Wildfire threat is strongly conditioned by geographic concerns that fluctuate extensively amongst and inside states. The newest Triple-I Points Temporary reveals how that reality performed out in 2024 and early this 12 months and discusses the significance of granular native knowledge for underwriting and pricing insurance coverage in wildfire-prone areas, in addition to for much-needed funding in resilience.

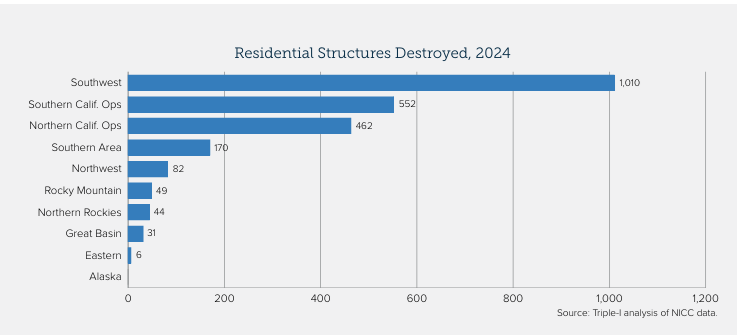

The 2024 wildfire season within the South and Southwest was notably extreme, marked by such occasions because the Texas and Oklahoma Panhandle fires in February and March and important blazes in Arizona and New Mexico. The Southwest accounted for the most important variety of residential buildings destroyed by wildfire, and three of the highest 5 areas for houses destroyed had been within the South.

California accounted for the most important variety of houses in danger for excessive wildfires. Within the first half, the state skilled an above-average variety of fires, although most had been contained earlier than rising to “main incident” dimension. Subsequent rains suppressed subsequent wildfire circumstances – and prompted substantial flooding.

However this rain contributed to an accumulation of fuels in order that, when hurricane-force Santa Ana winds whipped by way of Los Angeles County in early January 2025, the circumstances had been proper for fast-moving blazes to tear by way of Pacific Palisades and Eaton Canyon.

Temperature, humidity, wind, and topography fluctuate too extensively for a single “one dimension matches all” mitigation strategy. This underscores the significance of granular knowledge gathering and scrupulous evaluation when underwriting and pricing insurance coverage. Additionally it is necessary that insurers proactively have interaction with various stakeholder teams to advertise funding in mitigation and resilience.

A latest paper by Triple-I and Guidewire – a supplier of software program options to the insurance coverage trade – makes use of case research from three California areas with very completely different geographic and demographic traits to go deeper into how such instruments can be utilized to determine properties with engaging threat properties, regardless of their location in wildfire-prone areas.

Be taught Extra:

Getting Granular to Discover Decrease-Danger Properties Amid Wildfire Perils

Regardless of Progress, California Insurance coverage Market Faces Headwinds

California Finalizes Up to date Modeling Guidelines, Clarifies Applicability Past Wildfire