A story of two decisions:

Rohit, a 28-year-old architect, working at a multinational in Bangalore, lives a modest life-style. His onerous work reaped him a Rs 3,36,000 promotion final yr after taxes, giving him an additional Rs 28,000 a month. Listed below are two paths that he may select from for utilizing his extra earnings to make life-style modifications:

Path 1: Having fun with all of the fruits of his labor now

- Upgraded to a brand new car @ Rs 20,000 per 30 days

- Upgraded streaming providers or joined a passion membership @ Rs 4,000 per 30 days

- Went out to eat extra typically @ Rs 4,000 per 30 days

Path 2: Planting seeds for the longer term

- Elevated emergency fund @ Rs 4,000 per 30 days

- Made further debt funds @ Rs 8,000 per 30 days

- Invested extra into retirement @ Rs 8,000 per 30 days

- Elevated allowance for “enjoyable” spending @ Rs 8,000 per 30 days

One path sees Rohit use most of his extra earnings to extend his monetary safety. One other exhibits a rise in his spending alongside along with his earnings. This is named life-style inflation and it might have a toll on you earlier than you even understand it, limiting your skill to construct wealth.

Defining life-style inflation

Think about, like Rohit, you bought a job that you’ve been wanting and extra importantly, it got here with a pay elevate that you just had lengthy been hoping for. You might be extraordinarily blissful and begin seeing your self as a wealthier particular person. However three months later, you test your checking account and it has not grown. “What occurred?” you ask your self. “I’m making more cash. Why haven’t I been in a position to save more cash?”

The perpetrator right here is life-style inflation. It happens when an individual’s lifestyle will increase together with their improve in earnings. Individuals develop a way that they “deserve” extra facilities now that they reached their profession objectives or really feel as if they wish to reward themselves. However sadly, this phenomenon can pose a critical threat to your wealth.

Which path must you observe?

By following Rohit alongside the trail of placing further earnings towards debt, financial savings and investments whereas nonetheless having some enjoyable now, you possibly can set your self up for monetary success reasonably than locking in the next price of residing.

How does life-style inflation occur?

The above story is an ideal instance. As an alternative of saving nearly all of cash from a pay elevate, you may seemingly improve your lifestyle. You would be shopping for that particular espresso that you wouldn’t enable your self to have earlier than. Or immediately you could really feel that you just deserve a brand new costly automotive, even when your current automotive travels from vacation spot A to B simply wonderful.

What triggers it?

It isn’t solely pay raises or promotions that set off life-style inflation. A number of different components may also provoke it.

- Social comparisons and the need to maintain up with mates or colleagues

- Shifting to a wealthier neighborhood

- The need for standing and recognition

- Easy accessibility to bank cards and loans which in flip facilitates spending

- With larger earnings, individuals develop a way of entitlement to a greater life and a greater lifestyle

- As people earn extra, they go for extra handy choices (premium providers)

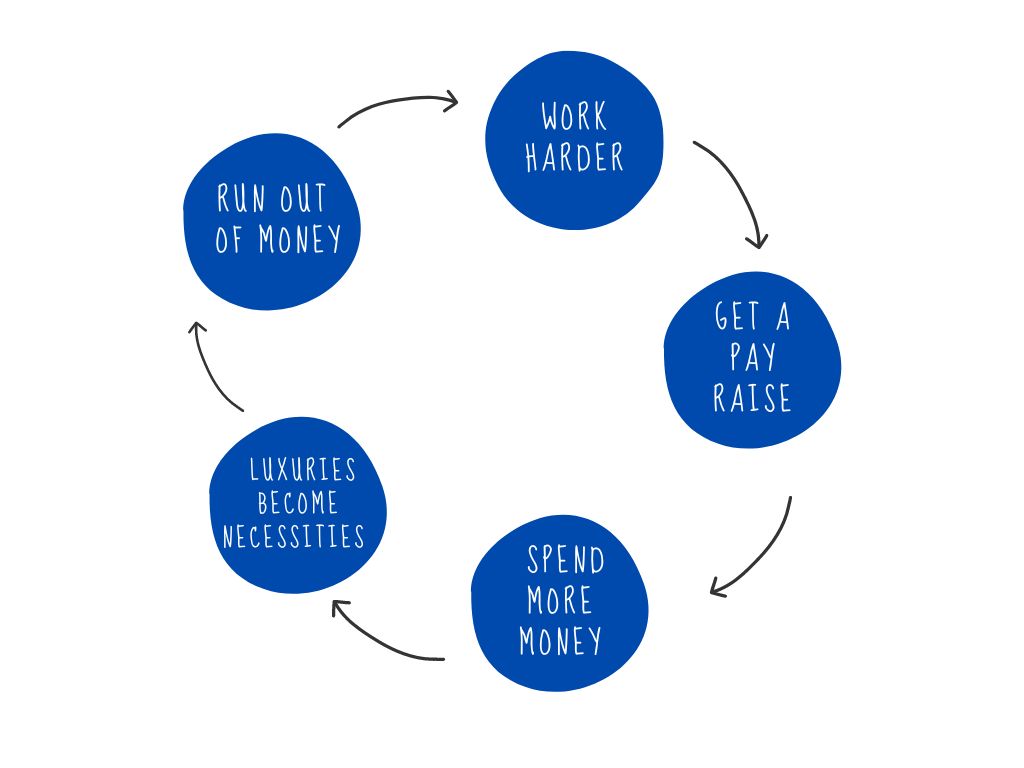

From Raises to Regrets

Each time you get a elevate, life-style inflation tends to grow to be larger. Every wage improve is usually accompanied by an upward adjustment in spending. Slowly and step by step, you get right into a cycle of residing pay test to pay test. Although you could possibly pay your payments, your skill to transform your larger wage right into a approach to construct wealth could get restricted. Within the long-run, this could show to be regrettable as you could be left with minimal funds, debt lure and lack of assets.

Prices related

Life-style inflation can include following prices:

- Elevated monetary obligations resembling larger month-to-month payments and automotive mortgage installments

- Diminished financial savings in addition to retirement contributions and different investments

- Accumulation of debt

- Missed alternatives (elevated earnings may go towards investing in training or a extra significant expertise)

Will I do know that I’m a sufferer of life-style inflation?

Not essentially. Life-style inflation tends to sneak up on individuals. That’s the reason it’s known as life-style inflation. You may not be consciously conscious of the truth that you may have begun spending more cash on luxurious gadgets that will have beforehand appeared to be costly.

What can I do to forestall life-style inflation?

1. Keep a price range:

Making a price range is among the handiest methods to fight life-style inflation. It permits you to check out your funds with out getting your feelings concerned.

2. Allocate to emergency and retirement fund:

Be sure that you allocate sufficient cash to your emergency financial savings and retirement fund. Maintain a relentless focus in your long-term monetary objectives.

3. Rejoice sensible:

You possibly can nonetheless have a good time the truth that you bought a pay elevate. You simply must do it responsibly. Make incremental modifications to your family furnishings as a substitute of shopping for all new without delay.

4. Don’t do something long-term:

Rejoice your success however ensure that it’s a finite factor like a trip, a chunk of jewellery or so. Don’t take pleasure in long-term habits or main commitments.

5. Delay gratification:

Generally, it’s a good suggestion to delay impulsive purchases by giving your self time (possibly a day or every week) to consider whether or not the merchandise is genuinely beneficial or it’s only a fleeting need.

Ultimate ideas

While you work onerous, you need to deal with your self. However just be sure you do it in a method that’s protected and liable for you in addition to your loved ones’s wants.