On the subject of managing cash, all people simply merely needs a hack that may multiply their cash manifolds. However wealth creation is just not a two-minute train, fairly it’s a complete course of that includes a stability of budgeting, investing and saving. In reality, there are some thumb guidelines of private finance that may information you in the direction of a safe monetary future. Whether or not you’re simply beginning out in your monetary journey or are already on the trail, trying to refine your current methods, these easy-to-follow guidelines can present a stable basis for reaching your financial targets.

Let’s discover the high 10 guidelines that may remodel your monetary journey and enable you to handle your cash correctly:

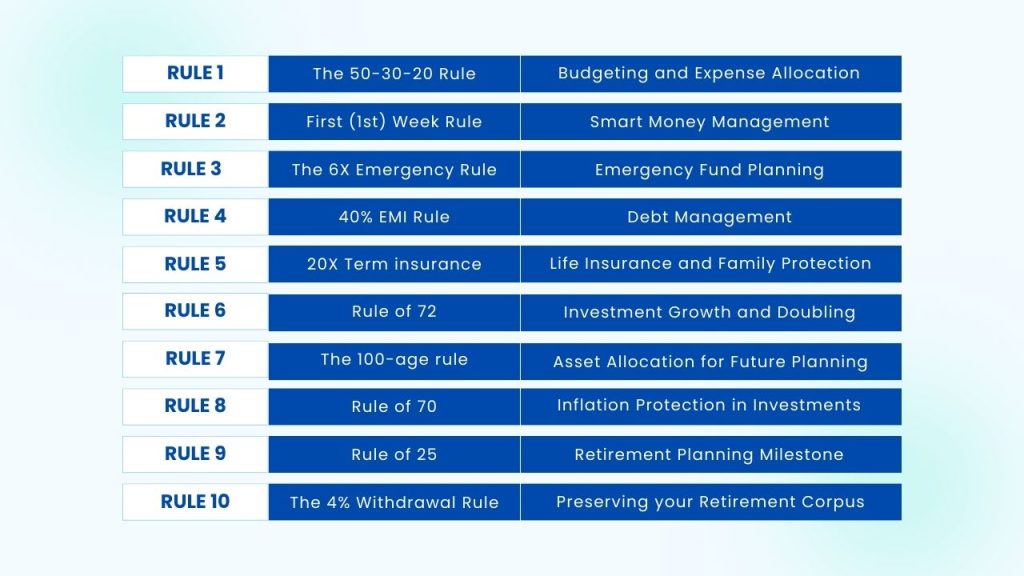

1) The 50-30-20 Rule

The 50-30-20 rule is likely one of the most extensively used and easy to know budgeting practices. In response to the rule, an individual’s take-home pay needs to be divided into three classes: wants (50%) needs (30%) and financial savings (20%). 50% of your revenue needs to be put aside for wants (insurance coverage, kids’s training), the subsequent 30% of your revenue can be utilized to fulfil needs (pursuing a passion, taking a trip), and the remaining 20% should be allotted in the direction of financial savings and investments.

The simplicity of the rule resides in its ease of comprehension and software, which permits every particular person to put aside a particular a part of their month-to-month revenue for financial savings. Folks ought to maintain monitor of their expenditures, particularly if they’ve problem saving cash on the finish of every month.

2) First (1st) Week Rule

The First Week Rule is a great option to handle your cash. It suggests saving and investing 20% of your revenue proper at the start of the month, i.e., within the first week itself. This early motion helps you construct a behavior of accountable monetary behaviour.

For impulsive customers, the rule advises ready every week earlier than shopping for one thing shiny and new. Take that point to consider the acquisition’s worth, potential return, and if there are higher methods to make use of the cash. If you happen to nonetheless really feel strongly about it after every week, go forward. However usually, this pause helps you understand you don’t actually need it, saving you cash in the long term.

3) The 6X Emergency Rule

To be on a safer facet, it’s all the time advisable to maintain a minimum of six occasions the sum of money that you simply spend in a month in the direction of your emergency fund. This cash can assist you out if one thing goes unsuitable like shedding a job or a sudden medical emergency. For instance, in case your month-to-month bills are Rs 50,000 lakh, you need to maintain Rs 3 lakh in your checking account to handle unexpected circumstances.

4) 40% EMI Rule

One other rule that will help you maintain your funds in examine is the 40% EMI rule. Debt administration is a essential a part of monetary well-being. The 40% EMI mantra means that the entire debt / EMI that you simply pay in the direction of a mortgage or bank card fee mustn’t exceed 40% of your web revenue. Merely stated, should you plan to purchase a home (or anything) with a take-home revenue of Rs 1 lakh, be sure the EMI is lower than Rs 40,000. This ensures that you’ve sufficient room in your finances for different mandatory prices and financial savings.

5) 20X Time period insurance coverage

Now, allow us to now focus on the “20x time period insurance coverage rule.” Life insurance coverage isn’t one thing we like to consider, but it’s an integral part of a sound monetary technique. Assume you’re the breadwinner in your family and earn Rs 5 lakh per 12 months. In response to the 20x rule, you need to take into account buying a life insurance coverage coverage that pays out Rs 1 crore within the occasion of the unthinkable. Why one crore rupees? It’s so simple as Rs 5 lakh x 20.

6) Rule of 72

Talking of funding, let’s meet the rule of 72. This rule serves as your crystal ball for predicting when your investments will double in worth. It calculates the variety of years it can take to double your cash at a sure fee of return.

Assume you’ve invested Rs 1,00,000 in an funding that pays you 12% per 12 months. Merely divide 72 by 12, and also you’ll uncover that your cash will double in round six years. That unique Rs 1,00,000 will develop into Rs 2,00,000. Equally, should you get 4% curiosity, divide 72 by 4 to get the variety of years it can take to double the cash, which is eighteen years.

7) The 100-age rule

The following rule is the “100-age rule”. It’s much like selecting the right elements for a meal. Your belongings are the elements on this state of affairs, and the recipe is your monetary future. The rule is straightforward: that you must subtract your age from 100 to get the quantity of your funds that needs to be invested in riskier belongings equivalent to fairness. So, should you’re a wholesome 32-year-old, the rule suggests investing roughly 68% of your financial savings within the inventory market and the remaining 32% in safer belongings equivalent to debt mutual funds or FDs.

8) Rule of 70

One other glorious rule for planning your cash is the rule of 70 – a secret weapon in opposition to the hidden menace to your wealth, i.e., inflation. Inflation erodes the worth of your cash over the time frame.

Now, right here’s the key. The rule of 70 helps you identify as to when your cash will lose half its buying energy. If the inflation fee is 6%, that you must simply divide 70 by that share (6). The consequence, 11.67, tells you that your cash’s buying energy will minimize in half as a consequence of inflation in roughly 11.67 years to return.

Figuring out this, you may make intelligent decisions together with your investments to remain forward of inflation’s sport and ensure your cash retains its worth over time.

9) Rule of 25

Let’s now speak in regards to the rule of 25. In response to this rule, you need to intention to avoid wasting a complete quantity equal to 25 occasions your annual bills earlier than contemplating retirement.

Right here’s a easy breakdown: In case your yearly bills quantity to 16 lakhs, the Rule of 25X suggests considering retirement after getting a financial savings corpus of Rs 4 crore (16 lakhs multiplied by 25). It’s essential to notice that this isn’t a strict deadline however extra of a milestone to assist information your journey towards monetary independence in retirement.

10) The 4% Withdrawal rule

One other golden rule that will help you protect your retirement financial savings is the 4% withdrawal rule. In response to this rule, when you have a Rs 1 crore retirement fund, you possibly can withdraw Rs 4 lakh (4% of 1 crore) within the first 12 months of retirement. To maintain up with rising costs, you possibly can enhance your annual withdrawal by the inflation fee. As an example, if inflation is 5%, you’d withdraw Rs 4 lakh 20 thousand within the second 12 months and Rs 4 lakh 41 thousand within the third 12 months, and so forth. The concept is to strike a stability: withdrawing sufficient on your wants whereas guaranteeing your cash lasts all through your retirement interval, i.e., for about 30 years to cowl bills.

Remaining phrases

Keep in mind, these thumb guidelines don’t depict a “one measurement match all” resolution. They’re extra like stars within the evening sky that information you thru the darkness however help you chart your individual plan of action.

Your monetary journey is sort of a distinctive journey and these guidelines are like your useful guides. They don’t seem to be strict guidelines, however they are going to level you to maneuver in the precise course when you find yourself a bit misplaced within the cash maze. So, by incorporating these 10 monetary guidelines into your life, you possibly can simplify the method of managing cash and dealing in the direction of your monetary targets.