For components of three many years, one in every of TV’s hottest exhibits has been “Whose Line is it Anyway?”, the spinoff of a UK improv present that used a rotating forged of actors, plus a musician and a slew of improv video games to get audiences laughing. Certainly one of Whose Line’s extra fashionable video games is named “Stand, Sit, Lie.” Actors are given a scene that they should act out, however through the scene, one actor should be sitting, one should be standing, and one should be mendacity down. If an actor adjustments place, the opposite actors should transfer rapidly to fill the empty area. If the standing actor sits down, the sitting actor has to face up. If the one sitting lies down…you get the image. Roles and positions change steadily.

SMB firms and Group & Voluntary Advantages insurers, brokers, and brokers are additionally shifting roles, seemingly at random. Roles will not be solely in flux, however they’re additionally nearly improvisational. SMB firms that used to lie down and anticipate brokers to feed them advantages are actually sitting up and trying to find their very own via totally different distribution channels. Insurers are increasing from brokers or brokers are actually standing up with new services and products and looking for further accomplice and channel choices.

Knowledge’s position can be in movement. For years, Group & Voluntary insurers have used comparatively little “suggestions” information to tailor insurance coverage or companies. There was little or no plan customization. There was nearly no worker personalization for many advantages. In lots of instances, worker information was held merely as a reputation in a gaggle document. Insurers relied upon year-over-year claims expertise and utilization information to adapt pricing. In the present day, nonetheless, staff and companies are keen to share extra related information, however Group & Voluntary insurers are struggling to determine find out how to put it to good use.

What insurers actually need is a holistic have a look at:

a.) giving staff experiences they don’t wish to hand over after they depart the corporate,

b.) enhancing their relationships and connections with value-added companies, and

c.) how their applied sciences develop employer curiosity and broaden product and channel choices.

Function-reversals and adjustments can be wanted, however with the intention to add roles and stay productive, insurers might want to perceive how they will use know-how to construct their companies. It’ll require new makes use of of information, value-added companies, and channel choices.

To provide everybody concerned higher insights into the Group & Voluntary market and alternatives, Majesco SMB survey information and Insurer survey information from our 2023 studies was used to match and distinction the place every participant thinks they’re, versus the place every participant is planning on going. Do these shifts match demand or will overlapping roles diminish everybody’s ROI? For an in-depth have a look at the outcomes, you possibly can obtain, Bridging the Buyer Expectation Hole for Group and Voluntary Advantages.

The Significance of Knowledge & Analytics for Group & Voluntary Advantages

The significance of capturing, enriching, and utilizing information for figuring out alternatives after which delivering a related and interesting expertise for workers is essential for Group and Voluntary advantages suppliers in as we speak’s digital period. Whether or not the information is structured, unstructured, real-time IoT, or machine-generated, it should be leveraged by superior analytics to allow the creation of tailor-made propositions and extra compelling buyer experiences…aligning worker must the suitable services and products, thereby creating deeper belief, loyalty, and engagement.

There is a chance throughout enrollment to supply steerage on merchandise based mostly on their information. Shifting past the once-a-year enrollment can be a possibility to broaden merchandise and worth. Simply contemplate, the delivery of a kid, getting into faculty, buy of a brand new dwelling, getting a brand new pet, switching to a Gig employee standing, or retirement are all occasions or cases the place the worker’s danger wants change however could also be missed alternatives for insurers. Does this must be the case – particularly with the demand for particular person and Gig merchandise rising? Might we seize extra employee-related information internally and externally to information them in choosing insurance coverage advantages when wanted, not simply yearly? Sure, if we rethink how we do enterprise. Something that helps the worker make the suitable selections on the proper occasions creates buyer loyalty and worth.

SMB Buyer – Insurer Gaps for Knowledge Sources and Applied sciences

Structured, unstructured, transactional, real-time, and third-party information throughout the Group and Voluntary advantages spectrum can be utilized to drive revolutionary data-led propositions, improved underwriting and claims, and finally enhanced buyer experiences. SMB clients and their staff, significantly Millennials and Gen Z are greater than keen to supply a broader vary of information for personalization, as represented in Determine 1. Nonetheless, insurers will not be utilizing this information successfully, creating a big buyer expectation hole.

As extra staff search for entry to worksites or particular person merchandise which might be simply transportable, having them priced based mostly on their private danger moderately than as a part of the group can be more and more demanded. As well as, use of the information and different demographic components can be utilized to counsel particular merchandise throughout the profit plan which might be extra aligned with their wants and expectations at enrollment, driving larger product adoption. That is one thing Majesco Clever Core for L&AH and Clever Gross sales and Underwriting Workbench do for our clients. It’s why we name them “clever options.”

Determine 1: SMB-Insurer gaps in new information sources and applied sciences for group/voluntary advantages pricing and underwriting

Main Insurers Navigating the Gaps Utilizing New Strategies or Knowledge Sources

Listed below are some examples of insurance coverage improv in motion. All three of those insurers reached exterior of their conventional roles to supply a profit or service related to tendencies or improvements from exterior the trade.

- Aflac launched dental, imaginative and prescient, and listening to plans for people pursuing contract, Gig, or solo entrepreneurial work exterior conventional workplaces or getting into retirement.[1]

- A number one advantages supplier launched a brand new essential sickness product that gives DNA testing to assist customized most cancers therapies.

- Beam Insurance coverage launched a brand new dental product that features a good toothbrush to observe brushing for improved well being.[2]

Worth-Added Providers for Group & Voluntary Advantages

A key technique for insurers to handle buyer expectations is to extend the worth of the merchandise they provide. To take action, insurers ought to bundle, or provide for a value, value-added companies that stretch the worth of the chance product/coverage, comparable to incomes factors for wellness that can be utilized to purchase issues, annual monetary planning evaluation, roadside help, claims help and extra.

Worth-added companies can create new income alternatives whereas additionally strengthening the client relationship, loyalty, belief, and worth. Usually, these match into the position of monetary wellness. It’s the place our partnership with Empathy to boost the claims course of provides great worth.

SMB Buyer – Insurer Gaps for Worth-Added Providers

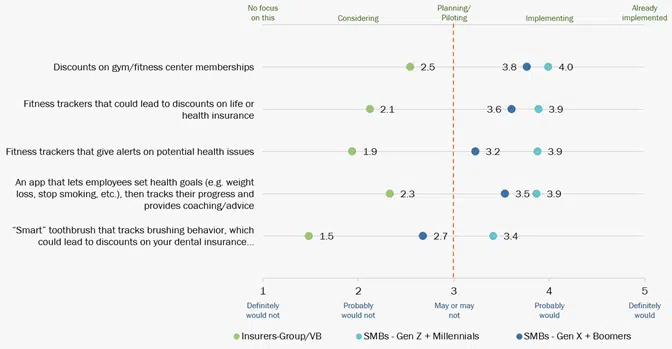

Throughout the board, there’s a vital buyer expectation hole between what clients need – no matter generational group – and what insurers are delivering, as represented in Determine 2. These value-added companies present tangible worth and improve total wellness with alerts and extra.

As well as, these choices might collect extra customized information to boost their pricing in addition to their total expertise. Many are “low hanging fruit” that will not take lots of effort, however create great worth and begin insurers down the street to a extra holistic, valued providing and expertise for purchasers. A lot of the worker well being and wellness information wanted for value-added companies or data-supplemented merchandise is already accessible as we speak via sources comparable to Fitbit, Apple, and Strava APIs — insurers can merely benefit from accessible information. Employers and staff are rising rather more amenable to sharing after they see the worth in offering it.

Determine 2: SMB-Insurer gaps in value-added companies for group/voluntary advantages

Main Insurers Navigating the Gaps with Worth-Added Providers

Listed below are some examples of firms which might be making it occur. They’re enhancing their merchandise as they encourage way of life and wellness enhancements amongst worker populations.

- EquiTrust Life Insurance coverage Firm partnered with Assured Allies to supply its Bridge fastened listed annuity with a long-term care rider policyholders entry to Assured Allies’ NeverStop information and analytics-based wellness program.[3]

- YuLife within the UK wraps their group safety proposition with their worker well-being app, offering entry to well-being monitoring and counseling companies, and reward companions to construct a extra partaking proposition for the worker whereas additionally offering companies to the employer to extend staff’ productiveness and loyalty.[4]

- Vitality presents a variety of value-added companies which might be targeted on wellness and are partnering with totally different insurers globally like John Hancock.

Distribution Channels for Group & Voluntary Advantages

Within the conventional distribution mannequin, insurers battle for a share of thoughts and pockets, so clients consider them after they want insurance coverage. Many giant insurers spend lots of of hundreds of thousands of {dollars} on promoting and others spend vital {dollars} within the conventional agent/dealer channel, to maintain them “high of thoughts” when insurance coverage is required. With the growing aggressive challenges to draw and retain clients, insurers should develop and make the most of a broader distribution ecosystem that engages clients when and the way they need…placing the client first.

In the present day’s interconnected world requires insurance coverage to play throughout a broad distribution spectrum of channel choices, increasing attain to clients when, the place, and with whom they wish to purchase insurance coverage. These choices kind a distribution ecosystem that expands attain however requires a partnership strategy, significantly for embedded channels.

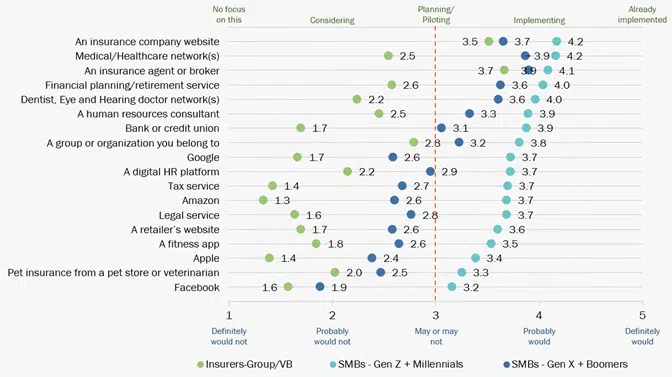

SMB Buyer – Insurer Gaps within the Pursuit of Distribution Channels

In the present day’s consumers nonetheless look to brokers and brokers, however will look to purchase insurance coverage via different channels or entities as nicely, as mirrored in Determine 3. SMBs are leveraging different trusted and dependable relationships that make shopping for insurance coverage via them related, significantly for the Millennial and Gen Z SMB homeowners.

This buyer expectation hole displays how group and voluntary profit insurers are limiting their market attain to this very giant and under-supported market phase.

Determine 3: SMB-Insurer gaps in distribution channels for group/voluntary advantages

Main Firms Coming into the Business by Taking over New Roles

- Highlighting the GAFA firm choices, some analysts are predicting Apple will enter the medical insurance market in 2024, leveraging wealthy health and well being information gathered from hundreds of thousands of Apple Watch customers[5] which is able to instantly align with their need for customized insurance coverage utilizing information from health trackers as famous beforehand.

- ADP works with some insurers to supply profit plan choices to SMBs, given they’ve a broader trusted relationship to handle HR and payroll wants.[6]

The Payoff — Taking over New Roles

As a substitute of constant the decades-long battle for a share of the identical giant employer market, we now have an unmet market alternative with small and medium employers. The expansion alternatives are fairly astounding. Over 50% of staff work in an SMB firm. We have to take a step again to rethink how that market must be served, and the way we will present advantages to a vastly modified worker work setting and market.

There’s an enormous space of untapped alternatives in diversified performs past the standard coverages provided. Whereas the anchor propositions for employer plans are healthcare and retirement companies and conventional group covers for defense and incapacity, increasing past this common set is essential to shut the client expectation hole and drive progress.

Most of those payoffs can be discovered underneath classes of new services and products (using information in new methods), new relationships (utilizing untapped partnerships and channels), and further capabilities (offering employers with instruments that save effort and time, together with giving larger insights.) Every of those areas must be approached holistically utilizing a recent strategy to operations plus a tech transformation that features the usage of AI, machine studying, and clever core system design.

Majesco offers Group & Voluntary insurers a lift into new markets and channels by offering them with applied sciences that expertly match the calls for of the brand new, improvisational market panorama. To study extra about how Majesco helps construct a brand new framework for Group & Voluntary progress, go to Majesco’s Clever Core for L&AH, Clever Gross sales & Underwriting Workbench, Digital Enroll360 for L&AH, and Majesco ClaimVantage Enterprise Claims Administration for L&AH. Be sure you additionally obtain Bridging the Buyer Expectation Hole for Group and Voluntary Advantages.

[1] “Aflac Dental, Imaginative and prescient and Listening to Plans Now Obtainable to People Outdoors the Conventional Worksite,” PR Newswire, October 13, 2022, https://www.prnewswire.com/news-releases/aflac-dental-vision-and-hearing-plans-now-available-to-individuals-outside-the-traditional-worksite-301648479.html

[2] McGrath, Jenny, “Beam needs to provide you a sensible toothbrush, then use the information to your dental insurance coverage,” Digital Developments, August 26, 2015, https://www.digitaltrends.com/dwelling/beam-technologies-introduces-dental-insurance-with-its-smart-toothbrush/

[3] Shashoua, Michael, “Assured Allies companions with EquiTrust on long-term care insurance coverage,” Digital Insurance coverage, December 8, 2022, https://www.dig-in.com/information/assured-allies-equitrust-launch-ltc-wellness-program

[4] Macgregor, Jamie, McCoach, Dan, “Subsequent-Gen Platforms in Group and Voluntary: Exploiting new alternatives throughout the worksite ecosystem,” Celent, August 26, 2021, https://www.majesco.com/white-papers/next-gen-platforms-in-group-and-voluntary/

[5] Collins, Barry, “Apple Will Launch Well being Insurance coverage In 2024, Says Analyst,” Forbes, October 18, 2022, https://www.forbes.com/websites/barrycollins/2022/10/18/apple-will-launch-health-insurance–in-2o24-says-analyst/amp/

[6] Small enterprise worker advantages, ADP, https://www.adp.com/sources/articles-and-insights/articles/s/small-business-employee-benefits.aspx