Microsoft Corp., an American multinational know-how conglomerate at the moment ranked the second largest firm (after Apple Inc.) by market capitalization ($2.452T), which actively engages within the improvement and help of software program, providers, units and options, shall report its monetary outcomes for FY24 Q1 on 24th October (Tuesday), after market shut.

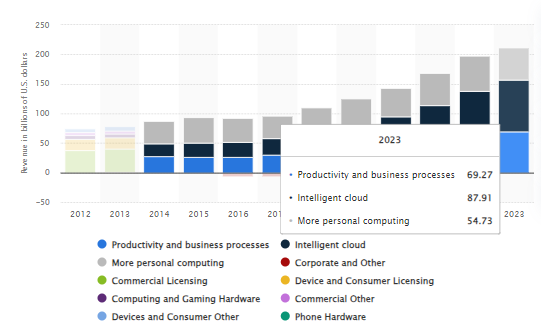

Microsoft derives its revenues from three most important segments. The primary phase is the Productiveness and Enterprise Processes phase, which incorporates services and products similar to Workplace Business, Workplace Shopper, LinkedIn and Dynamic Enterprise Options. The second phase is the Clever Cloud phase, together with numerous Server Merchandise and Cloud Companies, in addition to Enterprise Companies. The third phase is Extra Private Computing phase, involving Home windows, Units, Gaming, Search and Information Promoting. Clever Cloud has been the phase that has introduced essentially the most revenues to the corporate for the previous 4 years. In FY 2023, gross sales income generated from the phase was $87.91B, comprising over 40% from the entire income. Regardless of the macroeconomic difficulties, the corporate’s annual income for FY 2023 reached over $211B, up almost 6.9% from the earlier 12 months. A decade in the past, its whole income was round $78B.

Within the earlier quarter, the Clever Cloud phase continued to contribute essentially the most to the corporate’s income, at $23.99B (+14.7% y/y). Productiveness and Enterprise Processes and Extra Private Computing drove $18.29B (+10.2% y/y) and $13.91B (-3.2% y/y, primarily pushed by declining gross sales in Home windows OEM and units) in gross sales, respectively.

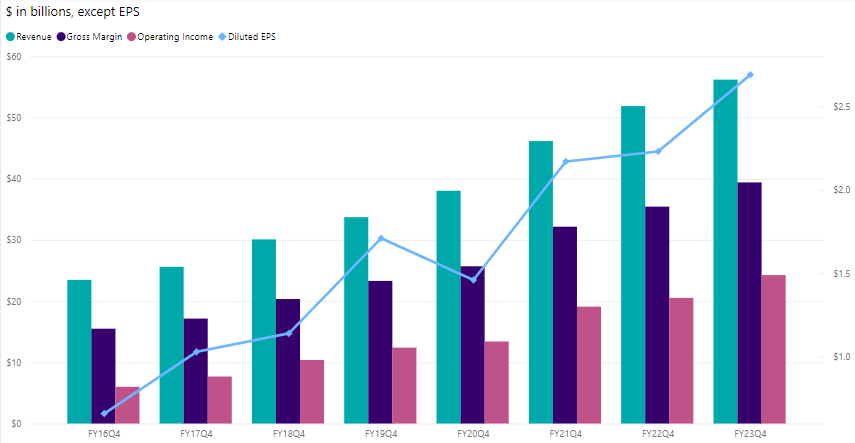

Working revenue of Clever Cloud is up over +19% (y/y) to $10.53B, whereas Productiveness and Enterprise Processes was up +25% (y/y) to $9.05B. Extra Private Computing edged up barely over +4% (y/y) to $4.68B. Internet revenue was $20.1B, up +20% from the identical interval final 12 months. Related with working revenue, the gross margin of Microsoft has been bettering steadily. Within the earlier quarter, it was $39.4B, up over 11% from the identical interval final 12 months.

The corporate has introduced not too long ago that it’s finalizing its $68.7B acquisition take care of Activision Blizzard (the subject with US FTC continues to be not finished but regardless). This in flip has made Microsoft the third largest gaming firm by income, simply after Tencent and Sony. It’s for sure that successful the deal would imply including extra Activision Blizzard video games to Xbox Sport Go in close to future, a plus level for bettering its general competitiveness within the gaming market. The Xbox at the moment affords 4 completely different subscription plans (from the bottom at $9.99 to the very best at $16.99 per 30 days) to swimsuit completely different preferences of its customers. As well as, the Sport Go Final and PC Sport Go solely price $1.00 for the primary 14 days of join, a method employed to draw and broaden its new person base.

Within the earlier quarter, Microsoft reported its gaming income was up 1% (+$36 million) from the prior 12 months interval. The Xbox content material and providers income alone was up 5%, pushed by progress in third social gathering content material and Xbox Sport Go. Nonetheless, its Xbox {hardware} income declined -13% (q/q), following softer demand for Xbox Collection S/X consoles. In accordance with Microsoft CFO Amy Hood, the outlook for Xbox content material and providers within the coming quarter ought to be up within the “mid to excessive single digits”, whereas there was no steerage supplied on the Xbox {hardware} revenues. The general gaming income is predicted to be up “mid single digits”.

Alternatively, there was information that Microsoft is slowly edging away from its partnership with Open AI (by growing in-house a smaller, more cost effective conversational AI) following the latter’s privateness gaffes, colossal computing prices and mounting losses. Additionally, Microsoft’s rising collaboration with Meta on Llama 2 fashions is seen to be contradicting with OpenAI’s curiosity as effectively, making a competitor for its closed supply fashions.

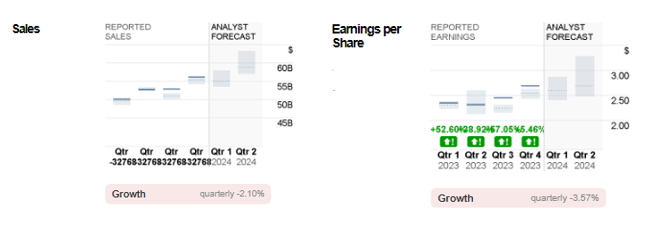

Microsoft: Reported Gross sales and EPS versus Analyst Forecast. Supply: CNN Enterprise

Consensus estimates for Microsoft’s gross sales income within the coming announcement stood at $55.0B, barely down from earlier quarter’s $56.2B, however up over 9% from the identical interval final 12 months. EPS is predicted to hit $2.59, down 10 cents from the earlier quarter. It was $2.35 in Q1 2023.

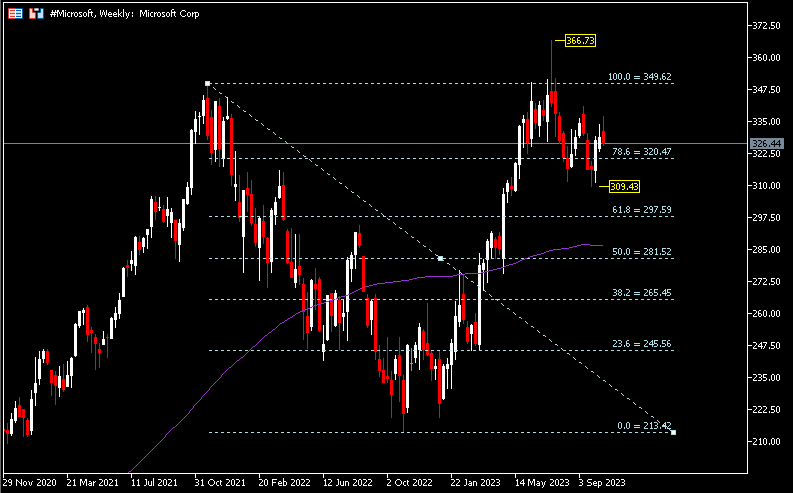

Technical Evaluation:

#Microsoft, Weekly: The primary half of 2023 has been good for the shares, till bullish momentum began waning in mid July after hitting an ATH at $366.73. Final week, the corporate’s share worth closed bearish, simply above help $320.50 (FR 78.6%). Breaking this degree could result in the bears persevering with testing latest lows at $309.43, adopted by $297.50 (FR 61.8%) and the dynamic help 100-SMA.

Click on right here to entry our Financial Calendar

Larince Zhang

Market Analyst

Disclaimer: This materials is supplied as a common advertising communication for data functions solely and doesn’t represent an unbiased funding analysis. Nothing on this communication comprises, or ought to be thought of as containing, an funding recommendation or an funding suggestion or a solicitation for the aim of shopping for or promoting of any monetary instrument. All data supplied is gathered from respected sources and any data containing a sign of previous efficiency isn’t a assure or dependable indicator of future efficiency. Customers acknowledge that any funding in Leveraged Merchandise is characterised by a sure diploma of uncertainty and that any funding of this nature entails a excessive degree of danger for which the customers are solely accountable and liable. We assume no legal responsibility for any loss arising from any funding made based mostly on the data supplied on this communication. This communication should not be reproduced or additional distributed with out our prior written permission.