) Account: Indian-sourced earnings (rental, pension, dividends from Indian firms) goes into an NRO account. Curiosity earned is taxable (round 30%) . Repatriation from an NRO account is capped at USD 1 million per monetary yr for all capital receipts mixed . Exceeding this restrict requires RBI permission.

- FCNR (Overseas Forex Non-Resident) Account: These are fastened deposits in overseas forex (USD, EUR, GBP, and many others.). They provide full reparability and tax-free curiosity, insulating you from rupee volatility. FCNRs lock in greater curiosity (1–5 years tenures) with out INR danger.

| Function | NRE/FCNR (Repatriable) | NRO (Non-Repatriable) |

| Supply of Funds | Overseas earnings solely | Indian earnings (hire, dividends, and many others.) |

| Repatriation | Limitless transfers overseas (full freedom) | ₹1 crore (~USD1M) cap/yr |

| Curiosity Tax | Tax-free in India | Taxed at ~30% (TDS applies) |

| Use Case | Keep abroad earnings, repatriate anytime | Park Indian earnings, topic to limits |

| Funding Hyperlink | Eligible for PIS buying and selling in fairness markets | Investments through NRO solely |

NRIs usually keep each NRE/FCNR and NRO accounts to separate overseas and Indian incomes. All the time route overseas remittances (wage, items from overseas) into NRE/FCNR accounts to maintain them absolutely repatriable. Use the NRO account for native earnings, maintaining in thoughts the $1M repatriation rule.

Documentation: Changing and working these accounts entails paperwork. To repatriate from an NRO account, you usually want Kind 15CA/CB (tax certificates by a CA) and a financial institution switch request. NRE/FCNR transfers require a easy request and Kind A2 (declaration type). Hold copies of passports, PAN card, and proof of remittance. Correct documentation avoids delays.

Funding Choices for NRIs

NRIs have entry to just about all funding autos obtainable to residents – plus abroad choices. Selecting the right combination is essential for wealth progress and tax effectivity:

- Equities (Shares, ETFs): NRIs can make investments straight in Indian inventory markets through a Portfolio Funding Scheme (PIS). This requires an NRE (PINS) demat account for fairness buying and selling . IPO subscriptions are allowed from NRE/NRO accounts. US/NRI-specific restrictions apply (e.g. NRIs from the USA/Canada should adjust to FATCA) . Traditionally, fairness delivers excessive returns; international diversification into US or different markets can add stability and forex positive aspects .

- Mutual Funds: Fairness, hybrid, and debt mutual funds are a well-liked selection. NRIs can make investments lump sum or through SIP by their NRE/NRO accounts . Observe: NRIs from FATCA-reporting nations could also be restricted from some funds . Professionals: Skilled administration, simple diversification. Cons: Exit load (for early withdrawal) and capital positive aspects tax on items (handled as capital positive aspects earnings).

- Mounted Deposits & Bonds: Indian FDs (in NRE/NRO) and foreign-currency FCNRs provide fastened returns. Authorities-backed choices like RBI’s Retail Direct (G-Sec account) or PSU bonds (e.g. NTPC, PFC) give steady earnings and tax advantages . NRE/NRO FDs have 1–5 yr tenures with fastened curiosity; NRE FD curiosity is tax-exempt. NRIs may also discover Tax-Free Bonds (topic to issuance) and company NCDs. Instance: In NRE/FCNR accounts, funds can earn as much as ~5–6% in long-term deposits, maintaining tempo with inflation.

- Public Provident Fund (PPF): NRIs can proceed present PPF accounts however can’t open new ones. Contributions until maturity are allowed (curiosity is tax-free).

- Nationwide Pension System (NPS): NRIs (18–70 years) can open Tier I NPS accounts. They provide market-linked returns and partial tax advantages. No contemporary investments in Tier II for NRIs.

- Actual Property: NRIs should buy residential or business property in India (agricultural land is prohibited). Properties funded by NRE/FCNR are absolutely repatriable. Property earnings will likely be taxed (with TDS on rents and LTCG at 12.5%). Actual property usually supplies good returns, however watch illiquidity, upkeep, and household strain as pitfalls.

- Gold: Bodily gold, gold ETFs or mutual funds are allowed investments. Sovereign Gold Bonds can’t be newly purchased by NRIs, however present holdings might be held to maturity.

- Different Belongings: Excessive-net-worth NRIs additionally put money into PMS (Portfolio Administration Companies), AIFs (Different Funding Funds), personal fairness and REITs . These can enhance returns however carry greater danger and lock-in intervals.

- Asset Allocation: Align your portfolio with danger tolerance and targets. Many NRIs profit from international diversification: combining Indian belongings with US/UK equities or worldwide funds . This not solely spreads danger however can seize positive aspects from a stronger overseas forex. For instance, US equities may buffer a weak rupee, as U.S. markets contributed ~28% of India’s remittances progress lately . A balanced combine (shares, debt, actual property) and periodic assessment is really useful

Repatriation Guidelines & Documentation

Shifting cash between India and overseas should comply with RBI/FEMA guidelines:

- From NRE/FCNR: Funds (principal + curiosity) are absolutely repatriable with out limits. NRIs merely submit a financial institution request with Kind A2 (objective declaration). Processing is often fast (3–7 days).

- From NRO: Solely as much as USD 1,000,000 might be despatched overseas per monetary yr, overlaying all capital receipts (sale of property, investments). To repatriate past INR 50,000, you’ll want:

- A stuffed financial institution switch request type.

- Kind 15CA (self-declaration of tax cost).

- Kind 15CB (chartered accountant’s certificates confirming taxes are paid on the quantity).

- Passport/visa copies and PAN (tax ID). Banks usually deal with components of this course of, however lacking docs can delay transfers

- Key tip: Keep clear information of the supply of funds (sale deeds, dividend slips), and all the time file tax returns. A CA certificates (15CB) prices ~₹5,000–₹25,000 relying on quantity. Failing to conform can set off RBI queries or penalties.

Current Price range & Regulatory Updates

Keep up to date on coverage adjustments affecting NRIs. The 2026–27 Indian Price range launched a number of NRI-friendly reforms:

- Tax Reduction: Small undisclosed overseas belongings (as much as ₹20 lakh) now keep away from prosecution. Eligible NRIs underneath presumptive tax can skip MAT

- TCS on Remittances: TCS (Tax Collected at Supply) on LRS remittances for training/medical diminished from 5% to 2%. Abroad tour bundle TCS additionally lower to 2%

- Versatile Compliance: The deadline for belated/revised ITRs has been prolonged to March 31. Small procedural defaults have been decriminalized.

- FAST-DS 2026: A one-time amnesty for unreported overseas belongings; pay due tax and curiosity with no penalty or prosecution.

- Property Transactions: No TAN (Tax Deduction Account Quantity) wanted when NRIs purchase/promote property, simplifying paperwork.

- Capital Markets: Simpler entry for NRIs, decrease compliance burdens (particulars TBD).

Annually’s updates (particularly Price range 2026) can influence how NRIs make investments and file taxes. For instance, the FAST-DS permits NRIs to “come clear” on overseas earnings with out concern. It’s smart to seek the advice of up to date authorities releases (Ministry of Finance/Price range) and your advisor yearly.

The Function of Monetary Planners and Advisors for NRIs

Navigating cross-border finance requires professional steering. A monetary planner or NRI monetary advisor understands each Indian laws and international finance. They tailor methods that stability your abroad earnings with Indian targets. Key advantages of an expert NRI advisor embrace :

- Custom-made Targets & Methods: They align your investments with life targets (retirement in India, children’ training, property) and assess international publicity. This goes past generic recommendation – it’s a strategic highway map on your distinctive state of affairs.

- Funding Portfolio Design: Advisors assist diversify throughout asset lessons (shares, mutual funds, bonds, AIFs, actual property, and many others.) and geographies. For instance, as an alternative of maintaining all financial savings in a 8 low-interest NRO account, an adviser can shift extra money into higher-yield investments.

- Tax & Compliance Administration: The largest headache for NRIs is usually taxes in two nations. A educated advisor helps apply DTAA treaties to keep away from double tax, ensures you file appropriate ITR varieties, and interprets new tax legal guidelines. In addition they guarantee each FEMA guideline is adopted (e.g. appropriate use of NRE vs NRO).

- Repatriation Planning: Advisors simplify fund transfers. They know the documentation (15CA/CB, Kind A2) and optimum timing (e.g. changing earnings when rupee is favorable). They coordinate with banks and tax specialists to make repatriation hassle-free.

- Wealth Consolidation: Many NRIs have scattered belongings (India and overseas). A planner consolidates all holdings, giving a single-window view of internet price. Common reviews and evaluations maintain you on observe and knowledgeable.

In brief, a very good advisor is absolutely fee-based (SEBI-registered) and legally certain to your pursuits. They exchange guesswork with tailor-made options, saving you from pricey errors (like violating RBI norms or lacking a tax credit score). For NRIs with important Indian belongings, hiring an skilled NRI monetary marketing consultant is very really useful.

Step-by-Step NRI Monetary Planning Course of

A disciplined course of ensures nothing is neglected. Right here’s a sensible roadmap:

- Decide Your Residency Standing: Examine present and upcoming keep durations. Do you qualify as NRI, RNOR, or Resident? Your residential standing impacts how India and overseas nations tax your earnings.

- Set Clear Monetary Targets: Outline short-term (e.g. emergency fund, trip), mid-term (little one’s faculty, dwelling downpayment), and long-term (retirement, inheritance) targets. Tie every purpose to a greenback quantity and timeline.

- Stock All Belongings: Listing all financial institution accounts, investments, properties (India and overseas). Observe account sorts (NRE/NRO), and examine KYC standing. Replace nominees for every asset to keep away from property points.

- Optimize Financial institution Accounts: Open or convert to NRE/FCNR accounts for overseas earnings; keep an NRO for Indian earnings. Guarantee you have got PIS demat accounts if planning fairness trades.

- Construct an Funding Plan: Allocate belongings per danger urge for food and targets. Think about forex hedging (e.g. FCNR for forex danger) and international diversification For instance, maintain some USD or EUR investments to stability INR bills.

- Tax Technique: Use DTAAs and exemptions. Construction investments to scale back TDS (e.g. investing in sure infrastructure bonds for tax breaks). Plan your repatriation to reduce tax leaks (with correct documentation).

- Insurance coverage and Safety: Buy ample life, well being, and property insurance coverage in India if household is dependent upon you. Lock in decrease premiums whereas younger and wholesome.

- Property and Succession Planning: Draft an Indian will overlaying Indian belongings. The shortage of 1 is a typical NRI mistake. Replace your life insurance coverage nominees frequently.

- Put together for Repatriation: If planning to return (partially or absolutely), begin restructuring 1–2 years upfront. Promote or convert belongings earlier than standing adjustments; type a rupee money reserve to clean the transition.

- Overview and Regulate Commonly: Legal guidelines change usually (e.g. Price range updates); so do markets. Overview your plan yearly (or upon main life occasions) together with your advisor.

Utilizing this step-by-step guidelines helps keep away from last-minute panic. Bear in mind, NRI planning is ongoing – what works immediately (NRE yields, tax legal guidelines) might shift subsequent yr.

Frequent Errors and Greatest Practices for NRIs

Even sensible professionals slip up with out a plan. Listed below are frequent pitfalls to keep away from:

- Idle NRO Balances: Maintaining massive sums in an NRO financial savings account (incomes ~3–4%) whereas inflation runs 5–6% silently erodes wealth. As a substitute, transfer surplus NRO cash into FDs, bonds, or mutual funds.

- Over-Investing in Actual Property: Shopping for a number of properties (usually because of household strain) can backfire. Actual property is illiquid and comes with upkeep prices and decrease post-tax returns. Think about REITs (actual property funds) for liquidity as an alternative.

- Neglecting Property Planning: Not updating nominees after marriage/divorce or a dad or mum’s loss of life results in authorized complications. All the time maintain your will and nominee particulars present.

- Not Adjusting on Standing Change: When your standing shifts (NRI → RNOR → Resident), tax implications change. Failing to reallocate investments throughout this transition can set off sudden taxes.

- Blindly Following Recommendation: Keep away from taking inventory suggestions from unverified sources (WhatsApp teams, social media). Generic “scorching” recommendation ignores your distinctive state of affairs and might be dangerous.

- Final-Minute Planning: The costliest errors occur proper earlier than returning to India. Don’t wait till visa renewal or flight bookings – begin monetary restructuring 1–2 years upfront.

- Ignoring Skilled Assist: Attempting to DIY complicated cross-border funds usually results in compliance errors. Companion with a certified monetary planner who makes a speciality of NRIs.

By sticking to greatest practices – clear targets, diversified portfolio, compliance, and professional recommendation – you flip these dangers into alternatives.

Abstract

- NRI monetary planning is essential for Indian expats. NRIs face twin tax regimes, forex danger, and strict FEMA guidelines

- Know your tax/residency standing. The brand new 120-day rule and RNOR standing imply you have to calculate Indian tax residency rigorously. File ITR to assert TDS refunds and use DTAA treaties.

- Use the appropriate accounts: Route overseas earnings into NRE/FCNR accounts (tax-free curiosity, full repatriation). Park Indian earnings in NRO (₹1 Cr repatriation cap, taxed curiosity).

- Diversify investments: Allocate throughout Indian equities, mutual funds, fastened earnings, and international belongings. NRIs’ foreign-currency earnings might be a bonus if invested properly (e.g. US shares acquire when USD strengthens).

- Plan repatriation & compliance: Perceive Types 15CA/CB and FEMA limits. Hold documentation (PAN, contracts, CA certificates) able to keep away from delays.

- Monitor adjustments: Sustain with Price range 2026 reforms and RBI tips. New measures (like FAST-DS 2026) can provide tax aid for NRIs.

- Work with specialists: A licensed monetary planner/marketing consultant educated in NRI finance can tailor a holistic plan. They deal with asset allocation, goal-setting, DTAA software, and regulatory compliance.

In abstract, NRI monetary planning requires a transparent technique and common assessment. Use your worldwide benefit properly: diversify globally, leverage tax treaties, and maintain funds accessible. By avoiding widespread errors and looking for skilled steering, NRIs can obtain monetary targets with confidence.

FAQs

What’s NRI monetary planning and why is it necessary?

NRI monetary planning entails managing cross-border funds – investments, taxes, and authorized compliance – for Non-Resident Indians. It will be important as a result of NRIs should juggle two tax methods, forex variations, and repatriation guidelines. Good planning turns these complexities into advantages (like tax exemptions and diversified portfolios) and prevents pricey errors

How do NRE and NRO accounts differ?

NRE accounts (Non-Resident Exterior) are for foreign-sourced earnings: they maintain INR however are funded by abroad earnings. NRE account curiosity is tax-free in India and funds are absolutely repatriable anytime. NRO accounts (Non-Resident Strange) maintain earnings earned in India. Banks tax NRO curiosity at round 30%, and account holders can repatriate solely ₹1 crore per yr. Use NRE for overseas earnings and financial savings you would possibly want overseas, NRO for Indian rental/dividend earnings.

What funding choices can be found for NRIs in India?

NRIs can put money into most Indian belongings: equities (shares and ETFs through an NRE/PIS demat account), mutual funds (debt, fairness, hybrid through SIPs or lumpsum), fastened earnings (NRE/NRO fastened deposits, bonds, G-Secs through RBI’s retail direct) , and even PPF/NPS (with some restrictions). They will additionally purchase residential/business actual property and gold (ETFs or bodily). World NRIs usually diversify with overseas equities for forex advantages

How do NRIs deal with taxes and repatriation?

NRIs file Indian tax returns (ITR-2 or 3) on earnings from India. Most earnings sources, similar to hire, curiosity, and property positive aspects, deduct TDS, so taxpayers usually declare refunds. Below DTAAs, taxpayers may also declare credit score for taxes paid overseas. For repatriation, NRE/FCNR funds can go abroad anytime. NRO funds require Types 15CA/CB and are topic to a $1M/yr restrict. Sustaining compliance and documentation (PAN, passport, CA certificates) is essential to clean transfers.

Why ought to I exploit a monetary planner for NRI planning?

As a result of cross-border finance is complicated. A certified NRI monetary planner or marketing consultant supplies customized recommendation on asset allocation, tax optimization, and compliance. They assist align your international earnings and Indian obligations together with your targets. For instance, they make sure you use DTAA to keep away from double tax, select the right combination of investments (native vs international), and regulate your technique when legal guidelines change. This experience usually saves time and money in comparison with DIY planning.

Are overseas earnings and abroad positive aspects taxable for NRIs in India?

Typically, an NRI is taxed in India solely on Indian-sourced earnings (Indian rents, salaries, capital positive aspects on Indian belongings). Overseas earnings (e.g. UK wage) is often not taxable in India for a non-resident, supplied your standing stays NRI (not RNOR or resident) and also you don’t meet these new residency assessments. Nevertheless, underneath the brand new guidelines, even overseas holdings should be disclosed, and RNOR standing can create exceptions. All the time affirm your residential standing and declare DTAA advantages to keep away from twin taxation.