In the event you’re 45 years previous and really feel behind on retirement financial savings, you’re not alone. Life occurs. Possibly you have been elevating youngsters, paying down a mortgage, supporting a sick member of the family, or just didn’t perceive the significance of investing earlier on.

Now, age 60 is barely 15 years away, and the considered relying solely on Canada Pension Plan (CPP) and Outdated Age Safety (OAS) for retirement earnings doesn’t really feel very snug.

It’s true that youthful traders have an enormous benefit. They’ve time to compound and get well from bear markets. However being 45 doesn’t imply you’re out of choices. It simply means the margin for error is smaller and the self-discipline required is greater.

In order for you a sensible shot at catching up, the components is straightforward: max out your Tax-Free Financial savings Account (TFSA) yearly and make investments it in a low-cost S&P 500 index exchange-traded fund (ETF). It’s aggressive. It requires a excessive danger tolerance. However it could actually work.

Begin With Your TFSA

For 2026, the TFSA contribution restrict is $7,000. That will not sound like a lot, however over 15 years, that’s $105,000 in new contributions alone (assuming they don’t hold climbing the annual restrict).

The TFSA is highly effective as a result of all funding development inside it’s tax-free, whether or not from dividends, curiosity earnings, or capital features. Furthermore, withdrawals can occur anytime and are usually not topic to tax.

In contrast to a Registered Retirement Financial savings Plan (RRSP), you don’t get a tax deduction upfront. However the flexibility and tax-free compounding make the TFSA extremely useful, particularly in case your earnings in retirement will not be dramatically decrease than it’s immediately.

In the event you can, lump sum the $7,000 originally of every yr. Traditionally, investing earlier has produced higher outcomes than ready. If that makes you nervous, you possibly can dollar-cost common by splitting the $7,000 into month-to-month or weekly contributions.

Why the S&P 500?

With solely 15 years to work with, you seemingly want significant fairness publicity. The S&P 500 represents 500 massive, established U.S. corporations that generate earnings, reinvest in development, purchase again shares, and pay dividends. Over time, these forces compound. You’re shopping for the market and letting capitalism do the work.

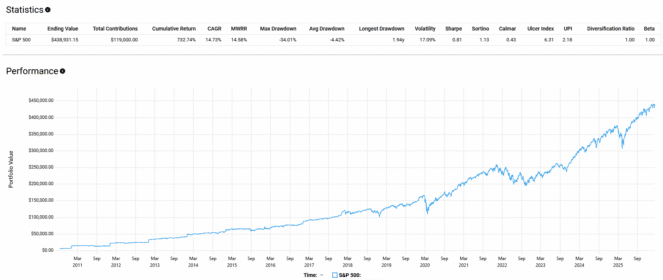

Think about the interval from September 2010 to February 2026. An investor who began with $7,000, added $7,000 yearly, reinvested all dividends, saved charges low, and held the whole lot inside a TFSA would have contributed $119,000 in whole. The ending worth of that portfolio would have grown to $438,931.15. That represents a 14.73% annualized return and a cumulative achieve of 722.7%.

Nevertheless it was not a clean trip. In a median yr, the portfolio swung roughly 17% up or down. Throughout the March 2020 COVID crash and the grinding 2022 bear market, the utmost drawdown reached 34.01%. In the event you pursue this technique, you need to settle for that sharp non permanent losses are a part of the method. The largest danger will not be volatility itself. It’s abandoning the plan on the worst attainable second.

To maintain extra of the return working for you, charges should keep low. One easy Canadian-listed possibility is BMO S&P 500 Index ETF (TSX:ZSP), which costs a 0.09% expense ratio. Meaning simply $9 per yr for each $10,000 invested.

This strategy will not be assured to make you entire. Markets don’t promise something. However constant TFSA contributions, broad diversification via the S&P 500, reinvested dividends, and the self-discipline to remain invested offer you a preventing likelihood.