Between the Nifty 50 Vs Nifty 500 Index Fund, which one do you must select? Allow us to discover the reply based mostly on the final 21 years of information.

Each index fund investor ultimately faces the identical query: “Which broad-market index ought to be my core holding?” The same old suspects are the Nifty 50 TRI, the Nifty LargeMidcap 250 TRI (NLM 250), and the Nifty 500 TRI. Every has a definite pitch — Nifty 50 for simplicity, NLM 250 for greater returns, and Nifty 500 for true market breadth.

This text makes use of precise NSE India TRI information spanning April 1, 2005 to March 2026 — 21 years, 253 month-to-month observations — to reply the query correctly. We study lump sum progress, drawdown profiles, rolling returns throughout 1, 3, 5 and 10-year home windows, and rolling customary deviation. After going by way of all the information, we arrive at a transparent view on which index makes probably the most sense for many long-term traders, and why Nifty 500 emerges as probably the most sensible selection.

Nifty 50 vs Nifty 500 Index Fund: Which One Ought to You Choose?

Allow us to first perceive what are these Indices are all about. Right here, for the comparability, I’ve taken the Nifty 50, Nifty Massive Midcap 250 Index and the Nifty 500 Index.

Nifty 50 –

The Nifty 50 covers 50 large-cap shares and represents roughly 55.5% of NSE’s complete free-float market capitalisation. It’s dominated by Monetary Providers, IT, Oil & Fuel, and FMCG. The index covers solely 14 out of 21 sectors at NSE. It’s the most liquid, most researched, and most tightly tracked Indian index — passive funds monitoring it have the bottom monitoring error and impression prices available in the market. Consider it as a portfolio of India’s 50 most dominant companies, market-cap weighted.

Nifty Massive Midcap 250 Index –

The NLM 250 is a 50-50 mix — it mandatorily allocates 50% weight to the Nifty 100 (giant caps) and 50% to the Nifty Midcap 150. This equal-part building isn’t market-cap weighted on the section stage — it’s a rule-based equal allocation between giant and mid caps, reset quarterly. That is the crucial distinction: NLM 250’s midcap publicity is structurally pressured to be 50%, no matter the place market capitalisation really sits. Consequently, mid caps get a far greater weight in NLM 250 than their precise market-cap share warrants. That is precisely what drives each its greater returns and its greater danger.

Nifty 500 Index –

The Nifty 500 is the broadest benchmark on this comparability. It covers 500 corporations and represents roughly 92.3% of NSE’s complete free-float market capitalisation — by far the widest protection. Critically, it’s absolutely market-cap weighted — which means every inventory will get a weight proportional to its precise dimension available in the market. The approximate present composition is:

• Nifty 50 (prime 50 giant caps): ~58.6% weight

• Nifty Subsequent 50: ~12.2% weight

• Nifty Midcap 150: ~18.5% weight

• Nifty SmallCap 250: ~10.7% weight

This implies Nifty 500 provides you real publicity to India’s whole listed fairness universe — however in proportion to financial weight, not arbitrary equal-allocation. The mid and small-cap publicity is actual however proportional and naturally managed, not like NLM 250’s hard-coded 50% midcap mandate.

Lump Sum Invested –

Allow us to now perceive what if somebody invested Rs.1 lakh in these three Indices, then what will be the present worth. I’ve thought-about the bottom date as 1st April 2005 primarily as a result of the Nifty Massive Midcap 250 Index base begins from 1st April 2005.

What did Rs.1 lakh invested on April 1, 2005 really grow to be after 21 years of staying absolutely invested by way of each disaster and restoration?

| Index | CAGR p.a. | Rs.1L ? (21Y) | Max Drawdown | Market Cowl |

| Nifty 50 TRI | 13.50% | Rs.14.29 L | -59.5% | ~55.5% of NSE |

| Nifty 500 TRI | 13.74% | Rs.14.93 L | -63.7% | ~92.3% of NSE |

| NLM 250 TRI | 15.17% | Rs.19.41 L | -67.6% | ~87.0% of NSE |

The chart tells a transparent story. All three indices delivered substantial wealth creation — turning Rs.1 lakh into Rs.14–19 lakhs. However the hole between NLM 250 and the opposite two is important: Rs.5.12 lakhs further per lakh invested versus Nifty 50, and Rs.4.48 lakhs further versus Nifty 500. That is the facility of a 1.67% annual CAGR benefit over 21 years.

Nevertheless, Rs.14.93 lakhs for Nifty 500 versus Rs.14.29 lakhs for Nifty 50 can also be value noting. Nifty 500’s benefit over Nifty 50 is Rs.64,000 per lakh invested — modest in rupee phrases, however achievable with meaningfully decrease structural complexity and a extra diversified portfolio.

NLM 250 wins on absolute return — however Rs.5.12L further got here at the price of 8.1% deeper crashes and much more risky holding expertise.

Nifty 500 beats Nifty 50 by Rs.64,000 per lakh — modest premium, however covers 500 vs 50 corporations and 92% vs 55% of the market.

The return hole between Nifty 500 and Nifty 50 is sufficiently small that almost all traders wouldn’t discover — however the diversification profit is actual and structural.

Drawdown –

Now allow us to perceive the drawdown of all these indices.

That is the chart that separates traders from merchants. Drawdown measures how far beneath its personal all-time excessive every index was at any level — computed from every day information, displayed month-to-month. That is the ache you’ll have really lived by way of as an investor. It isn’t a statistic on paper; it’s the quantity you stare at in your portfolio app throughout a market crash.

The 2008 Market Crash

All three indices crashed severely, however not equally:

• Nifty 50: ?59.5% from peak, trough October 27, 2008

• Nifty 500: ?63.7% from peak, trough October 27, 2008

• NLM 250: ?67.6% from peak, trough March 9, 2009 — 4.5 months LATER than Nifty 50

Two issues matter right here. First, Nifty 50 bottomed 4.5 months earlier than NLM 250 — giant caps entice institutional shopping for first throughout crises. NLM 250’s pressured 50% midcap publicity meant it saved falling whereas Nifty 50 was already recovering. Second, the distinction between ?59.5% and ?67.6% is psychologically monumental. An investor watching their portfolio halve is in ache. An investor watching it fall by two-thirds is usually in panic-selling territory — which is exactly once they completely destroy their returns.

Nifty 500 at ?63.7% sits between the 2, and its trough aligned with Nifty 50’s (October 2008), not with NLM 250’s later backside. The market-cap weighting of Nifty 500 — with ~58.6% in giant caps — gives a pure stabiliser throughout market stress that NLM 250’s hard-coded 50% midcap allocation can not.

Covid Crash

All three fell roughly 30–31% within the March 2020 crash. The ordering was maintained: NLM 250 ?31.2%, Nifty 500 ?30.6%, Nifty 50 ?30.2%. Restoration was swift for all — inside 8 months. The COVID crash, not like 2008, was V-shaped and policy-driven, and didn’t considerably differentiate the three indices by way of investor expertise.

In each vital market crash, the rating is constant: NLM 250 falls deepest, Nifty 500 falls reasonably greater than Nifty 50, and Nifty 50 recovers quickest.

The 8.1% further drawdown of NLM 250 versus Nifty 50 is not only a quantity — it represents actual investor ache and actual danger of panic-selling on the backside.

Nifty 500’s drawdown (?63.7%) is deeper than Nifty 50 (?59.5%) however considerably shallower than NLM 250 (?67.6%). An inexpensive center floor.

An investor who bought on the 2008 backside would have turned a paper loss right into a everlasting one. The deepest-falling index carries the very best danger of this behavioural failure.

Rolling CAGR Returns Throughout 4 Time Horizons

A single point-to-point return is nearly meaningless for evaluating an index — it relies upon completely on whenever you began. Rolling return evaluation solves this by computing the return for each attainable begin date within the dataset, exhibiting you the complete distribution of investor outcomes throughout completely different market entry factors.

Every level on the rolling return chart solutions: “If I had invested precisely N years earlier than immediately and held patiently, what would my CAGR have been?” A worth beneath zero means you misplaced cash in actual phrases.

1 12 months Rolling Returns –

The 1-year chart is excessive volatility on show. All three indices swing from roughly +90–115% to ?52–60%. The return unfold (greatest minus worst) is 142 proportion factors for Nifty 50, 157 proportion factors for Nifty 500, and 175 proportion factors for NLM 250 — the widest dispersion of any index at any window. That is the price of NLM 250’s mid-cap aggression at quick holding durations.

Nifty 500 produced unfavorable 1-year returns in 20.7% of all durations — barely extra regularly than each Nifty 50 (18.3%) and NLM 250 (18.3%). It is because Nifty 500’s broader market publicity (together with small caps) amplifies draw back in a manner that pure large-cap focus (Nifty 50) avoids.

At 1-year, fairness investing is almost hypothesis. Entry level determines nearly all the things.

All three indices had unfavorable returns in ~18–21% of rolling 1-year durations. No index is “protected” at this horizon.

NLM 250 has the widest return unfold (175pp) — greatest wins AND greatest losses at 1 12 months.

In case your horizon is 1 12 months, fairness is the unsuitable asset class. Full cease.

3 Years Rolling Returns –

At 3 years, the image improves considerably. Unfavourable CAGR durations grow to be a lot rarer — however they haven’t disappeared. A crucial discovering: Nifty 500 produced unfavorable 3-year CAGRs in 5.1% of all durations — twice as regularly as Nifty 50 (2.3%) and fewer regularly than NLM 250 (6.9%). The Nifty 50’s focus in steady giant caps provides it the bottom likelihood of a 3-year loss.

On the similar time, NLM 250 begins to point out its return benefit — averaging 14.5% 3-year CAGR versus Nifty 500’s 13.0% and Nifty 50’s 12.5%. However with a better frequency of unfavorable durations and a worse minimal (?9.4% vs ?2.6%), the danger isn’t absolutely compensated at this window.

Nifty 500 beats Nifty 50 in 58% of all rolling 3-year durations — a modest however constant edge.

Nifty 50 had the fewest unfavorable 3-year durations (2.3%) — its large-cap stability reveals up right here.

NLM 250’s greater common CAGR (+14.5%) is interesting, however unfavorable durations (6.9%) are practically 3x Nifty 50.

Nifty 500 beats Nifty 50 in 58% of 3-year durations — a constant however slim outperformance.

A 3-year horizon continues to be too quick for aggressive mid-cap publicity. Nifty 500 or Nifty 50 is extra acceptable right here.

5 Years Rolling Returns –

The 5-year chart is the place fairness investing begins to really reward endurance. Probably the most putting discovering: Nifty 50 had zero unfavorable rolling 5-year durations in the whole 21-year dataset. Each single 5-year rolling CAGR was optimistic for Nifty 50. Nifty 500 had simply 1.0% of durations with a unfavorable CAGR — basically remoted to the worst 2007–2008 entry cohort. NLM 250 was 0.5%.

At 5 years, Nifty 500 beats Nifty 50 in 52% of all durations — roughly a coin flip. NLM 250, then again, beats Nifty 500 in a outstanding 97% of all rolling 5-year durations. That is the place NLM 250’s structural mid-cap bias begins paying off constantly. Nevertheless, it comes with a better common customary deviation (~21.9% vs ~20.6% for Nifty 500 vs ~19.7% for Nifty 50).

At 5 years, Nifty 50 had ZERO unfavorable rolling durations. Fairness danger largely disappears at this horizon.

NLM 250 beats Nifty 500 in 97% of 5-year durations — a unprecedented discovering that helps mid-cap allocation for long-term traders.

Nifty 500 and Nifty 50 are basically tied at 5 years (52% win fee for Nifty 500). The additional 0.5% CAGR from Nifty 500 is actual however slim.

In case your horizon is 5+ years and you may deal with average drawdowns, Nifty 500 is the rational selection over Nifty 50. For optimum returns, NLM 250 dominates — however at greater skilled volatility.

10 Years Rolling Returns –

The ten-year rolling chart delivers the clearest discovering of this complete evaluation: each single rolling 10-year interval — for all three indices — was optimistic with out exception. Zero losses throughout 21 years of information and a whole bunch of rolling 10-year durations. That is the final word argument for long-term fairness holding: affected person traders all the time received, no matter which of those three indices they selected.

On the 10-year window, Nifty 500 beats Nifty 50 in 77% of all durations — considerably extra constant than at shorter horizons. And NLM 250 beats Nifty 500 in 100% of rolling 10-year durations — with out exception. These are highly effective information factors. The query is whether or not the additional CAGR from NLM 250 (+1.8% over Nifty 500) is well worth the further volatility and deeper drawdowns over that decade.

All three indices: zero unfavorable 10-year durations. Fairness over 10 years has by no means misplaced on this dataset.

NLM 250 beats Nifty 500 in 100% of rolling 10-year durations — +1.8% avg CAGR benefit.

Nifty 500 beats Nifty 50 in 77% of 10-year durations — a dependable and constant edge.

The longer the horizon, the extra Nifty 500’s breadth and NLM 250’s mid-cap publicity repay.

For a 10-year investor selecting between Nifty 50 and Nifty 500, the information is evident: Nifty 500 wins extra typically.

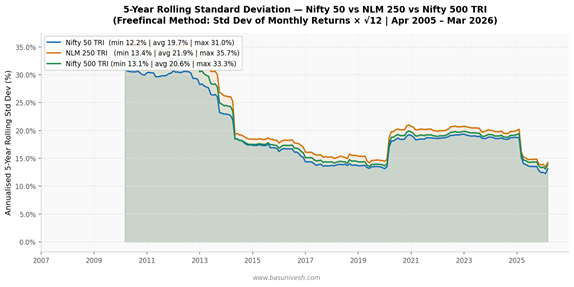

Rolling Commonplace Deviation –

Commonplace deviation of month-to-month returns, annualised by multiplying by ?12, is probably the most strong measure of skilled funding volatility. This isn’t theoretical volatility — it’s the precise month-to-month variability of returns that an actual investor would have lived by way of throughout every rolling interval. The next quantity means your returns bounced round extra violently.

1 12 months Rolling Commonplace Deviation –

The 1-year rolling std dev chart is dominated by the 2008–09 GFC spike. NLM 250 hit over 42% annualised volatility throughout this era — which means month-to-month returns had been swinging by over ±12% in a typical month. Nifty 500 peaked at ~40%, and Nifty 50 at ~38%.

Common 1-year rolling std dev: Nifty 50 18.8%, Nifty 500 19.6%, NLM 250 20.6%. The hole between Nifty 50 and NLM 250 is roughly 1.8 proportion factors on common. For the return premium NLM 250 earns (+2.7% avg CAGR over Nifty 50 at 1 12 months), this isn’t compelling at this horizon — the additional danger is giant relative to further return.

2008 peak: NLM 250 ~42%, Nifty 500 ~40%, Nifty 50 ~38% — real disaster volatility.

Common hole NLM 250 vs Nifty 50: ~1.8pp extra volatility for ~2.7pp extra avg CAGR. Not compelling at 1-year.

Nifty 500 sits barely above Nifty 50 in volatility, confirming its market-cap weighting retains it anchored.

3 Years Rolling Commonplace Deviation –

At 3 years, the GFC volatility spike continues to be seen however unfold throughout extra months. Common 3-year rolling std dev: Nifty 50 19.8%, Nifty 500 20.9%, NLM 250 22.1%. The hole between NLM 250 and Nifty 50 is now 2.3 proportion factors — really wider than at 1 12 months. This reveals an essential reality: mid-cap volatility doesn’t common out shortly. Prolonged durations of midcap underperformance (like 2018–2020) imply that 3-year std dev might be greater than 1-year std dev in some rolling home windows for NLM 250.

Hole widens at 3 years: NLM 250 is 2.3pp extra risky than Nifty 50 on common.

Mid-cap volatility persists at 3 years — it doesn’t “common out” as shortly as many traders assume.

Nifty 500 is only one.1pp extra risky than Nifty 50 — a really modest premium for considerably broader publicity.

5 Years Rolling Commonplace Deviation –

Common 5-year rolling std dev: Nifty 50 19.7%, Nifty 500 20.6%, NLM 250 21.9%. The image at 5 years is crucial for funding decision-making. Take into account the risk-adjusted return comparability:

• NLM 250 vs Nifty 50: +2.1% further CAGR, +2.2pp further std dev – questionable Sharpe enchancment

• Nifty 500 vs Nifty 50: +0.5% further CAGR, +0.9pp further std dev – modest however environment friendly enchancment

• NLM 250 vs Nifty 500: +1.6% further CAGR, +1.3pp further std dev – cheap risk-return at this window.

For a 5-year investor, Nifty 500 presents a greater risk-adjusted premium over Nifty 50 than NLM 250 does. You achieve modest breadth with out taking over disproportionate volatility.

At 5 years: Nifty 500 further std dev vs Nifty 50 = solely 0.9pp. For +0.5% CAGR. Small however optimistic trade-off. NLM 250 further std dev vs Nifty 50 = 2.2pp. For +2.1% CAGR. Massive in each instructions — excessive danger, excessive reward.

Danger-adjusted (Sharpe-like): Nifty 500 beats Nifty 50 effectively. NLM 250 beats each in return, however requires tolerance for sustained volatility.

10 Years Rolling Commonplace Deviation –

The ten-year rolling std dev chart delivers probably the most counter-intuitive discovering on this evaluation. Common 10-year rolling std dev: Nifty 50 18.9%, Nifty 500 19.9%, NLM 250 21.1%. The values have converged considerably in comparison with the 1-year window. The distinction between NLM 250 and Nifty 50 is now simply 2.2 proportion factors on common — for +2.3% common 10-year CAGR benefit. That could be a significant enchancment in risk-adjusted return on the 10-year horizon.

However right here is the important thing perception for the Nifty 500 comparability: at 10 years, Nifty 500 carries only one.0pp extra std dev than Nifty 50 whereas delivering +0.5% extra CAGR. That is a particularly environment friendly trade-off — nearly no further volatility for real further breadth and diversification.

All three converge to 18–22% annualised std dev at 10 years — the hole narrows considerably.

NLM 250: +2.2pp extra volatility than Nifty 50, however +2.3% extra CAGR – improved risk-adjusted image at 10Y.

Nifty 500: solely +1.0pp extra volatility than Nifty 50, and +0.5% extra CAGR – extremely environment friendly at 10Y.

At 10 years, the additional volatility in NLM 250 is actual however considerably diminished. Lengthy-term holders are rewarded.

Nevertheless, it’s essential to have really held for 10 years by way of ?67% drawdowns to grasp this convergence.

Why is the Nifty 500 the Most Appropriate Selection for Most Traders?

After inspecting 21 years of precise information throughout lump sum returns, drawdowns, rolling CAGR, and rolling volatility, we arrive at a thought-about view. The information helps Nifty 500 TRI as probably the most virtually appropriate index for almost all of Indian long-term traders — for the next causes.

1. Nifty 50 Is Too Concentrated to Be Referred to as “Diversified”

Nifty 50 covers simply 55.5% of India’s listed fairness market and solely 50 corporations. In a rustic with over 1,900 listed corporations throughout 21 sectors, a 50-stock portfolio misses 44.5% of the market by worth. It covers solely 14 out of 21 sectors. It’s closely skewed towards Monetary Providers and IT — sectors which occur to be dominant immediately however weren’t all the time so.

The Nifty 50 isn’t a nasty index. It’s wonderful for its goal — monitoring India’s largest companies at minimal price and monitoring error. However calling it a “diversified” fairness portfolio is a stretch by any cheap definition of diversification. If you happen to maintain solely Nifty 50, you may have basically wager your fairness returns on 50 corporations and 14 sectors.

2. NLM 250 Is Structurally Too Dangerous for Most Retail Traders

NLM 250 is a compelling index on paper, and the 21-year information confirms it delivers the very best returns. However three structural points make it unsuitable as a core holding for many retail traders:

• Compelled 50% midcap allocation isn’t pure. Market-cap weight of midcaps in India is roughly 15–18% of NSE. NLM 250 triples that to 50% by mandate. When midcaps underperform for prolonged durations — as they did from 2018 to 2020 — traders face extended, irritating underperformance versus even the Nifty 50. This isn’t a brief section — mid-cap cycles can final 2–3 years.

• Greater monitoring error is a sensible downside. Mid-cap shares are much less liquid. Index funds monitoring NLM 250 systematically endure greater monitoring error in comparison with Nifty 50 and even Nifty 500 funds, on account of impression prices within the mid-cap section. The returns you see within the index aren’t absolutely deliverable in a fund.

• The drawdown depth checks actual behavioural limits. A ?67.6% peak-to-trough fall isn’t a statistic most traders have genuinely internalised. In apply, an investor watching Rs.10 lakhs grow to be Rs.3.24 lakhs will promote — and at that time, all of the theoretical 15.17% CAGR turns into irrelevant. The index’s historic return is simply realisable by traders who held by way of each crash with out promoting.

3. Nifty 500 Is the Rational Candy Spot — Right here Is Why

Nifty 500 resolves all three issues above in a single index:

• True diversification: 92.3% of NSE free-float market cap, 500 corporations, all 21 sectors. That is as near “proudly owning the Indian economic system” as a single index will get.

• Market-cap-weighted and naturally rebalanced: Not like NLM 250’s pressured 50% midcap mandate, Nifty 500’s mid-cap weight (~18.5%) displays precise market proportions. When midcaps appropriate, the burden naturally reduces — built-in danger administration with none energetic choice.

• Decrease drawdown than NLM 250 with higher diversification than Nifty 50: At ?63.7% versus NLM 250’s ?67.6%, Nifty 500 avoids the worst of the mid-cap panic with out sacrificing breadth. And at ?63.7% versus Nifty 50’s ?59.5%, the additional ache is modest for considerably wider protection.

• Beats Nifty 50 in 77% of 10-year rolling durations: This isn’t marginal or unreliable. Over each decade-long window within the dataset, Nifty 500 outperformed Nifty 50 in practically 4 out of 5 cases. The additional return from broader market participation is actual and constant.

• Environment friendly risk-return in any respect horizons: At 10 years, Nifty 500 delivers +0.5% further CAGR versus Nifty 50 for +1.0pp further std dev. That is a particularly environment friendly trade-off — nearly no further volatility for real further breadth and return.

• Decrease structural monitoring error danger than NLM 250: Nifty 500’s larger-cap bias inside its 500 shares means index fund managers face decrease impression prices and tighter monitoring. The index return is extra carefully achievable in apply than NLM 250’s.

92.3% market protection vs 55.5% (Nifty 50) and ~87% (NLM 250) — broadest and most consultant. Beats Nifty 50 in 58%, 52%, and 77% of rolling 3Y, 5Y, and 10Y durations respectively — constant edge.

Max drawdown of ?63.7% vs Nifty 50 (?59.5%) — solely 4.2% further ache for massively wider protection.

Market-cap weighted: midcap publicity (~18.5%) is proportional and self-adjusting — no pressured structural bets. Danger-adjusted at 10 years: +0.5% CAGR for +1.0pp std dev versus Nifty 50. Extremely environment friendly.

Avoids NLM 250’s 50% pressured midcap allocation, greater monitoring error, and deeper drawdowns.

For many SIP traders with a 10-15 12 months horizon, Nifty 500 is the appropriate one-fund fairness answer.

The information from 21 years of precise NSE TRI values is evident. All three indices are good investments over a sufficiently lengthy horizon — the query is which fits your particular state of affairs.

Nifty 50 isn’t “unsuitable” — it’s India’s most confirmed large-cap benchmark with the bottom monitoring error and quickest restoration from crashes. However selecting Nifty 50 means accepting vital focus danger in a 50-stock, 14-sector, 55.5%-market-coverage portfolio.

NLM 250’s 15.17% CAGR is actual and significant — Rs.19.41 lakhs versus Rs.14.29 lakhs for Nifty 50 over 21 years. However most traders who declare they’ll maintain by way of a 67% drawdown won’t really achieve this when they’re residing by way of it. And the pressured 50% midcap mandate introduces prolonged underperformance cycles which are psychologically tough even for knowledgeable traders.

Nifty 500 is the pragmatic, data-backed candy spot: 92.3% market protection, market-cap-weighted pure allocation, beats Nifty 50 in 77% of 10-year rolling durations, avoids NLM 250’s structural mid-cap focus, and retains monitoring error at manageable ranges. For many Indian traders constructing long-term wealth by way of SIPs or lump sum investments, a Nifty 500 index fund is the only most rational core fairness holding.

The Most Necessary Lesson: Behaviour Beats Index Choice

All three indices multiplied Rs.1 lakh into Rs.14–19 lakhs over 21 years. The winner was endurance.

An investor who bought through the 2008 crash (?60 to ?67%) and waited for readability earned a fraction of those returns.

The perfect index for you isn’t the one with the very best again examined CAGR — it’s the one you’ll HOLD through the subsequent main crash with out promoting.

If you happen to can not confidently maintain an index by way of a 60%+ drawdown, don’t purchase that index no matter its historic returns.

Time in market > timing the market > index choice. The information, spanning two main crashes and 21 years, is unambiguous.