KEY

TAKEAWAYS

- The inventory market indices closed increased for the day however ended the week decrease

- The ten-year Treasury yield closed increased at 4.04%

- Regardless of the pullback in equities, the inventory market indices are nonetheless trying technically robust

You’ll be able to’t blame the marketplace for taking a breather after 9 constructive weeks.

The primary buying and selling week in January ended decrease, which can have involved traders. It is comprehensible how jittery traders are once you view the market’s response to the December jobs report. The roles information got here in higher than anticipated, which despatched ripples by way of Wall Avenue. Proper after the info was reported, fairness futures fell, and Treasury yields ticked increased.

Nevertheless, traders overcame the shock after digesting the data and looking out extra carefully on the information. And the lower-than-expected ISM quantity, plus factoring in two main strikes and their influence on the roles numbers, calmed traders for a short time. Equities turned increased, and Treasury yields dropped. The market continued to seesaw between positive aspects and losses all through the buying and selling day.

Do not be stunned if the market reveals comparable habits subsequent week, as traders await December CPI information and the beginning of earnings season. This does not occur until the tip of the week, so count on extra of the identical till Thursday.

Based on the CME FedWatch Software, the likelihood of an rate of interest lower within the March Fed assembly is at 64%, decrease than earlier than as we speak’s information was launched. 2024 is a 50-50 12 months, with elections and the Fed’s rate of interest. Elections are going to happen in a number of international locations world wide. And with over half the world’s inhabitants heading to the polls this 12 months, it is sure to deliver some volatility to the inventory market.

From a seasonal perspective for the US market, the primary quarter of an election 12 months tends to be unstable. There’s an opportunity that shares may dump forward of the elections, however usually development increased after the elections. And whereas 2023 carried out as anticipated, seasonally, it does not imply you must sit again and count on your portfolio to develop on the finish of the 12 months. Preserve a watch on the broader market.

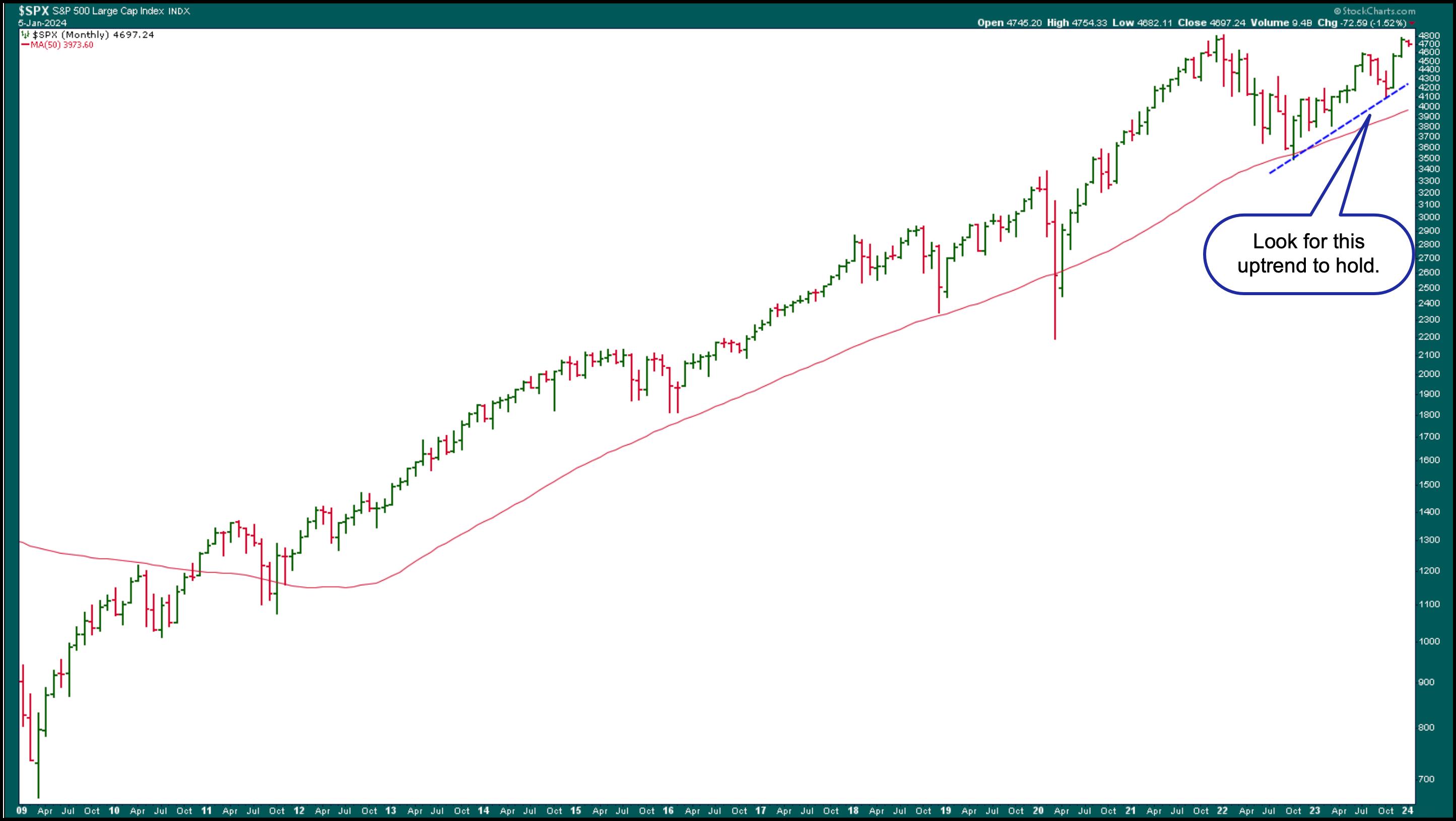

Given the S&P 500 index ($SPX) has been trending increased, buying and selling above its 50-month easy transferring common and displaying a comparatively steep uptrend since 2022 (see chart under), a correction should not be worrisome till the index nosedives under essential help ranges.

CHART 1. MONTHLY CHART OF S&P 500. The index has been trending increased since 2012 and, aside from a couple of situations, staying above its 50-month easy transferring common. A break under the blue dashed uptrend line may very well be the primary indication of a reversal.Chart supply: StockCharts.com. For academic functions.

We have now seen a rotation in management from Expertise to Financials and Well being Care, two sectors that struggled final 12 months. The hope of decrease rates of interest probably boosted the Financials, which have seen a pointy upside rally since early November. The Well being Care sector noticed an analogous transfer as Financials, although it pulled again a bit on Friday.

CHART 2. DAILY CHART OF FINANCIAL SELECT SECTOR SPDR ETF (XLF). After yields began falling, the Financials began recovering and rallied strongly.Chart supply: StockCharts.com. For academic functions.

However that does not imply the Magnificent Seven will lose their standing image. Though it closed off its excessive, Nvidia Corp. (NVDA) confirmed indicators of recovering as we speak. NVDA’s inventory nonetheless has a robust chart, sustaining help of its 50-day SMA. If the inventory continues to rally in 2024, it may pull the remainder of the market with it, particularly the opposite six shares that carefully observe behind. So do not lose religion within the mega-cap tech shares simply but.

CHART 3. NVIDIA STOCK IS STILL BULLISH. Do not quit on the Magnificent Seven shares; they may nonetheless rally increased.Chart supply: StockCharts.com. For academic functions.

It isn’t out of attain for Treasury yields to fall decrease, because the Fed is predicted to decrease charges. Decrease rates of interest may see progress shares pull again, however how a lot decrease are rates of interest more likely to go?

So long as the financial system retains chugging alongside, the expectations the market has priced in will in all probability maintain. However that does not imply rates of interest will fall near zero; extra probably, they may pull again, after which in all probability settle at across the 3% stage. So much has to do with the steadiness between rates of interest and financial progress.

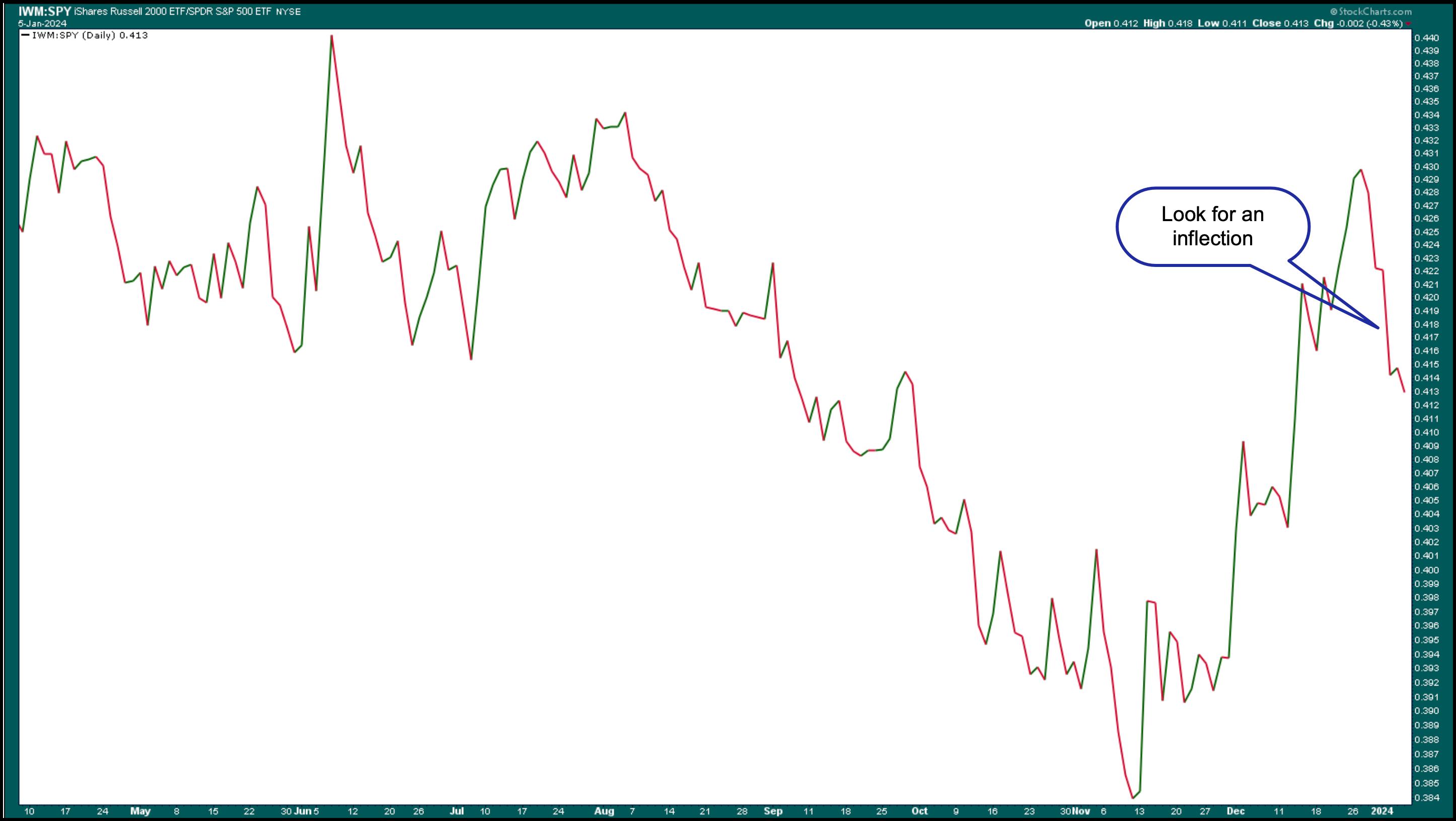

On a closing word, small-cap shares may present energy as charges fall. Regulate a chart of the small caps vs. massive caps in 2024, such because the one under of iShares Russell 2000 ETF vs. the SPDR S&P 500 ETF (IWM:SPY).

CHART 4. SMALL CAPS VS. LARGE CAPS. If the small caps begin outperforming the big caps and development increased, you could need to put extra weight on small-cap shares.Chart supply: StockCharts.com. For academic functions.

If there is a clear rotation and traders gravitate towards small-cap shares, it could be value including extra weight to this asset class.

Finish-of-Week Wrap-Up

- $SPX up 0.18% at 4697.24, $INDU up 0.07% at 37,466.11; $COMPQ up 0.09% at 14524.07

- $VIX down 5.52% at 13.35

- Greatest performing sector for the week: Well being Care

- Worst performing sector for the week: Expertise

- Prime 5 Massive Cap SCTR shares: Affirm Holdings (AFRM); USX-US Metal Group (X); Coinbase International (COIN); PDD Holdings (PDD); Karuna Therapeutics (KRTX)

On the Radar Subsequent Week

- December CPI

- December PPI

- Earnings season kicks off with Financial institution of America (BAC), JP Morgan Chase (JPM), Wells Fargo (WFC), Citigroup (C), Delta Airways (DAL), and extra.

Disclaimer: This weblog is for academic functions solely and shouldn’t be construed as monetary recommendation. The concepts and techniques ought to by no means be used with out first assessing your personal private and monetary state of affairs, or with out consulting a monetary skilled.

Jayanthi Gopalakrishnan is Director of Web site Content material at StockCharts.com. She spends her time arising with content material methods, delivering content material to coach merchants and traders, and discovering methods to make technical evaluation enjoyable. Jayanthi was Managing Editor at T3 Customized, a content material advertising company for monetary manufacturers. Previous to that, she was Managing Editor of Technical Evaluation of Shares & Commodities journal for 15+ years.

Be taught Extra