Gold has had its second in 2025, up 137.4% 12 months thus far. Canadian traders who acquired gold shares early in 2025 might be sitting on triple-digit good points to this point this 12 months, regardless of the safe-haven asset’s slight pullback from all-time highs printed in October. It’s solely prudent to take some revenue from the worry (gold) commerce and rotate capital into the subsequent development and industrial trades for the subsequent commodity cycle.

Whereas the safe-haven gold commerce profited handsomely in 2025 as tariff wars and different wars fed investor fears of financial turmoil, the macro outlook for 2026 could counsel a shift from safe-haven property in the direction of commodities that can help synthetic intelligence (AI) infrastructure builds, and improve international power safety.

After taking earnings on gold shares, which commodity shares might one put money into subsequent for 2026? Among the many high contenders are copper, the brand new gold for AI datacentres, uranium, a clear power supporting electrification, and lithium as a turnaround play.

Let’s take a more in-depth look.

Copper: A significant provide deficit could carry Canadian copper shares

A significant copper provide deficit might be brewing in 2026. Copper is in excessive demand as a key “wiring” materials for sprouting AI datacentres. Knowledge centres and modernized grids are copper-intensive, and copper demand is rising quickly, with AI hyperscalers rising their funding budgets for 2026.

Copper worth efficiency to this point in 2025.

To seize the copper upside, Canadian traders could purchase copper mining shares like Teck Assets (TSX:TECK.B) inventory.

Teck Assets might generate extra income, earnings and money circulate from its copper property because it ramps up the huge Quebrada Blanca mine, which can hit peak manufacturing by 2027. The spin-off of coal property made Teck Assets a close to pure-play copper development inventory that’s even engaging to international mining big Anglo American, which seeks a merger with Teck in a deal due for a shareholder vote this week. The merger could create a world “High 5” copper producer.

Teck Assets generated about 60% of its income from copper through the first 9 months of 2025. The rest was zinc gross sales as complete income grew 22.6% 12 months over 12 months.

Uranium: Cameco inventory could shine in 2026

World uranium provide capability will take time to develop as a result of a decade of underinvestment, whereas numerous new reactor builds and modular tasks are arising as politicians heat as much as nuclear-powered electrical energy technology as a dependable base load provide as economies demand extra power to energy a rising fleet of recent AI supercomputers.

Cameco (TSX:CCO) is without doubt one of the most established uranium miners. It’s a nuclear gas enrichment contractor and a key nuclear power design accomplice (by way of its 49% stake in Westinghouse). The uranium inventory might print excellent news in 2026 because it rises in keeping with uranium costs, which have remained agency since 2024, whereas long-term contract costs lately soared to file highs heading into 2026.

Uranium contract costs crept to a file excessive of US$86 per pound in November, a worth final seen in Might 2008. Utilities might be coming again to the contracting desk in 2026.

Cameco has important capability to contract for extra uranium provides for 2027-2030 because it ramps up manufacturing from beforehand mothballed mining property.

Purchase dividend-growth power shares in 2026

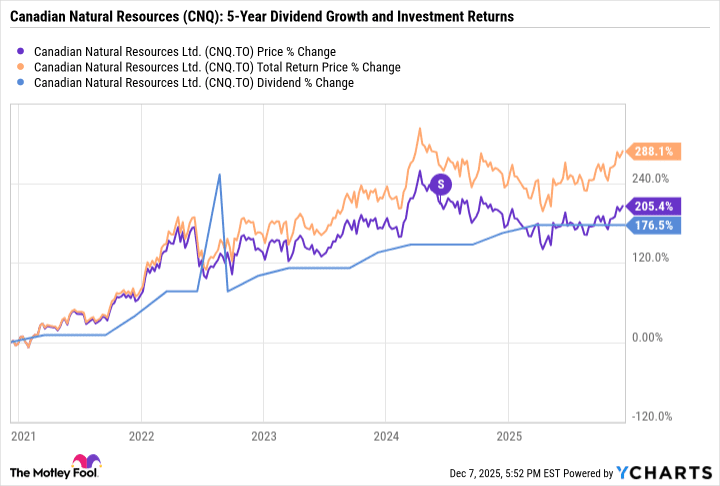

Oil costs will stay unstable, as common. Nevertheless, given the weak point skilled in 2025, with oil costs dropping 16% 12 months thus far, a rebound in 2026 might flood choose low-cost oil miners like Canadian Pure Assets (TSX:CNQ) inventory with more money sources to spoil their shareholders with dividend hikes and share repurchases.

Canadian Pure Assets is dedicated to returning free money circulate (after dividends) to shareholders. The $99.9 billion TSX power inventory has raised dividends by 176.5% over the previous 5 years, and will maintain the shareholder-friendly coverage as oil costs rebound. CNQ’s present, well-covered dividend yields 4.9% yearly.

World oil demand is rill rising, and CNQ is rising its manufacturing charges each organically and thru acquisitions, rising the enterprise.

The place to take a position subsequent?

If you happen to’re rotating earnings on gold shares in 2026, take into account splitting your allocations (say about 60%) into copper and uranium shares, which proceed to align with secular development tendencies of AI and power safety, and investing the rest into dividend payers like CNQ inventory to boost your portfolio’s income-generating energy to safe your retirement wants.