Think about getting a dividend elevate yearly out of your investments, paid out month-to-month, whereas the underlying enterprise grows stronger and its credit standing improves. That’s the image forming for Morguard North American Residential REIT (TSX:MRG.UN), a residential landlord with a 4.5% yield that simply notched a serious credibility improve and is steadily marching towards Canadian dividend royalty. When you’re looking for recurring passive earnings, this REIT deserves a more in-depth look.

Supply: Getty Photos

Morguard Residential REIT graduates from high-yield danger to investment-grade stability

The largest information in April was that Morningstar DBRS upgraded Morguard North American Residential REIT’s credit standing from BB (excessive) to BBB (low). That will sound like simply one other notch climb, however right here’s the interpretation: the REIT is now not a borderline junk-rated borrower. It’s now formally an funding grade debt issuer for the primary time.

Why does this matter? An investment-grade standing unlocks cheaper, extra versatile financing. The REIT can now faucet the unsecured debt market on a lot better phrases, funding new developments or acquisitions with out considerably diluting unitholders.

This credit standing improve didn’t come from luck. The REIT spent the previous a number of years promoting roughly $770 million of non-core belongings, paying down debt, and laser-focusing its portfolio on multi-suite residential buildings in high-demand markets. That self-discipline immediately strengthens the reliability of the 4.5% dividend you’re amassing each month.

A billion-dollar partnership with TD Asset Administration

In February, Morguard and the REIT introduced a three way partnership with TD Asset Administration to construct a $1 billion Canadian multi-suite residential portfolio. Critically, Morguard North American Residential REIT will act because the portfolio supervisor, incomes recurring administration charges and potential commissions. This association places the REIT in a capital-light position, amassing payment earnings that may additional assist its distribution with out saddling the steadiness sheet. Consider it as a facet stream of money that flows straight into the dividend security internet.

Yet another elevate away from dividend supremacy

Morguard North American Residential REIT has elevated its distribution for 4 consecutive years. If administration delivers one other elevate in 2026, mixed with that contemporary investment-grade credit standing, the REIT may doubtlessly graduate into the distinguished S&P/TSX Canadian Dividend Aristocrats Index—a membership reserved for high-quality Canadian dividend shares with at the very least 5 years of consecutive dividend development.

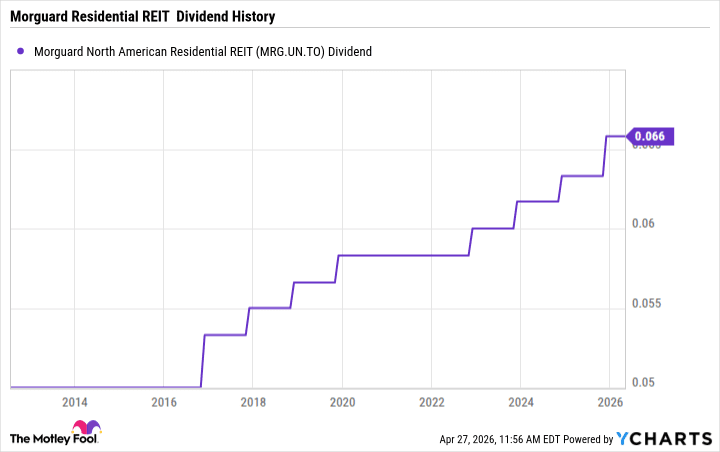

MRG.UN Dividend information by YCharts

Even with out the index membership, MRG.UN’s dividend observe document is spectacular. Since its first payout in 2012, the REIT has by no means missed a month-to-month cheque. It has raised its annual dividend in eight of the previous 13 years. The present month-to-month distribution of $0.06583 per unit is backed by a funds from operations (FFO) payout ratio of simply 42.7% in 2025, a big enchancment from 45% the 12 months earlier than. That leaves a large margin of security, which means the distribution may continue to grow within the close to future whilst residential rental markets briefly soften a bit.

Operations strengthening, models undervalued

The residential REIT’s underlying portfolio is performing nicely, too. In 2025, internet working earnings climbed 4.6% 12 months over 12 months, and diluted FFO per unit surged 8.5%. Administration was so satisfied the market mispriced the REIT’s models that it repurchased $24.3 million value of models at a median worth of $17.40. Professionals and insiders noticed deep worth on the month-to-month payer’s fairness models.

However occupancy dipped in 2025, with Canadian flats at 93.3% (down from 97.2% on the finish of 2024) and U.S. suites closing 2025 at 91.3%. Whereas that warrants monitoring, common month-to-month lease nonetheless rose 4.5% in Canada and 1.2% within the U.S. The REIT expects portfolio economics to stabilize by way of 2026 as demand for multi-family housing continues to outstrip provide, notably in its Solar Belt U.S. markets and Alberta.

What to look at now

Morguard North American Residential REIT reviews first-quarter 2026 earnings on Tuesday, April 28, with a convention name on Could 1. Buyers ought to hear for commentary on lease tendencies, occupancy restoration, and any trace in regards to the subsequent distribution improve. With a rising, well-covered month-to-month payout, a freshly minted investment-grade steadiness sheet, and a transparent path towards dividend “aristocracy”, MRG.UN is shaping as much as be a compelling month-to-month earnings machine for affected person Canadian traders.