This week, traders shall control earnings from the 2 behemoths of the retail commerce sector – House Depot and Walmart. House Depot sells instruments, development merchandise, home equipment and providers whereas Walmart operates a series of hypermarkets, low cost shops and grocery shops. By market capitalization in the worldwide retail sector, each had been ranked 3rd and a couple ofnd respectively, proper after Amazon.

As of September 2023, US retail gross sales elevated 3.75% over the identical month within the earlier yr, nonetheless under the typical determine 4.83% from 1993 till 2023. Nonetheless, the info recorded a month-to-month upward improve of 0.7%, beating market forecast (0.3%). This may increasingly level to still-robust shopper spending (however may finally be hampered by higher-for-longer rates of interest). Classes which noticed a rise in gross sales are miscellaneous retailer retailers (3%), non-store retailers (1.1%), motor autos and elements sellers (1%), gasoline stations (0.9%), meals providers and ingesting locations (0.9%), well being and private care shops (0.8%), meals and beverage shops (0.4%) and basic merchandise shops (0.4%). Quite the opposite, classes which noticed a decline in gross sales are furnishings shops, electronics and home equipment, clothes shops, sporting items, interest, musical instrument and bookstores (-0.8%), in addition to constructing materials and backyard tools (-0.2%).

House Depot

The corporate shall launch its Q3 2023 earnings outcome on 14th November (Tuesday), earlier than market open.

In Q2 2023, House Depot reported income at $42.92B, higher than market expectation ($42.19B) for the primary time in three quarters. Nonetheless, the reported determine was barely down practically -2% from the identical interval final yr following continued stress in big-ticket, discretionary classes. Different objects underperformed in comparison with these in Q2 2022, similar to working revenue ($6.59B, down -8.6% (y/y)), internet revenue ($4.66B, down -9.9% (y/y)) and diluted EPS ($4.65, down -7.9% (y/y)).

Different headwinds embody normalization of demand for DIY initiatives, weakening housing market, rising costs, shopper spending shift and many others. The administration additionally identified that complete buyer transactions fell by practically –2% in comparison with the identical interval final yr. Following a mix of the aforementioned components, the administration reiterated its muted forecast for FY2023, with gross sales predicted to say no between 2%-5% in contrast with the year-ago interval., whereas EPS is anticipated to be down 7%-13% from the prior yr interval.

Consensus estimates for gross sales income of House Depot within the coming announcement stood at $37.6B, down -12.4% from the earlier quarter, and down -3.3% from the identical interval final yr.

However, EPS is anticipated to hit $3.77, down practically -19% from the earlier quarter. In Q3 2022, it was $4.24.

Technical Evaluation:

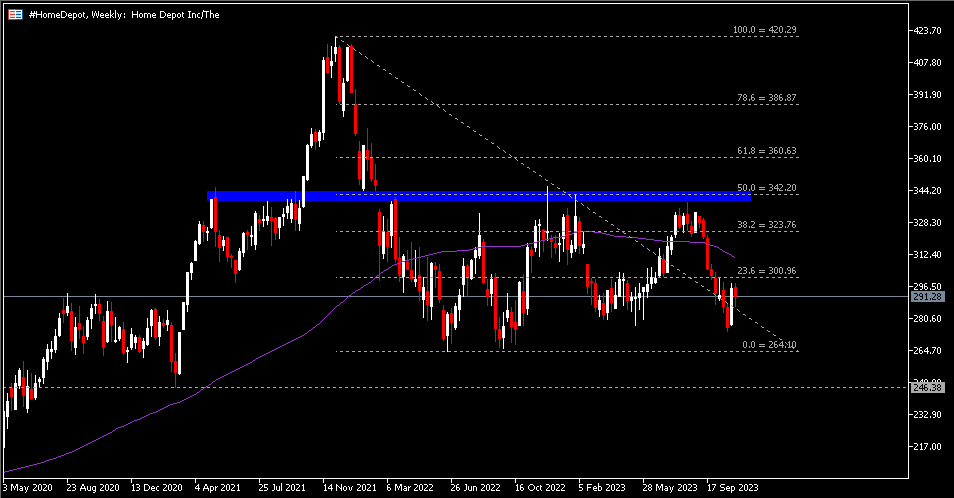

The #HomeDepot share value stays traded under resistance $301 (FR 23.6% prolonged from the excessive in Dec 2021 to the low in June 2022) and 100-week SMA, after forming a double high sample when the asset failed to interrupt the FR 50.0% at $342. Nearest assist is seen at $264.10 (the low seen in June 2022), adopted by the Feb 2021 lows at $246.38.

Walmart

The corporate is anticipated to report its earnings for Q3 2023 on 16th November (Thursday), earlier than the opening bell.

In distinction to House Depot, the important thing monetary metrics of Walmart had been stable within the earlier quarter. Gross sales income had been up 5.7% (y/y) to $161.6B.

The corporate continued to see development in eCommerce regionally (+24% (y/y)) and internationally (+26% (y/y), primarily led by China, Walmex and Flipkart) – the previous was pushed by grocery and Well being & Wellness (regardless of a modest decline basically merchandise gross sales), whereas the latter was boosted by energy in store-fulfilled. As well as, a division of Walmart – Sam’s Membership (paid membership based mostly warehouse, which sells groceries and home goods in bulk quantities) reported internet gross sales barely down -0.3% (y/y) to $21.8B. Nonetheless, the phase reported stable development in membership rely and revenue following continued energy in member development and renewals.

Working revenue was up +6.7% (y/y) to $7.3B. By enterprise segments, most important contribution got here from Walmart US ($6.11B, up +7.6% (y/y), whereas Walmart Worldwide noticed a leap of over 14% (y/y) in working revenue at $1.19B. Positive aspects had been barely offset by minor losses reported in Company & Assist.

Basically, Walmart’s steady innovation and progress in e-commerce is clear to all. Among the milestones achieved embody Walmart GoLocal, Walmart Luminate, Walmart Join, Walmart+, Spark Supply, Market and Walmart Achievement Providers. As well as, the corporate has numerous partnerships, investments and buyouts which hold the corporate at its aggressive edge.

Nonetheless, consensus estimates for gross sales income of Walmart stay flat at $156.8B, in distinction with the administration steering which anticipated a development of three%.

EPS is anticipated to hit $1.48, down over -19% from the earlier quarter. In Q3 2022, reported EPS was $1.50.

Technical Evaluation:

The #Walmart share value has traded in an uptrend since gaining assist in Could 2022. ATH is seen at $166.60, earlier than the asset closed the week at $166.05, above assist $160.75. Primarily based on the projection of Fibonacci Enlargement, the subsequent resistance to give attention to is $170, adopted by $181.40. However, a retrace under the mentioned assist might point out technical correction, to check the second larger low (inexperienced zone) at $151.60.

Click on right here to entry our Financial Calendar

Larince Zhang

Market Analyst

Disclaimer: This materials is supplied as a basic advertising and marketing communication for data functions solely and doesn’t represent an impartial funding analysis. Nothing on this communication accommodates, or must be thought-about as containing, an funding recommendation or an funding suggestion or a solicitation for the aim of shopping for or promoting of any monetary instrument. All data supplied is gathered from respected sources and any data containing a sign of previous efficiency just isn’t a assure or dependable indicator of future efficiency. Customers acknowledge that any funding in Leveraged Merchandise is characterised by a sure diploma of uncertainty and that any funding of this nature includes a excessive stage of danger for which the customers are solely accountable and liable. We assume no legal responsibility for any loss arising from any funding made based mostly on the knowledge supplied on this communication. This communication should not be reproduced or additional distributed with out our prior written permission.