By Sayon Deb, Director of Insights, UL Requirements & Engagement

In simply 5 years, lithium-ion battery fires linked to e-mobility units have developed from a fringe danger right into a mainstream security and legal responsibility disaster – notably in dense city areas, like New York Metropolis, the place adoption of those units has outpaced regulatory safeguards.

Along with the apparent public security risk, e-mobility battery associated fires characterize a major and increasing legal responsibility publicity for insurers, property managers, and metropolis businesses. Our newest report – developed in collaboration with Oxford Economics – units out to reply a extra basic query: What is that this disaster actually costing town?

The reply, conservatively estimated, is as much as $519 million in mixed human and financial loss between 2019 and 2023. This determine consists of fatalities, accidents, and structural property injury

Why Now? Why New York?

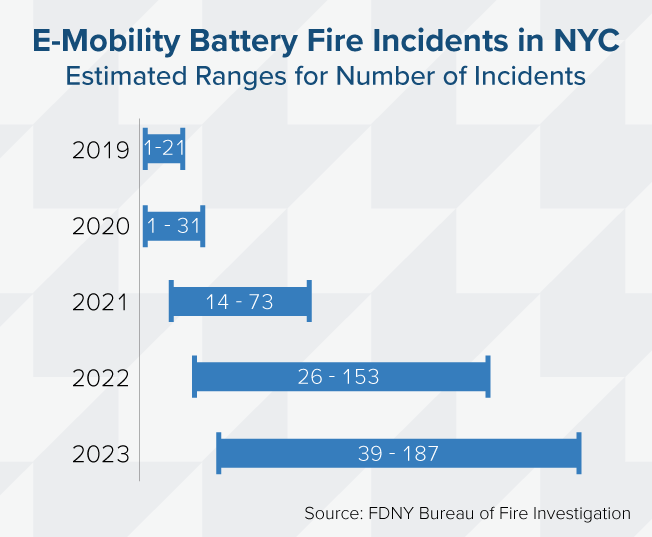

The dramatic rise in fireplace incidents – an estimated eightfold improve from 21 in 2019 to as many as 187 incidents in 2023 – correlates strongly with the inflow of low-cost, uncertified e-bikes and scooters. New York Metropolis’s distinctive mixture of visitors congestion, delivery-based gig work, and dense multi-family housing has made it a case research in how rapidly innovation can outstrip danger administration.

Knowledge from the Hearth Division of New York, the Shopper Product Security Fee, and UL Options’ Lithium-Ion Battery Hearth Incident Database shaped the muse of our modeling. This helped us generate incident estimates of fatalities, accidents, and structural properties damages.

Oxford Economics translated these incident reviews into price estimates utilizing a rigorous, conservative methodology by making use of federal valuation metrics for lack of life and harm. Fatality prices had been calculated utilizing the U.S. Division of Transportation’s Worth of a Statistical Life, set at $13.2 million per life as of 2023. Non-fatal harm prices had been derived as severity-weighted fractions of that worth, starting from minor harm to crucial harm, in accordance with DOT and Workplace of Administration and Price range financial steering.

Our evaluation then built-in structural fireplace price benchmarks from each Triple-I and the Nationwide Hearth Safety Affiliation. Triple-I’s knowledge was notably essential in defining the upper-bound estimates for property loss. Claims knowledge on the common insurance coverage payout for residential fireplace injury supplied a grounded, actuarial counterweight to NFPA’s generalized nationwide averages.

This dual-source method allowed us to seize a extra practical vary of probably losses throughout completely different housing sorts, from NYCHA public models to personal houses.

A rising blind spot for insurers

From a risk-modeling standpoint, e-mobility fireplace incidents don’t map simply to traditional insurance coverage classes. Many e-mobility customers, notably gig financial system employees, depend on leased, used, or modified e-bikes and e-scooters to satisfy supply calls for. A few of these units are powered by third-party or uncertified batteries or, in some cases, include second-hand parts. This creates a messy danger surroundings by which it’s laborious to know who owns what, the way it has been maintained, or the way it’s getting used. Furthermore, fires ensuing from these units typically fall exterior the scope of ordinary product warranties or producer duty. This makes it tough to find out who’s accountable when one thing goes improper.

For insurers, this presents a rising blind spot. Conventional assumptions round property and contents protection didn’t embody high-risk units charged in hallways or shared dwelling areas or for ignition sources that aren’t a part of standard product recall channels.

A $300 imported battery with no certification can set off a six-figure declare, and people dangers have gotten extra frequent.

The Path Ahead

Regulatory momentum is enhancing. New York Metropolis’s Native Regulation 39, signed in 2023, bans the sale and lease of uncertified e-mobility units. In July 2024, New York Governor Hochul enacted extra statewide measures to assist battery security and consumer training. Federal laws geared toward establishing nationwide security necessities for lithium-ion batteries utilized in e-bikes and e-scooters is making its manner via Congress. Whereas these are optimistic steps, enforcement and consciousness stay uneven, leaving important gaps in shopper safety and danger mitigation.

From our perspective at ULSE, a multi-pronged technique is crucial:

- Higher enforcement of security requirements for batteries and chargers.

- Extra sturdy public training on protected charging practices.

- Commerce-in and swap applications that encourage supply employees to discard unsafe batteries.

- Underwriting fashions that contemplate machine certification, shopper conduct, and constructing sort.

- Improved incident reporting frameworks that allow cities and insurers to gather higher knowledge and subsequently higher observe danger publicity.

With higher knowledge, smarter requirements, and extra coordinated public-private motion, the way forward for e-mobility will thrive with security at its heart.

Mr. Deb will likely be among the many danger and insurance coverage trade thought leaders talking at Triple-I’s Joint Business Discussion board (JIF) in Chicago on June 18, 2025. It’s not too late to register to attend this insight-driven occasion.