Where Will Enbridge Stock Be in 3 Years?

Stock · July 15, 2026

Income investors won’t soon forget the mishaps in the Canadian telecommunications sector that culminated in a massive dividend cut in 2025. For decades, BCE (TSX:BCE) stock was once one of the most stable dividend stocks on the TSX — a reliable blue-chip income generator that investors bought, tucked away, and ignored. That perception shattered when macro pressures and fragile balance sheets forced BCEâs management to hand shareholders a staggering 56% dividend cut in May last year. Its double-digit dividend yield crashed down to earth.

But if you thought the drama was completely over, recent market volatility had other plans. BCE stock shed 12.4% of its value during the past month, plunging to May-2025 multi-year lows and pushing its dividend yield right back into focus as the current yield rises to 5.8%.

So, what exactly is going on with BCE stockâs dividend today? Is this renewed slide a warning sign of another impending cut, or is it a classic value-investing window? Letâs dive in.

First, letâs clear up why BCE stock, alongside industry peers TELUS and Rogers Communications, experienced a sector-wide decline during the past month. The primary culprit wasn’t a sudden operational flaw in the Canadian telecommunications sector; it was noise. Specifically, overblown speculation surrounding the SpaceX stock IPO ignited fears that the Elon Musk-led satellite internet giantâs expansion plans may evolve into a wireless carrier, introducing formidable competition.

Those fears appear highly exaggerated for Canadian carriers. The Canadian telecommunications sector is protected by a deeply entrenched economic moat. Regulatory barriers, spectrum unavailability, and market size constraints mean SpaceX faces immense barriers to entry in Canada.

More importantly, the underlying telecom market health is quietly improving. The severe retail price war that compressed wireless margins during the first quarter of 2026 vanished during the second quarter. With rational pricing returning to the market, BCEâs core business is structurally healthier than the stock price suggests.

An investment thesis on BCE stock today expands beyond its traditional cellular networks and media assets into its massive, forward-looking transformation into an artificial intelligence (AI) infrastructure powerhouse.

In March 2026, BCE officially re-entered the data center space with a transformational announcement: the construction of a new 300-megawatt AI Fabric data centre campus just outside Regina, Saskatchewan. Once complete, it will be the largest purpose-built AI data centre facility in Canada. Instead of trying to navigate this massive tech pivot alone, BCE has already secured ultra-heavyweight hyperscalers CoreWeave (utilizing NVIDIA GPUs) and Cerebras (providing its revolutionary wafer-scale technology) as core anchor tenants.

Through its enterprise subsidiary, Ateko, BCE snapped up Calgary-based data engineering firm SDK Tek Services to bolster its data analytics capabilities. Flanked by high-profile partnerships with Cohere, Hypertec, and BUZZ HPC (a subsidiary of Hive Digital Technologies), BCE is constructing a comprehensive “Sovereign AI” ecosystem.

By keeping computing workloads strictly within Canadian borders, BCE could secure a competitive advantage for high-security public sector, government, and corporate enterprise contracts.

The AI initiatives establish growth momentum, with management aggressively raising its scaling targets for the segment as data centre construction gets underway.

Building the future of Canadian tech infrastructure requires serious capital. To fund the construction of the Saskatchewan campus, BCE is injecting $1.7 billion in incremental capital expenditures, with a massive $1.3 billion hitting the books during 2026 alone.

This aggressive spending spike means free cash flow (FCF) will temporarily suffer. For passive-income seekers, this is a crucial variable: because cash is being heavily funnelled into high-margin AI infrastructure, you shouldn’t expect a return to dividend growth anytime soon.

Unlike the precarious financial position BCE stock found itself in back in 2022 when macro crosswinds exposed fragile cash flow statements, the company has stabilized its ship.

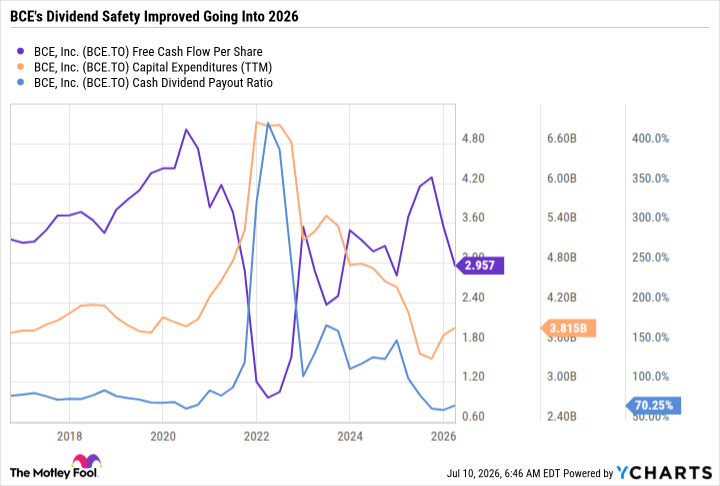

Thanks to the original 2025 payout reset, lower capital expenditures and better free cash flow per share, BCE stock’s trailing 12-month (TTM) cash dividend-payout ratio has dropped to a far more sustainable 70.3%.

BCE Free Cash Flow Per Share data by YCharts

Furthermore, the heavy 2026 data centre capital expenditures are structured to be leverage-neutral. While the company fortifies its balance sheet over the next few years, the risk of a further dividend cut remains remarkably low.

The post What Is Going On With BCEâs Dividend? appeared first on The Motley Fool Canada.

Before you buy stock in Bce, consider this:

The Motley Fool Canada team has identified what they believe are the top 10 TSX stocks for 2026⦠and Bce wasnât one of them. The 10 stocks that made the cut could potentially produce monster returns in the coming years.

Consider MercadoLibre, which we first recommended on January 8, 2014 … if you invested $1,000 in the âeBay of Latin Americaâ at the time of our recommendation, youâd have over $17,000!*

Now, it’s worth noting Stock Advisor Canada’s total average return is 97%* – a market-crushing outperformance compared to 88%* for the S&P/TSX Composite Index. Don’t miss out on our top 10 stocks, available when you join our mailing list!

Get the 10 stocks instantly* Returns as of July 6th, 2026

More reading

Fool contributor Brian Paradza has no position in any of the stocks mentioned. The Motley Fool recommends Nvidia, Rogers Communications, and TELUS. The Motley Fool has a disclosure policy.