All through historical past, insurers have been pivotal in driving social change, enabling human progress, innovation, and prosperity. From seatbelts to vaccines and fire-retardant supplies, insurers have fostered quite a few improvements. These days, they face a brand new monumental problem: local weather change. 2024 has been one other report loss yr for insurers pushed by pure catastrophes linked to local weather change. Insurers are therefore in search of greener pastures. If completed proper, aiding companies of their transformation to scale back greenhouse fuel emissions turns into a constructive for insurers. They are often facilitators of the transition to a carbon-neutral future by exerting affect throughout the wide range of industries they finance.

There is a chance for insurers to safeguard their top-line and bottom-line whereas supporting prospects on their web zero journeys. In Underwriting, that minimizes threat publicity and scope for regulatory fines by proactively responding to adjustments, and purchasers who successfully embark on the inexperienced transition are anticipated to carry increased gross sales within the mid to long run. In Investments, the case is even higher understood: 93% of traders say that local weather points are almost certainly to have an effect on the efficiency of investments over the subsequent two to 5 years. Non-transitioning corporations or those that begin transitioning too late are at risk of shedding an funding grade credit standing, whereas the outperformers – what we name ‘inexperienced stars’ are anticipated to learn from inexperienced applied sciences shift in a Paris-agreement-aligned world situation.

A brand new software for worthwhile portfolio decarbonization

Insurers want to have the ability to translate their investee and purchasers’ emission discount measures into monetary implications for applicable threat calculations, to decarbonize profitably on their very own finish.

As we at Accenture are dedicated to fostering web zero enterprise practices we’ve launched the GreenFInT (Inexperienced Monetary Establishment Device ), also called the Worthwhile Portfolio Decarbonization Device. Evaluating pattern consumer portfolio dynamics up till 2050 for top carbon intensive sectors, it exhibits ‘inexperienced stars’ would possibly outperform ‘local weather laggards’ by 30-40 proportion factors. The true worth of the software lies in familiarizing insurance coverage managers throughout funding, threat and pricing with setting assumptions for various world views, from a ‘sizzling world’ situation to reaching the Paris alignment.

Permit me to delve into the software in larger element. The GreenFInT software caters to each the emissions measurement and reporting use instances (e.g., ESRS E1 quantitative KPIs for CSRD) in addition to to enterprise worth instances with reference to decarbonization. The software applies local weather situations (e.g., 1.5°C, 2.4°C) to portfolio corporations’ expertise combine, relying on their Internet Zero pledges and transition plans. Variations in expertise combine, pledges, and plans translate into divergent profitability curves through required capital investments and variations in operational prices.

‘Inexperienced stars’ win out in the long run

For illustration, an insurer’s ‘inexperienced star’ consumer from the facility era sector with a SBTi verified Internet Zero goal by 2040 has and could have a bigger share in renewables than a consumer categorised as ‘laggard’. With its proactive transition in the direction of web zero, the ‘inexperienced star’ consumer has preliminary excessive capital prices to finance the construct out of put in capacities from renewable vitality sources to fulfill its milestones whereas electrical energy costs are comparatively excessive – outlining a enterprise alternative for insurers because the consumer is in want of financing and insuring of the renewables constructed out. As compared, a ‘laggard’ firm had no and won’t have capital investments past typical substitute and upkeep prices of its energy vegetation. Alternatively, renewables have a lot decrease operational value in comparison with energy generated from nuclear vitality and pure fuel. Thus, the ‘inexperienced star’ that has invested in renewables in a well timed trend will profit from decrease operational prices whereas the ‘laggard’ could have increased operational prices from conventional vitality sources.

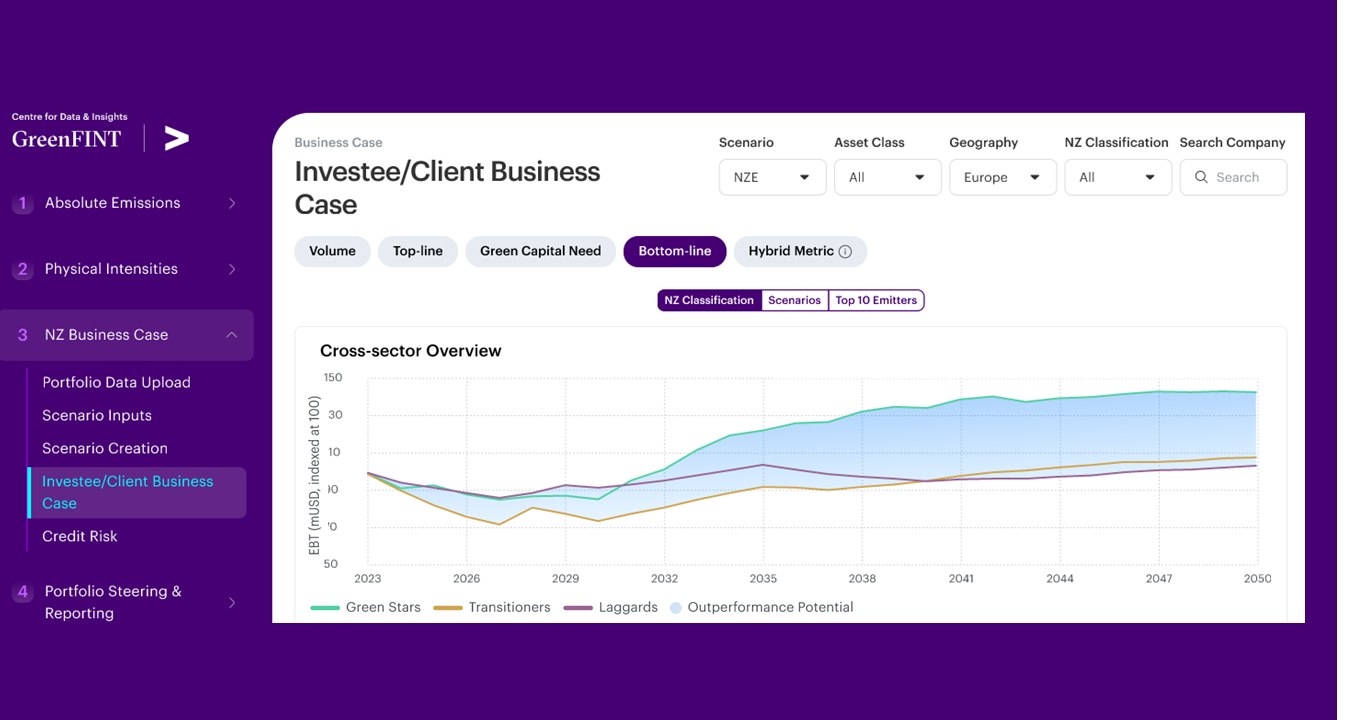

Let’s take an exemplary insurance coverage portfolio with 40 massive firm purchasers from 4 high-intensity sectors, specifically energy era, metal, actual property, and automotive, centered inside Europe. In a 1.5°C situation, the capital want for the web zero transition of those corporations quantities to roughly 650bn USD 2023-2050 – in response to the GreenFInT modelling. Whereas within the mid-term up till 2030, the EBT margin of ‘laggards’ outperform ‘inexperienced stars’ by roughly 6 proportion factors, within the long-term, 2023-2050, ‘inexperienced stars’ outperform ‘laggards’ by 30-40 proportion factors (see graph under).

This forward-looking method – leveraging scientific sector carbon budgets vs. conventional forecasts based mostly on historic values – permits insurers to combine long-term situations (as much as 2050) into their present concerns. This can be a most vital step in the direction of breaking the ‘tragedy of the horizon’. GreenFInT makes it attainable to establish insurers’ investees and purchasers with reliable web zero commitments because the enterprise case evaluation can reveal who could not be capable of afford their web zero commitments. Constructing a trusted relationship with these corporations as insurer or investor immediately, is vital for a worthwhile decarbonization. Insights gained by GreenFInT may be useful to prioritize purchasers to interact with and a grounded dialog opener to raised perceive the purchasers’ transition plans.

Past a web zero enterprise case evaluation, GreenFInT additionally covers the accounting of Scope 3 Class 15 emissions in absolute phrases and bodily intensities in addition to goal setting and a ‘What-If’ functionality, enabling insurers to simulate results on their carbon footprint with changes to their portfolio.

The time to behave is now

Insurance coverage has persistently demonstrated resilience within the face of quite a few challenges, and the present push in the direction of decarbonization isn’t any totally different. By embracing the transition to web zero, insurers can’t solely safeguard their profitability but in addition play a pivotal position in fostering a sustainable future. The combination of science-based sustainability targets into underwriting and funding practices will allow insurers to drive vital change throughout varied industries. As regulatory pressures and public expectations proceed to rise, insurers should act decisively to keep away from the dangers of inaction and greenwashing. The instruments and methods outlined present a transparent pathway for insurers to attain worthwhile portfolio decarbonization, making certain long-term progress and belief in a quickly evolving panorama. The time to behave is now, and the alternatives for individuals who lead the cost are immense. For additional dialogue on learn how to implement these methods in your enterprise, please get in contact.