How Agentic AI Will Improve Customer Engagement in Insurance

Insurance · July 1, 2026

There is a hidden disease that is killing insurers — the disease of legacy technology. The problem is a matter of strategic priority, investment and focus. Insurers are still pouring funds down obsolete tech tunnels through amortization, ongoing maintenance, and payoffs — and they are doing it only to maintain the way they have done business in the past. It does nothing to support doing business for the future, including bringing new products to market. Business transformation in insurance must include the move to an AI-enabled core to create the business operating model needed for the future.

With a shift to cloud and AI-native core systems, insurers can establish an evergreen business foundation that can adapt quickly to technology and market changes, without another complete transformation. In Majesco’s Strategic Priorities 2026 Report, we break down the broad issue of legacy into insurance functions and opportunities.

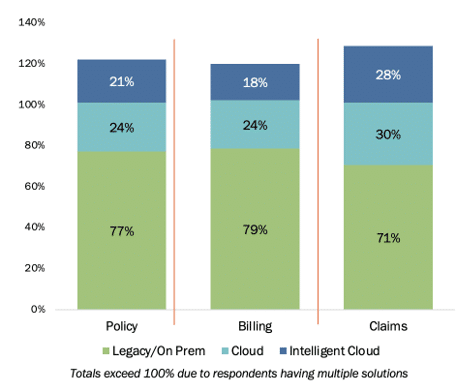

Majesco found that legacy, on-premise solutions are still the predominant core option for insurers, with 71–79% still using them. Only 24–30% are using core cloud solutions. Surprisingly, only 18-28% of insurers have adopted intelligent core cloud solutions. Despite the last twenty years of core modernization, the rapid technology shift—from modern modular core to cloud and now intelligent core—has challenged insurers to keep up with the shifts.

The reasons legacy systems still dominate are varied and complex, but a few key universals seem to predominate.

Figure 1: Status of core systems implementations

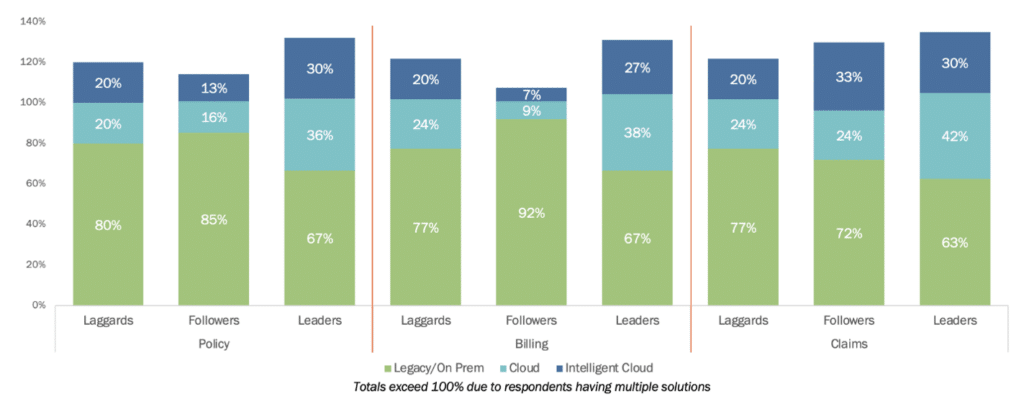

A deeper dive comparing Leaders, Followers, and Laggards in Figure 2 unveils fundamentally different architectural realities that position them in a new intelligent era of insurance. Across policy, billing, and claims systems, Leaders demonstrate lower dependence on legacy/on-prem environments and meaningfully higher adoption of both cloud and intelligent cloud platforms.

For policy administration, only 67% of Leaders remain on legacy systems as compared to 80% of Laggards and 85% of Followers. Billing systems amplify this divide. While 92% of Followers and 77% of Laggards remain anchored in legacy, only 67% of Leaders do and show the strongest cloud adoption (38%) and materially higher penetration of intelligent cloud billing (27%). Claims systems follow a similar pattern, but with one notable exception: Followers outperform Laggards in intelligent cloud claims adoption (33% vs. 20%).

Collectively, these patterns illustrate a widening technology foundation gap that will shape industry growth and competitiveness in the Intelligence Era.

Leaders are clearly focused on an intelligent cloud foundation that enables intelligent automation, embedded AI, faster cycle times, and seamless data flows. This is in contrast to Laggards and Followers who are entrenched in legacy environments that limit their operational ability.

Figure 2: Status of core systems implementations by Leaders, Followers, and Laggards

While Leaders clearly stand out in the move to cloud and intelligent cloud solutions, overall, the industry is significantly at risk with the extent of legacy still used within insurers.

Many did not make the move to native cloud soon enough and fell behind, becoming legacy. Today, many are already falling behind with the move to an AI-native foundation and are operating with systems that are quickly becoming the new legacy.

Replacing outdated core technology with next-gen intelligent core has never been more important. It removes the disease of legacy and grows a healthy business.

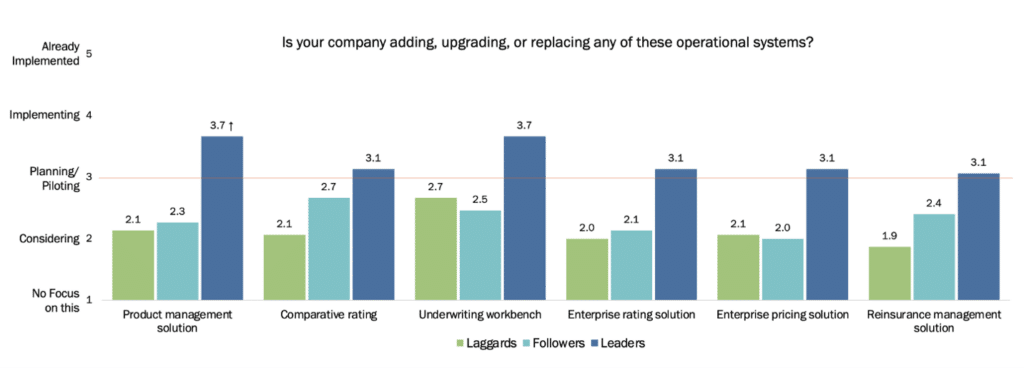

Year-over-year changes, segmenting results by Leaders, Followers, and Laggards reveal dramatic discrepancies in modernization maturity, as seen in Figure 3. Leaders score significantly higher across all operational systems, with ratings in the Planning/Piloting and Implementing phases, indicating active focus and investment to enhance overall operational agility. Outside of the underwriting workbench, Laggards are consistently only at the Considering phase, demonstrating little to no modernization activity across critical platforms. Followers are equally behind in enterprise rating and enterprise pricing.

Figure 3: Adding, upgrading, or replacing operational systems by Leaders, Followers, and Laggards

Distribution management solutions that provide onboarding, licensing and compensation management are essential in managing distribution channel relationships. Investments in digitization have two potential sources of return for insurers. Reduction in costs due to the ability to automate processes is a significant potential source of value—but only if it improves the agent’s ability. The second is ease of doing business. Together they help both insurers and agents drive growth.

With continued consolidation of the agent and broker channels, the importance of these solutions and the influence they have on distribution partners’ view on whether the insurer is easy to do business with cannot be understated. The Majesco-commissioned Celent research report, Reshaping the Distributor Insurer Relationship, found that to become the agent’s preferred insurer, carriers must have great services, good pricing, and differentiated products, as well as policies, procedures, and technology that make it easy to do business.[i]

These systems influence agent satisfaction, speed to appoint, compensation accuracy, commission agility, and overall ease of doing business—all critical to distribution performance in an increasingly competitive landscape.

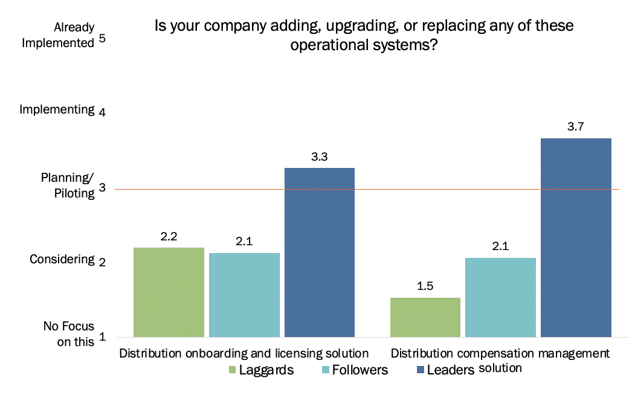

In Figure 4, Leaders report high activity in distribution compensation modernization (3.7) as compared to Followers and Laggards, plus meaningful activity in onboarding and licensing systems (3.3). Followers and Laggards fall sharply behind — particularly in compensation systems, where scores drop as low as 1.5, a 139% gap to Leaders.

Once again, this growth lever is maximized by Leaders and reflects their commitment to improving the agent and broker experience as well as supporting multi-channel expansion.

Figure 4: Adding, upgrading, or replacing distribution management solutions by Leaders, Followers, and Laggards

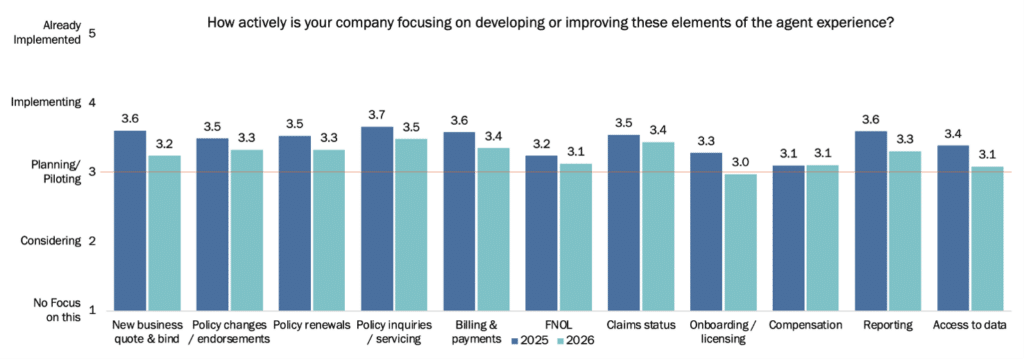

The year-over-year changes across agent-experience capabilities in Figure 5 show a clear and consistent pattern of flat or declining activity levels across nearly every category. While this suggests the business-as-usual mindset theme, it is likely to be representative of the fact that during the digital era, many insurers modernized their digital portals to elevate the experience.

Figure 5: Year-over-year changes in developing or improving elements of the agent experience

However, as these companies move to cloud and AI-native core solutions, a revamp of their digital portals will likely be needed to take advantage of the extensive automation and embedded analytics that can further enhance the agent experience.

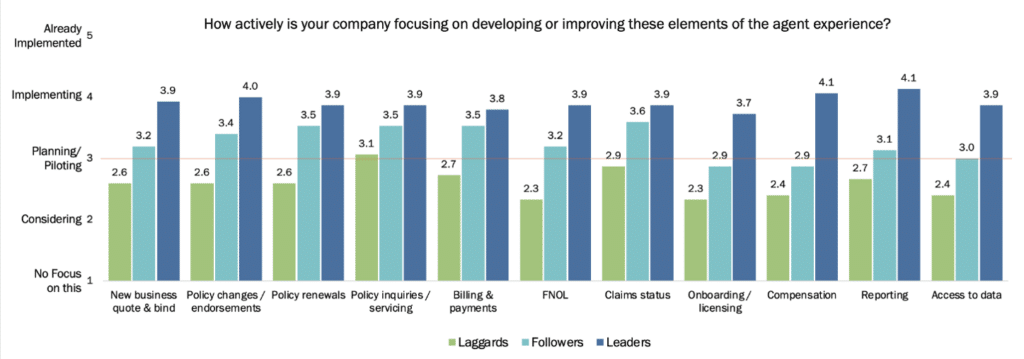

When we look at Leaders, Followers and Laggards, however, Leaders report the highest activity levels across all categories, as seen in Figure 6, anchored in the Implementing phase, which aligns with them implementing cloud and AI-native core solutions and wanting to take advantage of them in the portals.

Followers sit in the range between Planning/Piloting and Implementing—active but not transformative. Laggards, however, consistently score between Considering and Planning/Piloting, indicating minimal effort in modernizing agent tools and workflows, which is also seen in modernizing their core.

Figure 6: Developing or improving elements of the agent experience, by Leaders, Followers, and Laggards

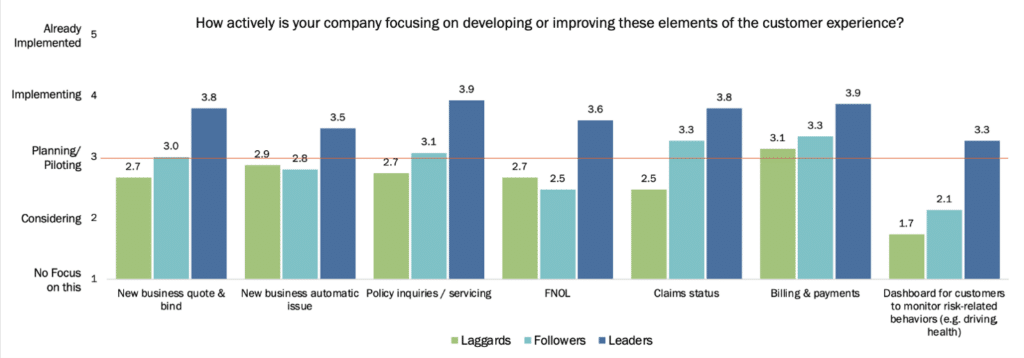

Once again, Leaders consistently score the highest across all customer experience categories, as seen in Figure 7, with all areas at or just below the Implementing phase. In contrast to the Agent Experience, Followers and Laggards maintain moderate activity near the Planning/Piloting phase on four areas, with Followers outpacing Laggards in claims status.

Given the strong focus on cloud- and AI-native core systems by Leaders, this view aligns with their wanting to take advantage of them in the portals.

This underscores a widening divide, where Leaders are implementing intelligent core solutions that can redefine customer experiences that incorporate automation, intuitive self-service, proactive communication, AI, and data-driven personalization.

Figure 7: Developing or improving elements of the customer experience, by Leaders, Followers, and Laggards

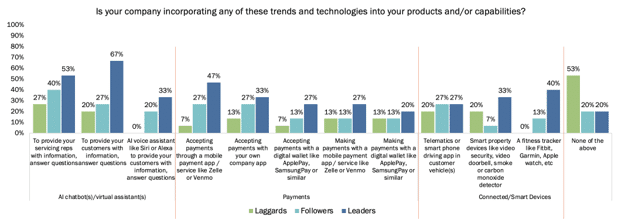

Leaders once again continue to exhibit significantly higher adoption, as seen in Figure 8. AI-enabled service tools, including chatbot-based support for both customers and employees, range from 33–67% penetration.

In contrast, Laggards demonstrate extremely low penetration across nearly all digital and AI-driven technologies, with categories ranging from 0–27%, reflecting the limitations of their legacy systems. Followers fall in the middle but closer to Laggards in many areas.

The “none of the above” response category is especially telling, where Laggards display the highest share of non-adoption—a clear sign of lack of innovation maturity and cultural embrace of digital experimentation.

Figure 8: Incorporation of trends and technologies into products and/or capabilities by Leaders, Followers, and Laggards

If insurance legacy systems are a hidden disease, Cloud and AI-native core solutions are an antidote. Legacy platforms are keeping insurers from the meaningful strides they can make to command better market positioning, greater brand prestige, lower cost ratios, drive growth, and greater profits. In real-world situations, Leaders are conquering insurance business issues with technologies that open them up to an entirely new world of business possibilities and prepare them to meet modern risk issues and the modern customer with relevant insurance answers.

Are you ready to lead?

Majesco invests in the insurer experience, helping your organization to gain control of your future and innovate with confidence. Learn more about how today’s industry trends point clearly toward a path away from legacy and toward cloud and AI-native solutions. For more insurance digital transformation trends, be sure to read Majesco’s recent Thought Leadership report, Strategic Priorities 2026: The Frontier Insurer in the Intelligent Era of Insurance, and sign up for our upcoming webinar, From Intelligence to Action: How GenAI and Agentic AI are Reinventing Insurance as a Frontier Insurer.

[i] Carnahan, Karlyn, “Reshaping the Distributor Insurer Relationship: A Survey of Independent Insurance Agents,” September 20, 2021, https://www.majesco.com/white-papers/reshaping-the-distributor-insurer-relationship/

The post The Hidden Cost of Standing Still:Legacy Platforms Slow Growth and Halt the Shift to AI-Enabled Insurance Business appeared first on Majesco.