Tuesday’s session was outlined by a convergence of forces that despatched U.S. Treasury yields climbing towards multi-year highs and lifted the greenback to its greatest single-session efficiency among the many main currencies. With WTI crude oil holding comfortably above $100 per barrel, the Iran battle displaying no indicators of decision, and resilient U.S. financial information preserving Federal Reserve charge hike hypothesis firmly in play, threat urge for food deteriorated via a lot of the day. Equities prolonged their current shedding streak whereas gold pulled again sharply, and the greenback drew broad-based help because the session’s standout performer.

Take a look at the foreign exchange information and financial updates you’ll have missed within the newest buying and selling session!

Foreign exchange Information Headlines & Information:

- New Zealand Digital Card Retail Gross sales for April 2026: 2.0% y/y (3.4% y/y forecast; 2.7% y/y earlier)

- Japan GDP Development Price Prel for Q1 2026: 2.1% y/y (1.5% y/y forecast; 1.3% y/y earlier)

- Japan GDP Value Index for Q1 2026: 3.4% y/y (3.0% y/y forecast; 3.4% y/y earlier)

- RBA Assembly Minutes (4 and 5 Might 2026): eight of 9 Financial Coverage Board members supported the 25 foundation level charge hike to 4.35%, with one member preferring to attend for extra information. The Board considered the rise as essential to handle inflation expectations amid rising gasoline costs from the Center East battle, whereas offering flexibility to evaluate the financial influence and family responses to the continued geopolitical state of affairs.

- Australia Westpac Shopper Confidence Change for Might 2026: 3.5% (-1.1% forecast; -12.5% earlier)

- Japan Industrial Manufacturing Remaining for March 2026: -0.4% m/m (-0.5% m/m forecast; -2.0% m/m earlier)

-

U.Okay. Employment Change for March 2026: 148.0k (95.0k forecast; 25.0k earlier)

- U.Okay. Unemployment Price for March 2026: 5.0% (4.9% forecast; 4.9% earlier)

- U.Okay. Claimant Depend Change for April 2026: 26.5k (32.0k forecast; 26.8k earlier)

- U.S. ADP Employment Change Weekly for Might 2, 2026: 42.25k (33.0k earlier)

- Canada Constructing Permits for March 2026: 10.3% m/m (3.8% m/m forecast; -8.4% m/m earlier)

- Canada New Housing Value Index for April 2026: -0.4% m/m (-0.1% m/m forecast; -0.2% m/m earlier)

- Canada CPI Development Price for April 2026: 2.8% y/y (3.0% y/y forecast; 2.4% y/y earlier); 0.4% m/m (0.7% m/m forecast; 0.9% m/m earlier)

- U.S. Pending Residence Gross sales for April 2026: 3.2% y/y (-0.5% y/y forecast; -1.1% y/y earlier)

- New Zealand International Dairy Commerce Value Index for Might 19, 2026: 0.6% (1.5% earlier)

Promoted: Day merchants & Scalpers have higher odds of constructing nice choices in the event that they see market catalysts immediately. Get the real-time feed that execs use to catch the information.

Be a part of FinancialJuice for Free to be taught extra!

Disclosure: We could earn a fee from our companions when you enroll via our hyperlinks, at no additional value to you.

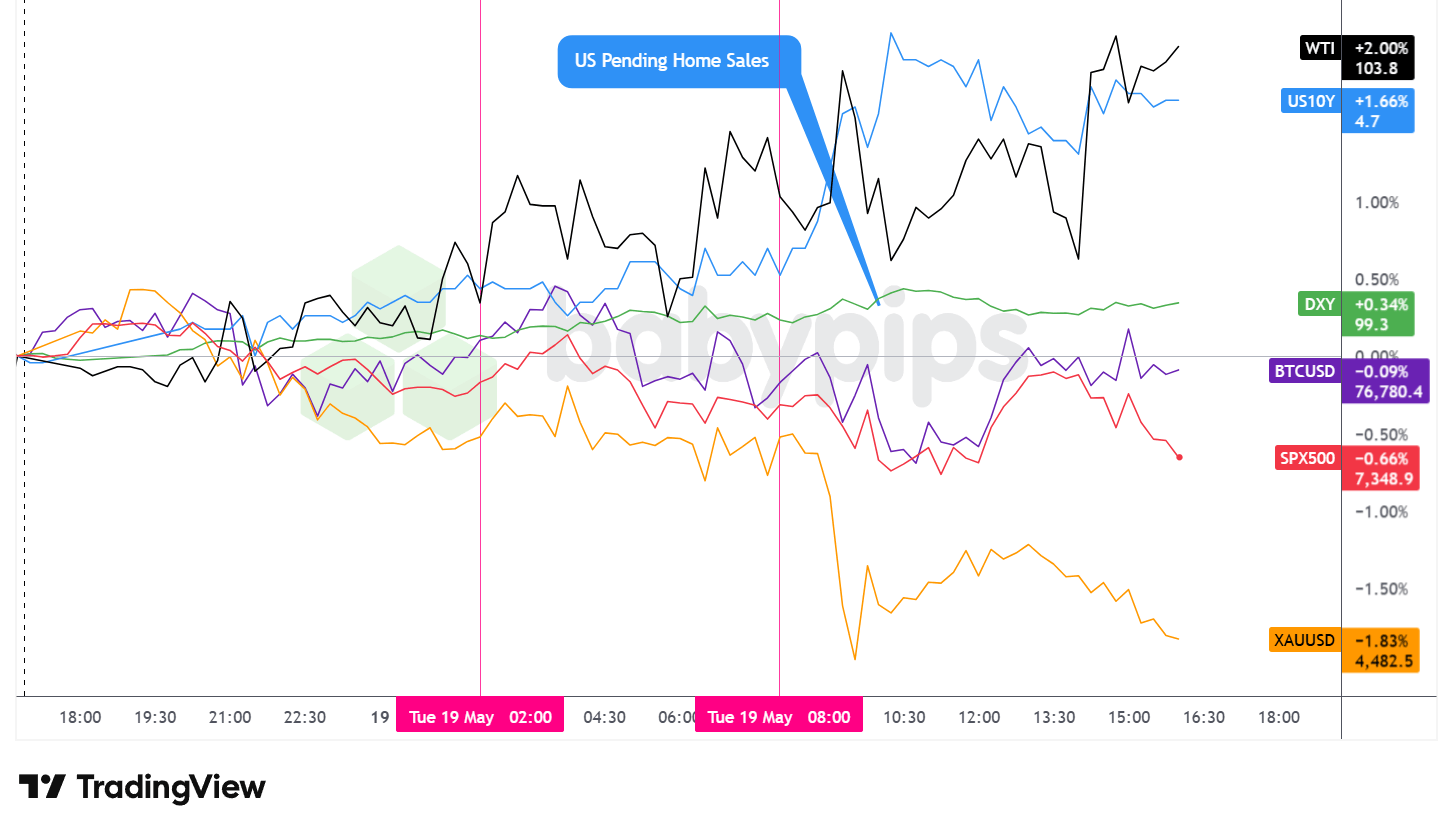

Broad Market Value Motion:

Greenback Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Quicker With TradingView

The session’s most consequential transfer was within the bond market, the place rising yields put stress on threat belongings throughout the board and bolstered the greenback’s outperformance on the day.

The U.S. 10-year Treasury yield rose roughly 1.66% on the day to commerce round 4.70%, touching ranges not seen in years as bond markets priced in a rising chance that elevated energy-driven inflation might push the Federal Reserve towards charge hikes somewhat than cuts. The 30-year yields individually reached their highest ranges since 2007 through the session, with the broader narrative centered on oil holding above $100 and the Iran battle offering no near-term aid on the inflation entrance.

The S&P 500 closed down roughly 0.66%, settling close to 7,348.9, extending the index’s longest shedding streak because the finish of March. The benchmark fairness index drifted decrease via a lot of the U.S. session towards the headwinds of rising bond yields and Fed charge hike hypothesis. A partial rebound in semiconductor shares offered some mid-session stabilization, although it was inadequate to reverse the broader pattern decrease. Nvidia’s earnings, due after Wednesday’s closing bell, have been extensively cited as a key near-term catalyst for the sector and broader market sentiment.

WTI crude oil was the session’s strongest performer, rising roughly 2.00% to commerce close to $103.80 per barrel. Oil remained comfortably above $100 per barrel, supported by the continued Hormuz disruption. Trump’s risk to renew strikes on Iran could have added a further geopolitical threat premium via the session, although a direct causal hyperlink can’t be confirmed.

Gold pulled again sharply, declining roughly 1.83% to commerce close to $4,482.50 per ounce. The valuable steel got here beneath sustained promoting stress starting across the London-to-U.S. session transition and continued decrease via the afternoon. The magnitude of the transfer doubtless mirrored, at the very least partly, the competing attraction of rising nominal Treasury yields pulling capital away from non-yielding belongings, although no single identifiable catalyst instantly explains the complete extent of the decline.

Bitcoin traded roughly flat on the session, edging down roughly 0.09% to commerce close to $76,780. The cryptocurrency oscillated in a relatively contained vary relative to the extra directional strikes elsewhere, displaying little decisive response to the macro crosscurrents dominating the session.

Promotion: In case your confidence has grown in your market consciousness & methods with this market recap, and also you wanna take motion, Maven Buying and selling may also help. They supply simulated funding challenges beginning as little as $15, permitting you to commerce main pairs with professional-sized capital. No closing dates imply you may take swing performs on these market themes with out the stress of a ticking clock.

Study Extra About Maven Buying and selling At present!

Disclosure: We could earn a fee from our companions when you enroll via our hyperlinks, at no additional value to you.

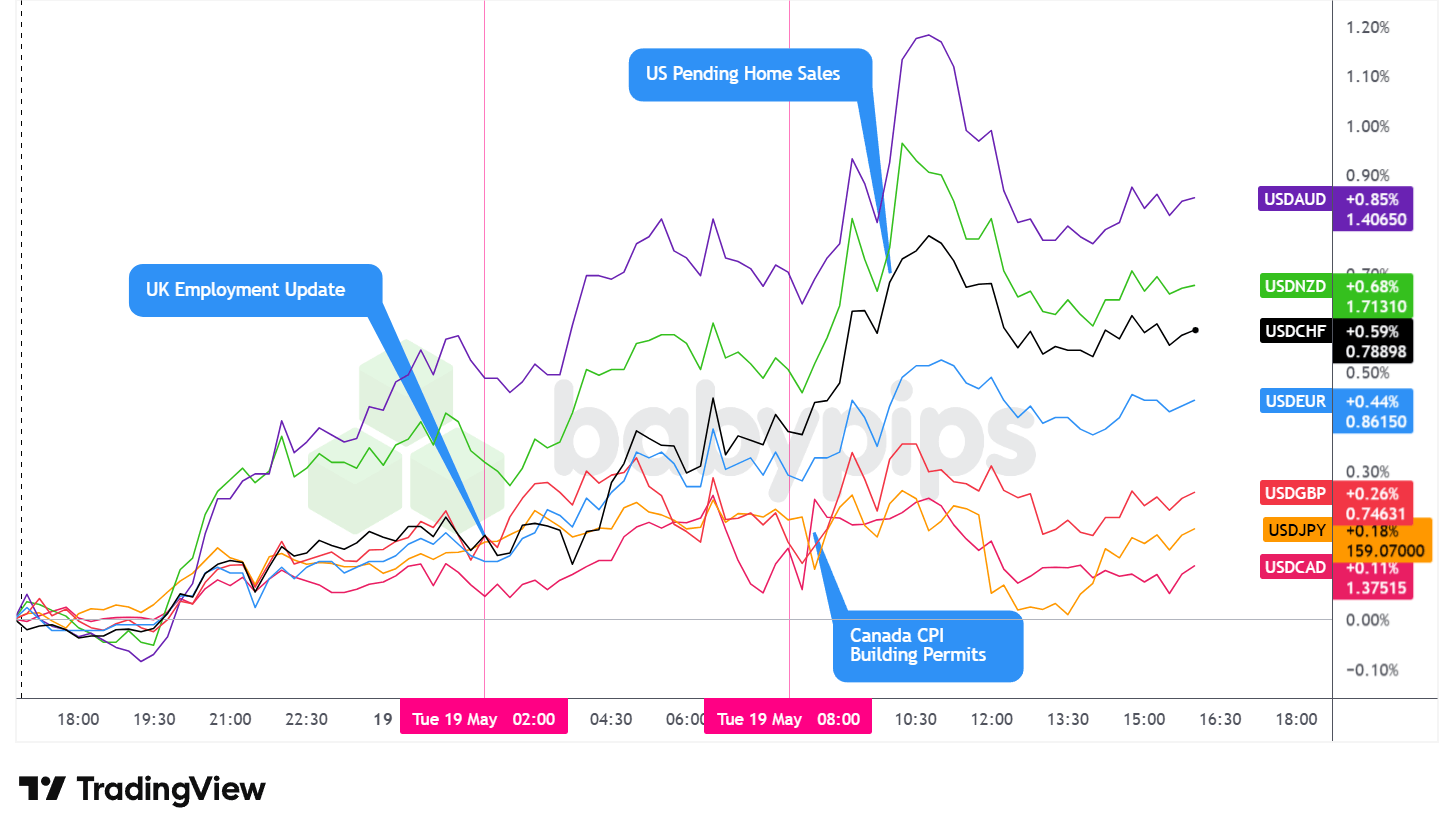

FX Market Habits: U.S. Greenback vs. Majors

Overlay of USD vs. Majors – Chart Quicker With TradingView

The U.S. greenback closed Tuesday because the best-performing main forex, extending positive factors broadly as a mixture of elevated Treasury yields, persistent Center East geopolitical uncertainty, resilient U.S. financial information, and rising Fed charge hike hypothesis offered underlying help for the dollar all through the session.

Throughout the Asian session, the greenback traded with a gradual bullish lean, step by step reclaiming Monday’s losses as AUD, NZD, GBP, and JPY all retreated. USD/JPY pushed towards 159, staying inside vary of the 160 stage Japanese authorities have flagged as a possible intervention set off. Japan’s Q1 GDP beat at 2.1% annualized versus a 1.5% forecast supplied preliminary help for threat belongings, although the Nikkei failed to carry early positive factors, with analysts noting the vitality shock’s full influence on development received’t be seen till Q2 information. The RBA minutes confirmed eight of 9 board members backed the hike to 4.35%, with language extensively learn as leaving June open as a potential pause whereas preserving August reside.

The London session was anchored by the UK jobs report, which leaned softer on steadiness. The unemployment charge ticked to five.0% towards a 4.9% forecast, and a provisional April payroll decline of 100,000 drew consideration, although the ONS flagged the estimate as topic to larger-than-usual revisions given the tax-year timing, a warning broadly echoed by analysts. The March employment change beat at 148,000 versus 95,000 anticipated, including to the combined image. The general information urged a labor market in gradual retreat with out delivering a clear dovish sign, and the greenback continued trending greater as yield and geopolitical dynamics dominated flows.

The U.S. session introduced Canada’s broadly softer-than-expected CPI suite alongside U.S. pending house gross sales. Canada’s headline CPI got here in at 2.8% year-on-year versus a 3.0% forecast, with core measures undershooting throughout the board — the Trimmed-Imply at 2.0% and Median at 2.1% each operating nicely beneath their 2.3% forecasts, suggesting underlying value pressures could also be cooling sooner than anticipated.

U.S. pending house gross sales got here in barely beneath the month-to-month forecast at 1.4%, although the year-on-year studying of three.2% beat expectations considerably. The greenback prolonged positive factors via a lot of the session, peaking close to the London shut earlier than pulling again modestly and stabilizing into the afternoon.

Promoted: The Technique is Half the Battle; Your Mindset is the Relaxation.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ critiques on Amazon) Jack Schwager interviews profitable merchants to disclose a standard fact: their edge isn’t simply information or abilities—it’s their psychological resilience and inflexible threat management. Whether or not you’re navigating shifting geopolitical themes or prime tier financial information, learn the way the “wizards” keep medical when the remainder of the market is emotional.

Grasp Your Buying and selling Mindset with Market Wizards!

Disclosure: We could earn a fee from our companions when you enroll via our hyperlinks, at no additional value to you.

Upcoming Potential Catalysts on the Financial Calendar

- U.S. API Crude Oil Inventory Change for Might 15, 2026 at 8:30 pm GMT

- U.S. Fed Paulson Speech at 11:00 pm GMT

- Japan Reuters Tankan Index for Might 2026 at 12:00 am GMT

- Australia Westpac Main Index for April 2026

- Germany PPI for April 2026 at 6:00 am GMT

- U.Okay. Inflation Development Charges for April 2026 at 6:00 am GMT

- China FDI (YTD) YoY for April 2026

- Euro space CPI Development Price Remaining for April 2026 at 9:00 am GMT

- U.S. MBA 30-Yr Mortgage Price for Might 15, 2026 at 11:00 am GMT

- U.S. MBA Mortgage Functions for Might 15, 2026 at 11:00 am GMT

- U.S. Fed Paulson Speech at 12:00 pm GMT

- U.S. Fed Barr Speech at 2:15 pm GMT

- U.S. EIA Crude Oil Shares Change for Might 15, 2026 at 2:30 pm GMT

- U.S. FOMC Minutes at 6:00 pm GMT

Wednesday’s calendar is headlined by the U.Okay. April inflation print at 6:00 am GMT, which would be the most intently watched launch of the session for foreign exchange merchants. With the Financial institution of England holding charges at 3.75% whereas balancing a weakening labor market towards energy-driven value stress from the Iran battle, any shock in both route might meaningfully shift BOE charge expectations and transfer sterling.

The eurozone CPI closing for April at 9:00 am GMT follows shortly after and will probably be scanned for any revision to preliminary readings.

The FOMC Minutes at 6:00 pm GMT spherical out the day because the session’s highest-impact U.S. occasion, with markets prone to parse the language intently for any indicators on how severely policymakers are weighing the potential of resuming charge hikes in response to the vitality shock.

On the oil aspect, the API crude inventory change estimate arrives within the night earlier than the official EIA stock information the next afternoon at 2:30 pm GMT.

Fed speeches from Paulson and Barr through the U.S. session may draw consideration given the present sensitivity round charge coverage messaging. Nvidia’s earnings after Wednesday’s closing bell add a further layer of occasion threat for fairness and threat sentiment extra broadly.

Keep frosty on the market, foreign exchange pals!

Tuesday’s session confirmed precisely how the bond market, fairness indices, oil costs, and geopolitical threat all moved collectively to form forex flows. However most merchants watch these markets individually, lacking the connections that predicted the greenback’s transfer earlier than it occurred. Premium members can learn our lesson:

📖 What Is Intermarket Evaluation?

Studying this helps you perceive how Treasury yields have an effect on forex actions, why rising bond yields supported the greenback whereas pressuring equities and gold, and find out how to learn shares, bonds, commodities, and currencies collectively so that you see the complete image earlier than putting any commerce.

And when you’re not a Premium subscriber but, now’s a great time to enroll.

With Babypips Premium, you get full entry to Faculty of Pipsology classes that allow you to perceive not simply how particular person markets transfer, however how they drive one another and form forex flows earlier than value motion even seems in your chart.