The second week of October noticed UK pure fuel futures costs improve by virtually 50% to £160, an 8-month excessive from simply £89 final week. The state of affairs was pushed by forecasts of colder climate which elevated demand amid provide considerations brought on by geopolitical dangers and labour disruptions on the Australian LNG amenities.

Because the weekend approaches, the UK is anticipating temperatures to drop sharply, with daytime highs in southern England anticipated to be 10 levels Celsius decrease than earlier within the week. The primary evening frosts of the season are doable in central and northern areas.

Relating to provides, Israel closed a fuel discipline on account of security considerations, whereas investigations into pipeline leaks within the Baltic raised considerations about winter security. As well as, some progress was made on Friday in talks between Chevron and unions over a wage and situations settlement for his or her LNG plant in Australia, however no remaining settlement has been reached on the time of writing. (BBC)

Surging pure fuel costs and rising US core inflation are two indicators that would immediate the BOE to lift rates of interest once more earlier than the tip of the 12 months. The rise in fuel costs may imply that the vitality part of the inflation basket will proceed to place stress on the headline inflation fee, because it did in August, which in flip will strengthen inflation expectations extra broadly.

Senior rate of interest setters on the BOE sounded cautious in signalling that the speed hike cycle is full. Governor Andrew Bailey mentioned on the IMF convention in Marrakesh that UK rate of interest choices can be “tight”. He mentioned regardless of stable progress in preventing inflation, there was nonetheless work to be accomplished. Such developments have helped shore up market expectations of additional fee hikes and pushed again expectations of the beginning of fee cuts. This dynamic is beneficial for Sterling.

In the meantime, the US Greenback surged on Thursday and Friday after the US reported that core providers inflation had elevated notably in September. Elevated safe-haven demand additionally supported the Greenback amid fears the battle between Israel and Hamas may spill over after Iran’s international minister mentioned Hezbollah militants may open a brand new entrance in Israel’s struggle.

Along with the prospect of tighter US financial coverage, Sterling confronted extra stress from UK industrial manufacturing information. In response to the most recent figures from the Workplace for Nationwide Statistics (ONS), revealed on Thursday, the nation’s industrial sector exercise declined once more in August. Manufacturing output fell by -0.8%, versus estimates of -0.4% and a -1.2% decline in July. Total industrial manufacturing fell by -0.7%, versus estimates of -0.2% and -1.1% within the earlier month. On an annualised foundation, though manufacturing output elevated by 2.8% in August, the determine nonetheless fell in need of the three.4% forecast. The general quantity of business manufacturing additionally fell in need of expectations, growing by just one.3% towards a forecast of 1.7%.

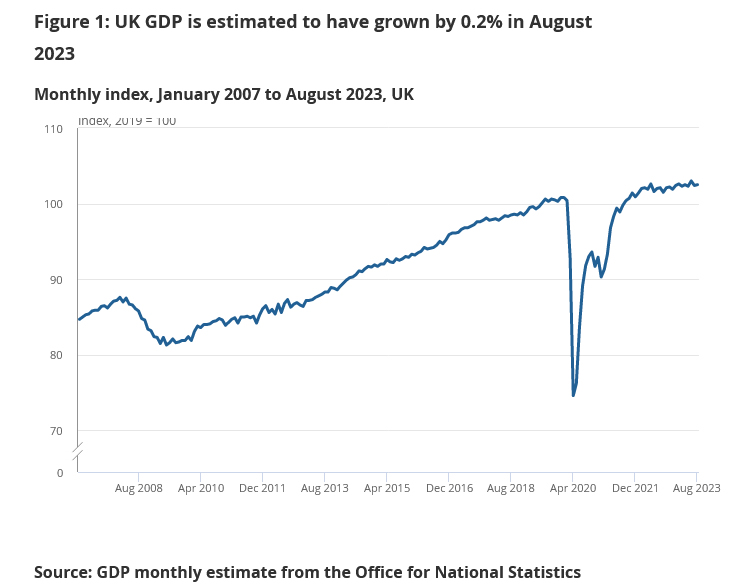

Even if UK GDP, after contracting by -0.6% in July, elevated by 0.2% in August, the danger of a slowdown in financial development is growing. That is largely on account of developments in geopolitical tensions within the Center East that are feared to disrupt international provide chains and rising costs of pure vitality sources that may improve inflationary pressures.

This case poses a dilemma for BOE resolution makers, between controlling inflation and stopping the economic system from slipping right into a extreme recession. The BOE rate of interest was unchanged at 5.25% in September. The following BOE assembly is scheduled for the 2nd of November and whether or not the regulator will select to lift charges even by just a few foundation factors stays a big query.

Technical Evaluation

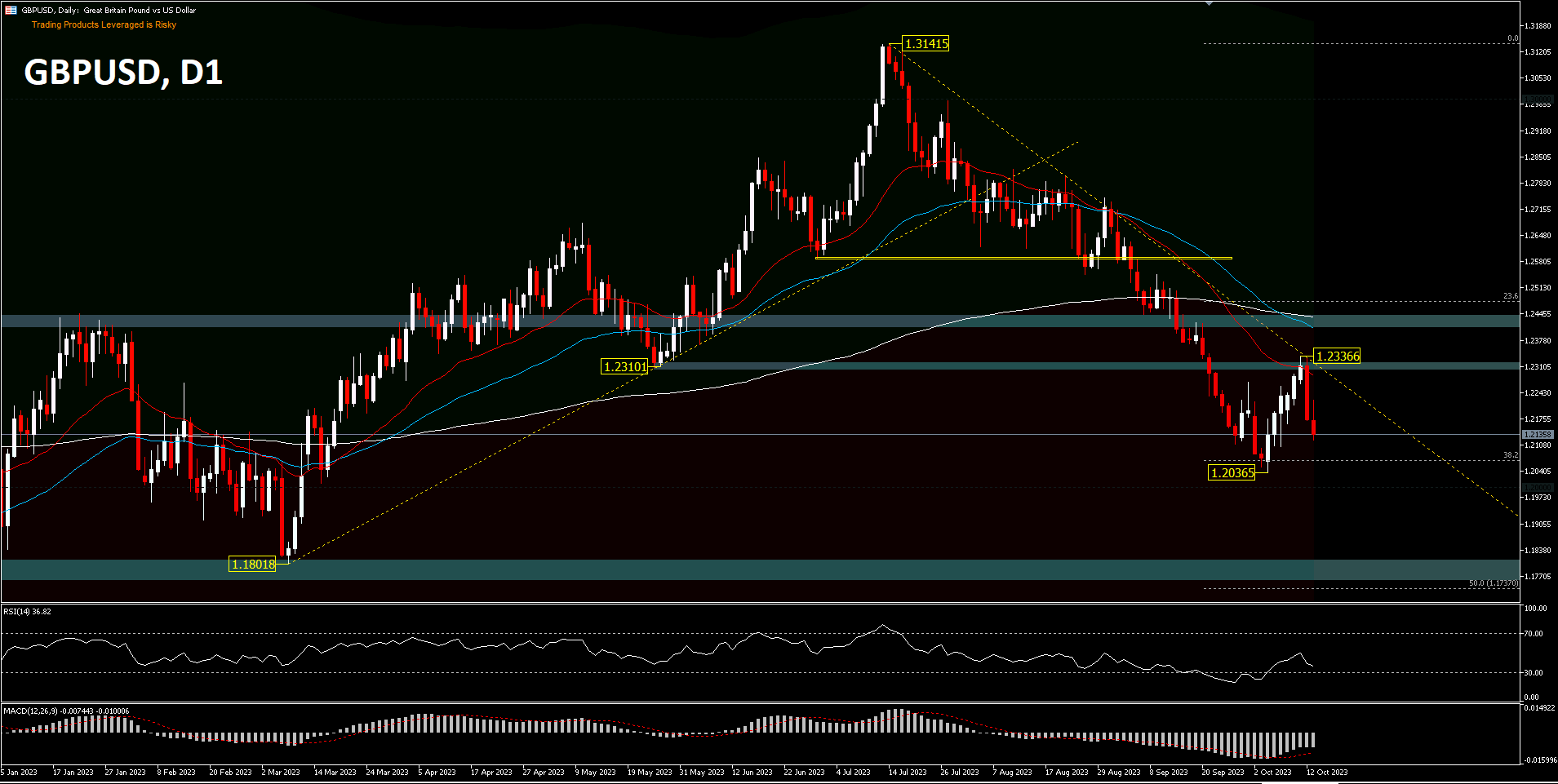

GBPUSD’s decline from the medium-term peak of 1.3141 remains to be a correction from the rise to 1.0330 (2022 low). However the danger of a complete pattern reversal is growing. A sustained break of the 38.2percentFR retracement of 1.0330-1.3141 pullback will open the way in which to the 50percentFR degree of 1.1737 first. For now, the danger will stay on the draw back so long as the 52 EMA holds, in case of a rebound. All every day technical indicators nonetheless validate the current decline.

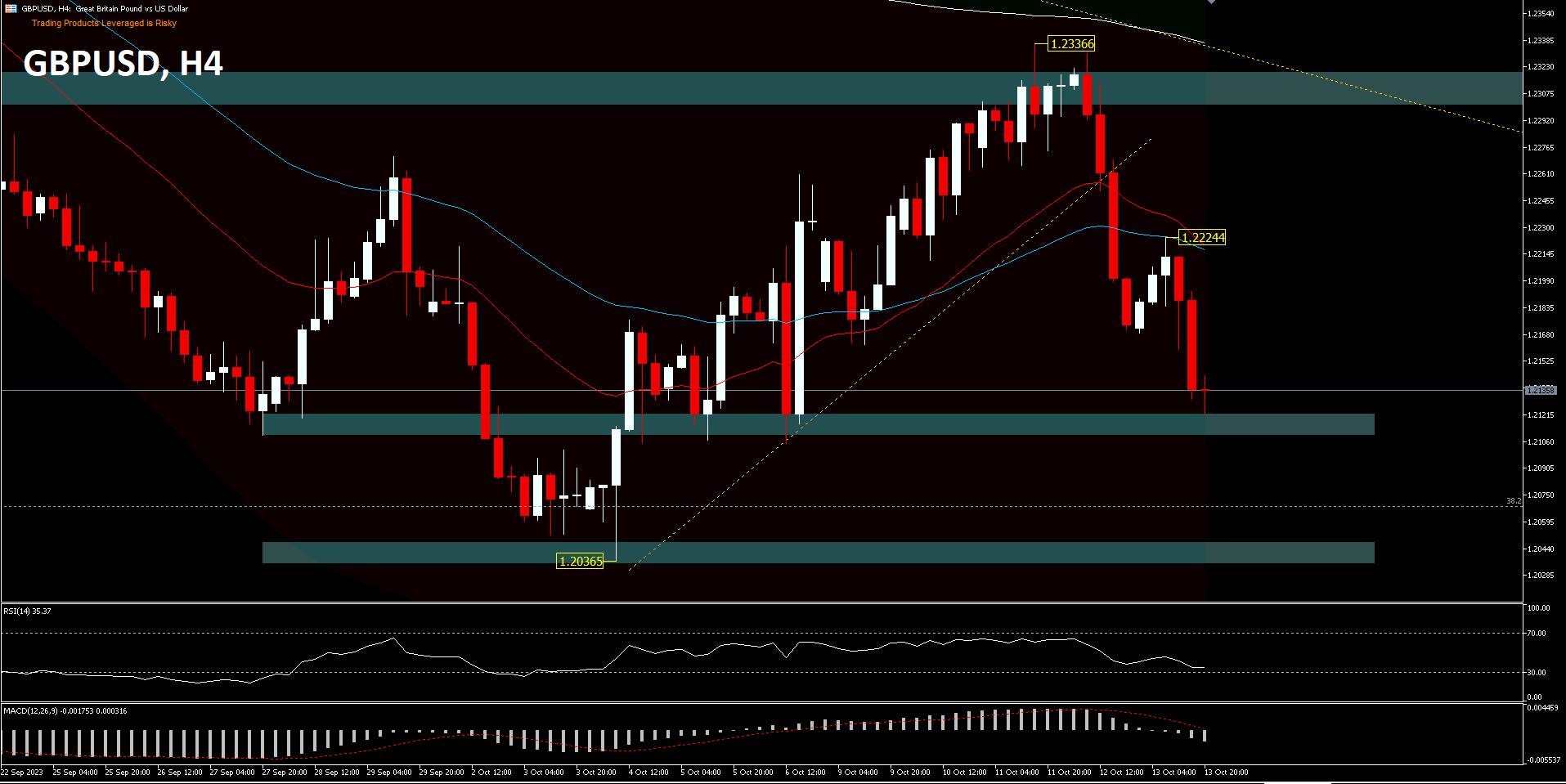

H4 – The rebound from 1.2036 continued increased final week, however was rejected by the short-term descending channel resistance [EMA 200] and has been weakening since then. Preliminary bias stays to the draw back this week for a retest of 1.2036. A robust breakout will resume the general decline from 1.3141 to the subsequent assist at 1.1801. On the upside, a transfer above 1.2224 minor resistance will change the intraday bias to impartial first. Nonetheless, the danger will stay on the draw back so long as 1.2336 resistance holds.

Click on right here to entry our Financial Calendar

Ady Phangestu

Market Analyst – HF Instructional Workplace – Indonesia

Disclaimer: This materials is offered as a normal advertising communication for data functions solely and doesn’t represent an impartial funding analysis. Nothing on this communication comprises, or ought to be thought-about as containing, an funding recommendation or an funding advice or a solicitation for the aim of shopping for or promoting of any monetary instrument. All data offered is gathered from respected sources and any data containing a sign of previous efficiency will not be a assure or dependable indicator of future efficiency. Customers acknowledge that any funding in Leveraged Merchandise is characterised by a sure diploma of uncertainty and that any funding of this nature entails a excessive degree of danger for which the customers are solely accountable and liable. We assume no legal responsibility for any loss arising from any funding made primarily based on the knowledge offered on this communication. This communication should not be reproduced or additional distributed with out our prior written permission.