![]()

Looking for a

profitable

path to core

modernization

Trendy banking is a far cry from the analog processes of yesteryear. Right this moment’s smartphone-wielding clients demand hyper-personalized transactions woven seamlessly into on a regular basis life,

one-to-one private service with their information at brokers’ fingertips, and instantaneous monetary insights—and a few are even urgent for options like blockchain integration and assist

for digital currencies. However the skill to serve these clients just isn’t assured: Gartner predicts that by 2025 greater than 85% of organizations will transfer ahead with cloud ideas,

however won’t but be capable of totally use cloud-native architectures and applied sciences.

These instruments shall be key to banks’ skill to maneuver to digital ecosystem platforms and develop new companies,

associate with different gamers, work successfully with colleagues, and meet buyer expectations.

Monetary establishments are beneath stress to future-proof and accommodate rising applied sciences equivalent to synthetic intelligence (AI), machine studying (ML),

and cloud computing—and they’re additionally dealing with vital infrastructural strains. Whereas some banks of all sizes nonetheless function with a siloed, monolithic system,

they may face growing issue assembly the calls for of a big buyer base and a slew of interconnected digital companies. A 2023 research by analysis agency

IDC and cost software program firm Episode Six initiatives that utilizing outdated expertise

price banks greater than $36 billion in 2022, and will price banks greater than $57 billion by 2028. Governance points, vendor lock-in, workers turnover, and restricted assets are compounding

stressors on legacy programs.

“The phrase ‘core banking system’ has modified dramatically over the previous 50 years,” says Dave Murphy, head of economic companies for Europe,

Center East and Africa and Asia Pacific at Publicis Sapient, a worldwide digital transformation consulting firm. The dramatic modifications in core

banking programs has modified how banks method banking, which modifications how they need to deal with modernization. “When individuals take into consideration modernizing a

core banking system, they’re attempting to interrupt down the issue that was created a long time in the past when it was your complete financial institution in a single system,” he says.

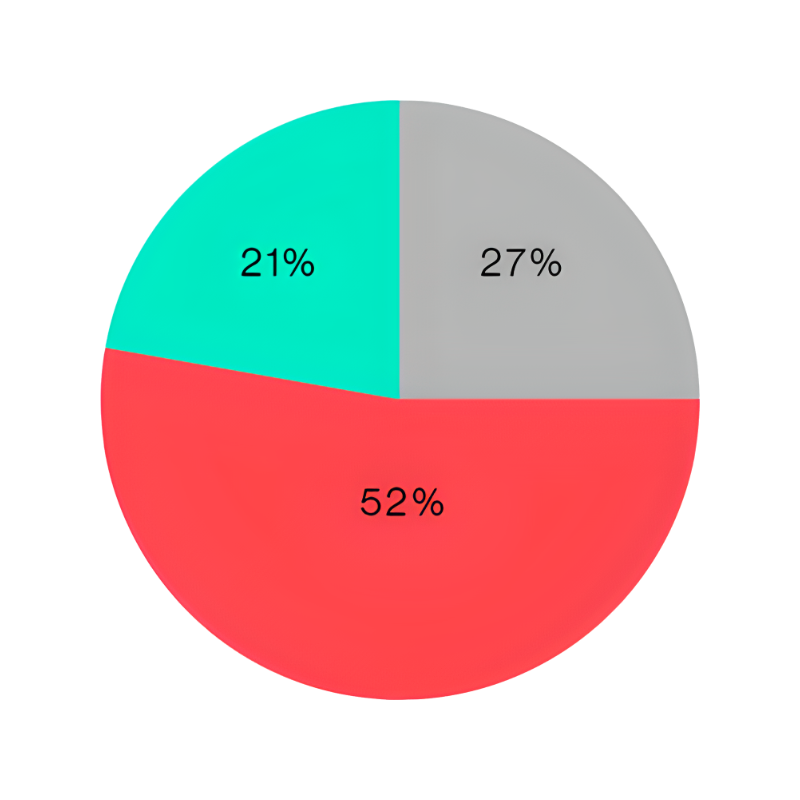

Fewer than one-third of the world’s greatest banks are investing in digital monetary ecosystems

in a “significant manner,” in keeping with 2023 analysis from the Boston Consulting Group. The identical analysis says about 25% of those organizations are investing

in pilot testing core banking programs.

27% Important engagement: The digital ecosystem is strongly linked to the core enterprise.

52% Reasonable engagement: The ecosystem is partially linked to the financial institution’s core enterprise.

21% Minimal engagement: The digital ecosystem is primarily linked to pilots.

At the very least in concept, migrating to a contemporary core can ameliorate all of those points. However executives and compliance groups are apprehensive concerning the danger and energy concerned.

To efficiently clear these hurdles, Murphy says, it’s essential to take end-to-end strategic steps—together with embracing core tenets of the “composable enterprise” and

exploring migration techniques equivalent to purposeful coexistence.

To innovate and handle limitations of legacy infrastructure, there are some conditions when modernization is obligatory—for example,

when resilience points cannot be remedied by further {hardware} or when a vendor goes out of enterprise, leading to an imminent end-of-life state of affairs.

Even in less-drastic circumstances, legacy programs go away a lot to be desired. Monetary establishments have turn into bigger and extra sprawling

via acquisitions and buyer development through the previous a number of a long time, which means ingrained monolithic applied sciences are supporting rather more

than they had been initially designed for. Working on these antiquated programs, banks typically have issue responding to market shifts like

rate of interest modifications or demand for brand spanking new merchandise equivalent to buy-now-pay-later (BNPL) purposes. Governance points, too, are a rising concern,

as regulatory compliance necessitates nimble programs that may simply adapt to altering legal guidelines and requirements.

What’s extra, the ageing nature of legacy programs poses personnel challenges. Murphy notes that there’s a shrinking pool of consultants accustomed to older banking applied sciences.

“There are vital abilities and data gaps,” he says. “Lots of these programs had been created a very long time in the past, and admittedly, individuals are not studying these back-end applied sciences—issues

like COBOL or Meeting—nowadays.” Developed within the late Nineteen Fifties, COBOL performs a foundational (and a rising) position in banking programs, in keeping with a 2022 survey of enterprise customers by

market researcher Micro Focus: 92% of respondents stated COBOL is strategic for his or her enterprise, and greater than half anticipate to nonetheless be utilizing it in 10 years.

59% Legacy infrastructure

53% Lack of real-time entry to information

51% Lack of agility

47% Ineffective information methods

44% Discovering the precise companions

39% Compliance challenges

38% Lack of digital expertise

These challenges are compelling causes to pursue core modernization. However some approaches like “large bang” migrations, wherein a corporation switches

to a brand new system all of sudden, have confirmed disastrous time and time once more. Partially due to debacles just like the UK’s

TSB Financial institution system transition in 2018—throughout which

clients had been locked out of their accounts, confidentiality was compromised, and funds had been misappropriated—this migration tactic has turn into

synonymous with service disruptions, failures, and regulatory penalties.

An enormous bang methodology, Murphy says, “positively has turn into an unfeasible method, primarily as a result of I feel there’s been sufficient case examples of disasters created

by it,” explains Murphy. On paper, he says, it might seem sooner and due to this fact inexpensive. However the monitor report of huge bang transformations

like TSB Financial institution has drawn consideration to the necessity for coexistence between outdated and new programs for an extended time period, he says.

“Individuals are actually requesting extra of an incremental migration,” Murphy says.

An incremental method is barely possible when monetary establishments have a supporting framework in place.

That is the place the idea of the composable enterprise comes into play. Gartner defines a composable enterprise as infrastructure

produced from interchangeable constructing blocks, which allows agility in response to new calls for, visitors spikes, manufacturing points, or provide chain challenges.

Changing into composable entails deconstructing large, unwieldy programs into extra versatile, modular elements, effecting not only a financial institution’s expertise construction,

however its working mannequin. This method not solely frees the backend, but additionally facilitates collaboration throughout a broader spectrum of answer suppliers.

Placing information on the core, it ensures a extra seamless person expertise as banks experiment with modernizing companies in a extra piecemeal trend.

“You need to restrict the change {that a} buyer sees whenever you’re modernizing your structure,” explains Murphy. “Essentially, when you’re

offering them with the identical service however forcing them to alter their behaviors since you’ve modified programs, that may be fairly troublesome to handle.”

Additional, modularity could be a springboard for innovation, permitting establishments to improve elements like buyer identification or fraud detection

and not using a complete overhaul, Murphy says. It additionally lets banks check and be taught from small parts of their buyer or product portfolio,

unlocking potential development alternatives.

These development alternatives emerge, largely, from higher use of information. A 2023 survey of U.S. banking leaders by Forbes and banking software program firm Thought Machine discovered

respondents (63%) take into account their buyer information

a big aggressive benefit.

“Certainly one of your biggest property as a financial institution is the info—possession, with the ability to entry it, leverage it in real-time, and apply it to modern areas like AI,” says Murphy.

“So, it’s essential to free your self up so that you even have possession of your information and entry to it. Then, you possibly can start to compose a set of options in your clients round it.”

“Certainly one of your biggest property as a financial institution is the info—possession, with the ability to entry it, leverage it in real-time, and apply it to modern areas like AI.”

Dave Murphy, Head of Monetary Providers for Europe, Center East and Africa and Asia Pacific, Publicis Sapient

Alongside composability, a method of purposeful coexistence

performs a central position in an efficient core modernization journey. This transitional tactic entails working outdated and new core programs concurrently,

leading to much less danger, and resulting in a extra phased, calculated, and strategic migration.

Murphy says this method is complementary to the composable enterprise mindset. “It’s a complete lot tougher to consider coexistence if

you’re not eager about your establishment or financial institution as a composable enterprise. For those who’re shifting from one monolith to a different,

you are successfully shifting from two black packing containers, which could be very troublesome,” he notes.

Latest analysis by Publicis Sapient

on core banking transformation factors out that separating migration and coexistence methods might help guarantee every is executed with focus and

experience. Different components which may increase success charges embody implementing a typical information layer for environment friendly aggregation, a routing layer for

optimized information distribution, and strategic “hollowing out of the core” to supply modules for each legacy and new programs.

The analysis emphasizes the importance of automated reconciliation utilizing superior applied sciences for streamlined information integration, in-depth evaluation

of legacy information to make knowledgeable migration choices, and testing coexistence methods in a stay setting for early danger mitigation. Planning for

the decommissioning of the older system can also be important to appreciate price financial savings and guarantee stakeholder dedication all through the modernization course of.

Embrace coexistence and empower a central staff. This staff wants senior sponsorship, and the power to make troublesome choices at tempo.

Don’t attempt to reply all questions in the beginning. Let the central staff set a north star early on, lay the implementation path, and work via every problem.

Use expertise to raised assist coexistence. Use the goal structure to allow coexistence, so interim builds can extra simply be modified as you transition.

Determine your coexistence management factors. The less factors you could management to flip from one coexistence state to a different, the higher.

Tactically spend money on legacy. Plan these modifications early with the groups supporting the legacy core, together with third events.

Separate migration and coexistence. Knowledge migration is shifting information from A to B. Coexistence is a state the financial institution will function for a number of weeks to a number of years.

Construct a typical information layer. A standard information layer aggregates information and feeds downstream programs, minimizing downstream influence.

Create a routing layer. An information cache answer permits the routing layer to make environment friendly and clear routing choices.

Take into account domains and capabilities. Construct essential enabler domains—like buyer or cost—to make sure they’re already disaggregated.

Spend money on automated reconciliation. The necessity to reconcile information sources will materially enhance throughout coexistence.

Go deep on the coexistence information evaluation. Don’t run on assumptions concerning the core legacy information and which coexistence states it’s essential to cater for.

Take a look at and show coexistence in manufacturing early. There could also be a chance to de-risk any cutover to a coexistence state.

Plan for decommissioning of the legacy property early. Guarantee the associated fee financial savings for this system is known, tracked, and occurs as early as potential.

Purposeful coexistence can set a powerful basis for digital transformation efforts together with core modernization.

“The objective with purposeful coexistence is to attenuate the modifications that downstream reporting and normal ledger programs see—and to actually

preserve it centered on incremental enhancements between these two layers,” explains Murphy. “Although you must be very good about it,

it is frankly the one transfer banks could make as we speak, given our 24/7 related world and its huge calls for.”

“Although you must be very good about it, it is frankly the one transfer banks could make as we speak, given our 24/7 related world and its huge calls for.”

Dave Murphy, Head of Monetary Providers for Europe, Center East and Africa and Asia Pacific, Publicis Sapient

Financial institution management are obliged to consider the strategic outcomes, Murphy says. Modernization can imply banks are prepared for elementary market-level improvements,

and developments like generative AI. “One consequence is the boldness that you simply actually have a resilient structure that may proceed to reply to the large

calls for clients are placing in your financial institution, that you simply frankly by no means had earlier than,” he says. “Resilience could not drive high line development, however it’s going to permit you to

keep in enterprise,” Murphy says.